Jumping right in, the big changes I made in April were that I added a number of new trial positions, and I sold a lot of Cloudflare, which I know has been a popular stock around here for a long time. I didn’t sell out of it completely, and I don’t intend to for the time being.

And regarding Enphase, its report, while not bad, was not good enough for me to take a significantly bigger interest in it. Its report made me more likely to sell it when something more appealing comes along.

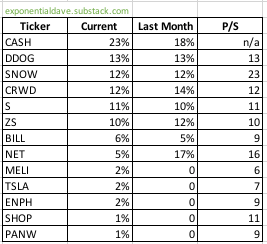

Current Positions

I know GAAP is not very popular around here (and with good reason - it is quite dumb sometimes), but the common denominator with most of my new stocks is that they are GAAP profitable. Most of the stocks performing well in the past 6-12 months have been GAAP profitable, so I am experimenting with diversifying into some GAAP profitable growth stocks.

Performance

My portfolio is up 26% as of writing on 4/30/2023 from when I started tracking my results in January of 2020. Meanwhile my benchmark, WCLD, is up 2% since January of 2020, and the S&P 500 is up 29% since January 2020. For the period from January 1st, 2023 through 4/30/2023, my portfolio is down 5%, meanwhile WCLD is up 6%, and the S&P 500 is up 9%.

- 2020 Performance: 225%

- 2021 Performance: 30%

- 2022 Performance: -69%

- 2023 Performance: -5%

- Cumulative Performance 1/1/2020 - 4/30/2023: 26%

Cloudflare

The numbers themselves weren’t horrible, and Cloudflare’s long term investment thesis is intact. But here’s what was bad: they lost their claim of revenue growth predictability. Cloudflare had often touted its revenue predictability, and they deserved it! They had grown revenue eerily consistently for every single quarter they’ve ever had as a public company (more than 12 at this point). And more importantly, they had never failed to beat and raise their annual guide, even if only by a little bit.

This is the quarter where that trend was broken. They missed their quarterly revenue estimate by $0.8 million, which honestly I could probably look past. That’s not a huge deal. But it is paired with a pretty big drop in their annual guide from 37% to 31%, only a couple months after they told us 37%!

Furthermore, their current annual guide has a built in acceleration in QoQ growth from here. Specifically they now estimate 2023 revenues to be $1.284 billion. Q1 was $290.2 million, representing 6% QoQ growth. They just guided for $306 million in Q2, which is 5% QoQ growth. They have come in basically right at their guide the past two quarters in a row, so it would not be wise to think they will beat their guidance for Q2. So let’s say they hit $306 million like they forecast. That means that they have $596.2 million in revenue for H1 2023. Then to hit their $1.284 billion annual guide, they need $687 million in H2 2023, which would represent roughly 8% QoQ growth in each of Q3 and Q4. They just barely eeked out 6% QoQ growth in Q1 and guided to 5% growth in Q2. So they are forecasting an acceleration to 8% growth in back to back quarters after they just got knocked on their butts and proved that this challenging macro environment has made it too hard for them to forecast accurately.

After the blunders of this quarter, I just don’t have full confidence in their ability to hit their own estimates (which seem pretty optimistic). Missing estimates, as we’ve just seen, could lead to another 25% haircut. For this alone, I need to sell a lot of Cloudflare, seeing as it was a whopping 17% position before this earnings call.

Looking objectively here, assuming they can grow between 25%-30% for 2023, I am still interested in owning Cloudflare, just not a 17% position, or anywhere near that. It currently sits around a 6% position and I intend to probably keep it between 3%-6%.

Some positive notes:

- Non-GAAP net income hit a record $27m, while GAAP net loss narrowed to -$38m from -$41m last year

- Free cash flow of $13.9 million, a FCF margin of 5%

Negatives:

- Missed quarterly revenue guide by a hair

- Lowered annual revenue guide significantly (37% → 31%)

- DBNRR (dollar based net retention rate) 127% last year to 117% now

- Founder CEO Matthew Prince going out of his way to throw their sales and GTM teams under the bus. Not a good look for a so called leader

To throw in a different opinion, there is a pretty shrewd guy I follow who covers many stocks, and in his opinion now that Cloudflare has suffered its 25% discount, its expectations have been reset. And according to him, now it’s a bargain. I really hope he’s right, but as someone who has followed this stock for years, I can tell you we’ve had quite a few price resets, and Cloudflare keeps finding new ways to drop even lower.

