This is not a feature, but a bug in the system. That’s why bank deposits walks (not runs). At some point the NII has to start coming down. It will.

Of course! Now one has to question the stress test itself because, FED has aggressively increased the rates and says if inflation continues they will continue to raise and rates may stay higher for longer, how come they are not testing for a scenario?? I mean testing for recession is great, what if economy stays red hot and inflation comes back and fed raises rates?

I have been highlighting that BAC has a leverage in reducing their manpower cost. BAC has gotten bigger by acquiring lot of small banks and they have never right sized. Now, from the GFC they have invested heavily on technology, so their tech expenses are not going to be high (compared to WFC or C) and they can slowly reduce their manpower, reduce branches and this is a nice 1% to 2% tailwind.

I don’t believe you are correct. This is “the” feature. Banks cost of funds is their interest cost plus a large portion of the fixed cost of building and staffing a local branch system. In low rate environments the fixed costs weigh heavily. In a higher rate environment, I would add that current rates are closer to normal than high, the fixed costs stay relatively flat while the interest expense rises. But the blended cost (interest expense plus operating expenses for the branch system) rise slower than the reinvestment rate). You are witnessing this and will continue to see it over the next year or more. The deposits will not run away to higher rates at other banks nor at BAC either. You just have to focus on each customer and what they are using their accounts for, plus their own knowledge of the personal benefits/costs of moving the funds. It is just not going to move around. Never has never will. BAC, WFC, USB will all have higher Net Interest Income in 2023 than 2022. Likely by 10% or more. You will see more evidence of this in 2 weeks.

Think about this concept. Stronger economy, lower credit losses, higher rates.

Weak economy, higher credit losses, lower rates.

Both seem perfectly rational.

Again, you need to focus on the whole balance sheet, not just the parts (securities) that are easy to market to market (level 1) things. All the assets and liabilities need to be remarked to get a overall impact to BAC. It can be done, but just looking at the securities position is biased.

Trouble? Why? Do they ever explain why? A security is just a loan with lower origination cost and lower expected credit losses, offset by a lower yield.

All of the securities, like all assets, are reflected in the current operating earnings. Which I would add are at a record high! So what is the trouble? Is there an opportunity cost, sure, is it big, yes. Is it going to bring down the business, of course not. And every day some of it rolls off and reprices at current higher rates. If BAC does nothing and all other product rates are stagnant, BAC earning rise. So what is the trouble? The trouble is that headlines like this sell papers or clicks or whatever else you are pushing. I bought 10% more BAC last week. Wells too.

1 Like

“” Trouble? Why? Do they ever explain why?

[/quote]”” did you read it ?

I do not have access to the seeking alpha article. However, this is the 3rd version of this headline that I have come across over the past week, including the financial times. I did read those. Along with Dick Bove comments, who I typically like. No meat on any of them. FWIW, the Q2 mark loss will be more like $120 BB+. Of course all the liabilities are repricing as well. BAC was very smart to hedge their AFS portfolio. Nobody gets everything right. However, I don’t see it as doom and gloom.

If you can grab relevant parts from the seeking alpha article, would be interested in see it.

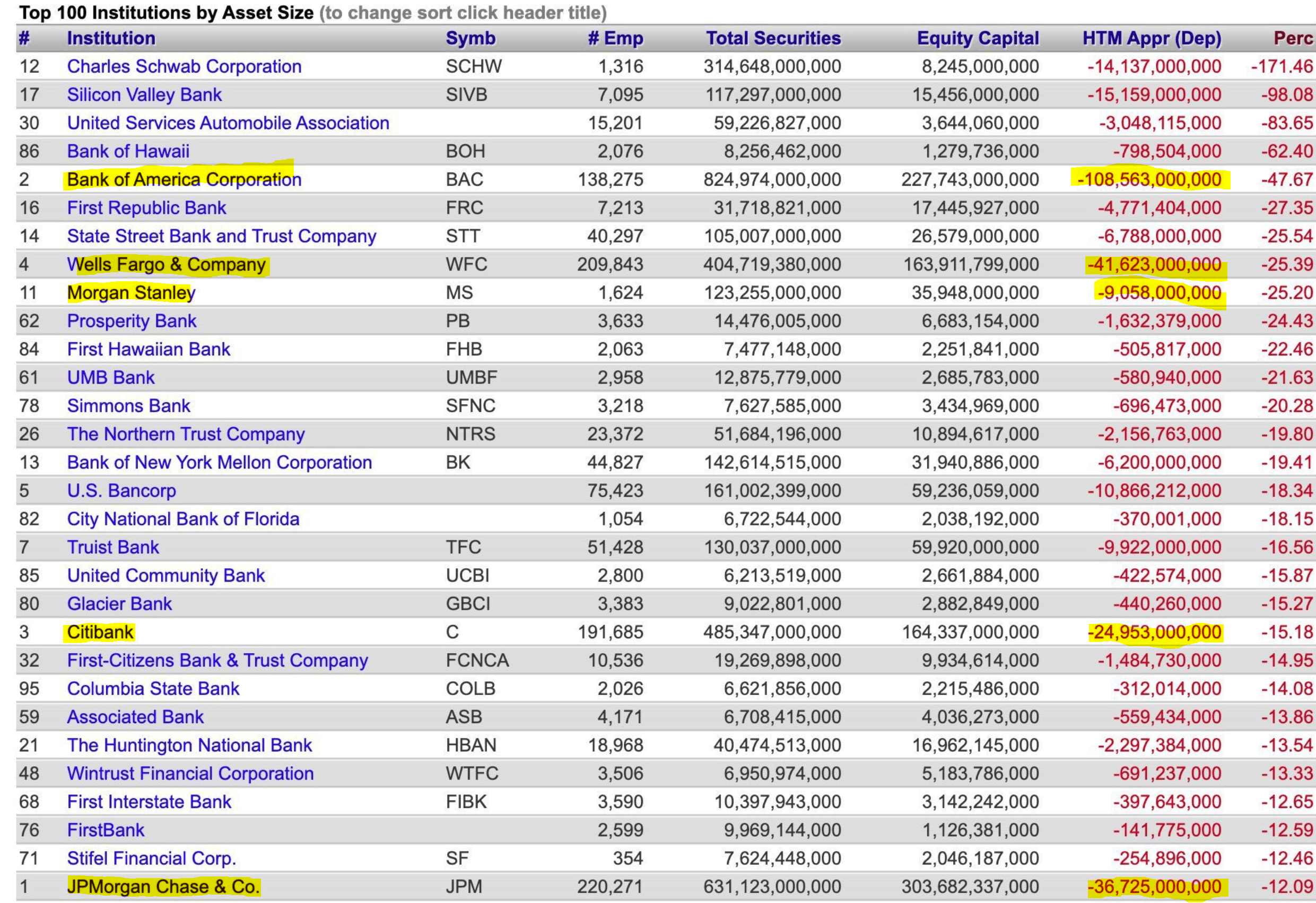

“” As a result of the repricing of bonds, Bank of America’s investment portfolio suffered substantial paper losses, surpassing $100 billion, as disclosed by the Federal Deposit Insurance Corporation at the end of the first quarter. These losses stand out prominently when compared to the unrealized losses incurred by rivals.

For reference, the unrealized losses of key competitors JPMorgan Chase (JPM), Wells Fargo (WFC), Citigroup (C), Morgan Stanley (MS) amounted to only approximately $37 billion, $42 billion, $24 billion and $9 billion respectively.

FDIC

An interesting comparison versus JPMorgan stands out, and highlights the importance of a bank’s management team. While BofA CEO Brian Moynihan was quite nonchalant about capital allocation during the 2020-2021 bubble in fixed income markets …

Deposits have crossed $1.9 trillion and the loans are $900 billion and change. And that difference has got to be put to work . . . we’re not timing the market or betting. We just sort of deploy it when we’re sure it’s really going to be there

… JPMorgan’s CEO Jamie Dimon was very reluctant to move excess cash into low-yielding treasuries …

I would not be a buyer of Treasuries … I think Treasurys at these rates, I wouldn’t touch them with a 10-foot pole.

Thanks. This is what I am talking about. This is one chart covering 0% of BAC liabilities and 20% of their assets. Seems like it is missing a lot of useful information. Yes, BAC did not optimize the opportunity, but that is not what the headline read. The headline read “trouble!”. What trouble. BAC earns $3.50+ per share. Has hundreds of millions in cash, no need for hot money (CD’s). Low credit risk profile (BAC has a great chart in one of their presentation comparing 10 years ago balance sheet to today). If you want to know the real story on BAC, don’t read the hacks in the media, just go through BAC quarterly presentation and the recent open discussion I think at MS conference (this discussion is great if you are like me and grew up in consumer banking). They go through in great detail their philosophy on banking and their key performance indicators. Don’t be an armchair finance guy, be a banker and see what they have built. There is nothing more important than credit discipline. Same as insurance and pricing. You should be very impressed and all of your questions might get answered. I like WFC and they are a fan favorite, but their credit profile is no where near as solid as BAC. But they are fine as well. Every bank is different.

FWIW. That chart is at least a month old. Every basis point change in rates impacts every line in the balance sheet. However, all of the lines don’t have public trading markets for comparison. But I assure you, that during an acquisition every line will get marked to market. The shortcut proxy is net interest income. Which has risen every year. In spite of the securities exposure, BAC maintains an asset sensitive overall position. SIVB was liability sensitive. They have publicly stated that they model NIM to be higher if rates rise not lower. Even though the negative securities mark will get larger. That is the end game. Not one line item, but the whole kit and caboodle.

One final observation. Even if you think BAC IV should reflect the securities loss, dollar for dollar after tax ($109 BB x .79%), that would only be about $88 BB. BAC market cap has decline by over $200 BB? Makes no sense to me.

Just saying, it is not the credit that caused the collapse of SVB.

Somehow that assumes the earlier market value is correct valuation. Look, I am very long BAC, but the arguments you are putting out doesn’t make sense.

2 Likes

Good morning, as you know Buffett is basically none confrontational. He isn’t going to say, publicly , that team bac dropped the ball on duration risk. What other, mistakes, are not yet fully disclosed? If he was offered 31 for the block, would he sell it ? I think he would, just by reading him, but we can’t be certain. Happy fourth to those who celebrate ![]()

![]()

Go take a look at BAC Q1 2023 earnings presentation on securities and yield. Slides 9 - 12.

Next look at BAC Q4 2022 earnings presentation on credit profile page 37.

Make your own conclusions.

BAC is a core position for Berkshire and they are over 10% investors. This is not a crisis and BAC has earnings to ride this. What stock price does in the interim is of least concern to Berkshire and Buffett.