It’s probably been way over discussed at this point, but I would be remiss if I didn’t talk about Matthew Prince’s behavior. There are numerous cringey quotes from him in this call. I’m not going to list all of them, but this one where he dodges responsibility and makes light of people about to get fired probably takes the cake:

…we saw a lot of our success with our enterprise customers because our products were so good and solved real problems that every big company faces. That allowed many on our sales team to succeed largely by just taking orders. When the fish are jumping right in the boat, you don’t need to be a very good fishermen.

But at the risk of mixing watering metaphors, as the tide goes out, you get a clear view who’s not wearing shorts. The macroeconomic environment has gotten harder, and we’re seeing that some on our team aren’t dressed for work. Digging in with Marc, we’ve identified more than 100 people on our sales team who have consistently missed expectations… We are now in the process of quickly rotating out those members of our team who have been underperforming and bringing in new with salespeople who have a proven track record of success, grit and a strong cultural fit.

For the record, I don’t think one lowered annual guide and one missed quarterly revenue estimate suddenly means that Cloudflare is a bad investment. But I do think that in the context of this challenging macro environment, Cloudflare is likely to have a rough 2023 coming. And I don’t want to come along for the ride with 17% of my portfolio.

What Cloudflare’s Adjustment Means for my Other Stocks

My concern is that Cloudflare’s problems are going to be a problem for most or all enterprise SaaS stocks. I am most concerned about Datadog, Snowflake, Zscaler, Crowdstrike, Bill, and SentinelOne. Why isn’t my newest holding Palo Alto in there? Because it’s GAAP profitable, and the market has not thrashed GAAP profitable companies nearly as much as our favorite unprofitable SaaS stocks (this is why I’m exploring Mercado Libre, Tesla, etc).

What exactly did Cloudflare cite as the reasons for decreased business output?

- Slower expansion from existing customers

- macro uncertainty

- Silicon Valley Bank crisis

- Lengthened sales cycles (27% longer on average)

- Significant decline in close rates (but not in win rates)

- An extreme back end weighting to the quarter (almost half of new business closed in last 2 weeks of quarter)

- Go to market team holding back the rest of Cloudflare

- Companies being increasingly cautious and deeply scrutinizing spend

- Delays in collections

Unfortunately, pretty much every one of those things could be affecting my other B2B SaaS companies. But I’ll be the first to admit these fears may be overblown, and I hope they are. After all, Datadog already issued a particularly soft annual guide already, Snowflake already downward revised their FY guidance, and Bill’s upcoming quarterly guide is quite weak. The good news is that not all these companies report earnings at the same time, so the ones reporting sooner (DDOG and BILL on Thursday 5/4 of this week) can give us an idea of whether or not Cloudflare’s problems are specific to Cloudflare or more widespread across other companies.

Furthermore, I sense that many are not fully aware of what I perceive as a “tech recession”, so here are some extra details on sustained deterioration in cloud software spending growth. Amazon Web Services (AWS) reported that its QoQ growth rounds to 0%, which is to say that it didn’t grow at all. This has never happened in the ten years of AWS revenues data that I have. And its YoY growth rate does not paint a much better picture. Its YoY growth was 16%, but as recently as 3 quarters ago it was at 33%. And historically it’s been in the 30%-40% range. Microsoft Azure and Google’s GCP are much cagier with their specific revenue numbers. But the trend is clear, cloud spending growth is in a sustained downward trend.

The good news is, the market to some degree knows the relation between Cloudflare and the other cloud stocks. When Cloudflare and other tech stocks have bad reports, we tend to see small drops in the others. So maybe some of the possible pain ahead has been “priced in”, as many market analysts love to say. But one thing we’ve learned is that, for the most part, no amount of “priced in” will save a growth stock from a big drop if they:

- Miss guidance

- Lower their annual guide

- Post a big YoY drop in revenue , even if it seems “obvious” to everyone paying attention that it was going to happen (probably the fancy trading algorithms the smart money uses go wild with selling when this happens)

For all these reasons, I think I’m going to be doing some very out of character (for me anyway) portfolio maneuvers that are off topic for this board. So I won’t discuss them further here.

I remain hugely bullish on each of these stocks in the long term. But in the extreme short term I am somewhat bearish for each of their upcoming earnings reports, at least until we see what’s going on with DDOG and BILL later this week.

What I’m realizing, and this is just my opinion so please come to your own conclusions, is that concentrations in high growth GAAP unprofitable stocks is still incredibly risky, even at today’s markedly lower prices. Cloudflare’s recent shenanigan is proof of this. I hope I’m not scaring people, because realistically there is a good chance I’m wrong. But I’ve had thoughts like this in the past, done nothing, and regretted it. Who knows, hopefully DDOG and BILL and the others will have good/boring earnings reports.

I think in the long term, our unprofitable growth stocks have exciting futures and substantial profits ahead of them.

The stock market in the short term and medium term is a very complicated beast. This is why a lot of wise, successful investors don’t worry about short/medium term and just focus on the long term . This is what worked very well for Tom and David Gardner since the 1990’s. And to refute a lot of what I said earlier in my own post here, it might be wise to take my significant short term fears and cautions as signs that the worst is over. Maybe this is the greatest sign of the coming of the next great bull market, when a software perma bull is finally cutting back. Saul said as much earlier this week about how maybe his discouragement is actually a big time bullish sign that we are out of the worst.

Enphase

Enphase, being a small 2% trial position in my portfolio, is a footnote in this portfolio update relative to what’s going on with Cloudflare and the other B2B SaaS stocks.

As a trial position, it still needs to prove itself to be worthy of my investment dollars, and this quarter didn’t achieve that . It wasn’t a terrible quarter, but I needed to see a strong likelihood that it can continue its past 12 quarters of break neck growth. And what we actually got shows that this is not likely. In fact, it’s pretty likely that 2023 will feature a strong slow down in YoY growth in coming quarters.

They’ve had big turn around years before (like in 2020) , but obviously that is not a very comparable year.

Here’s what I wrote on Saul’s board the day earnings came out:

–Growth was totally flat QoQ, never a good look for any growth company. BUT, as evidenced by their past results and alluded to in prior conference calls, it’s Q1 seasonality (which tends to be a weak quarter), just more intense than usual.

–What is not seasonality, is that they are guiding to just 3% growth for next quarter. Many of you (like me) have probably gotten used to companies that sand bag their guidance big time and trounce their own estimates. Enphase is not one of those companies. Their biggest guidance beat of the last three years is 3%, so I think if you’re being very optimistic, you assume they get to 6% QoQ growth next quarter. If you’re playing it safe, you assume 3%-4%. So half the year gone, and only 3%-4% growth. No bueno.

–The problem is that U.S. growth was -9% QoQ. European sales buoyed overall growth by growing 25% QoQ. But European sales are not a big enough percent of overall sales to move overall revenue growth for the quarter beyond 0%.

–Although analyzing quarter over quarter paints a dark picture, looking at the YoY improvements are eye popping. Net income is up 190% to $147 million from $52 million last year, while free cash flows are up 148% YoY, and revenues are up 65% YoY. That said, it’s hard to imagine there is some big spike in revenue growth coming in Q3 or Q4.

After reading the transcript, I didn’t see anything that made me stop and think that they are due for a big acceleration in coming quarters.

Wrapping Up

This is yet another especially challenging time to be a growth stock investor. I am always optimistic about the long term future for software stocks and growth stocks as a whole. While I would bet the worst is behind us, the truth is that no one can know exactly where we are and what the near term will bring. What is clear is that the underlying fundamentals of revenue growth, high margins, and increased profitability for our stocks continues. So long as that is the case, these companies have a bright future.