Former ambassador and presidential candidate Nikki Halley say that 65 is way too young to retire and Social Security should be adjusted accordingly. She also wants more Medicare Advantage plans.

3 Likes

As someone else said during a debate about the exact same thing about 20 years ago: So, the janitor can’t retire because Lawyers are living longer?

13 Likes

Nikki Haley tells Bloomberg News “65 is way too low” for the retirement age, advocates attaching it to life expectancy

Apart from the fact that 65 is not the retirement age for most workers today, I wonder how far she wants to go with this. Based on life expectancy, men should be able to retire before women, Black people retire before White people, smokers retire before nonsmokers, and poor people retire before rich people. Somehow, I expect that is not what she means.

16 Likes

“Full” Social Security was already adjusted to 67 a couple of decades ago. It was phased in over the years.

8 Likes

As I recall from biology classes, “life expectancy” for humans is the number of years after which 50% of a given cohort will have died. Given that “life expectancy” changes with age, which cohort would one use to determine that “65 is way too low”?

I am a male born in 1945. At birth. my “life expectancy” was 62.9 years. At age 65, my “life expectancy” was 12.6 years. This data is from Social Security’s Period Life Expectancy table in the 2023 OASDI Trustees Report. At age 78, I’ve beat both expectancies.

It might make more sense to start increasing the earliest retirement age to 65 as it was when the original Social Security legislation was passed.

Another option would be to increase the number of years of work history from 35 to 40 to receive the maximum benefit from Social Security.

6 Likes

Nikki Haley tells Bloomberg News “65 is way too low” for the retirement age, advocates attaching it to life expectancy

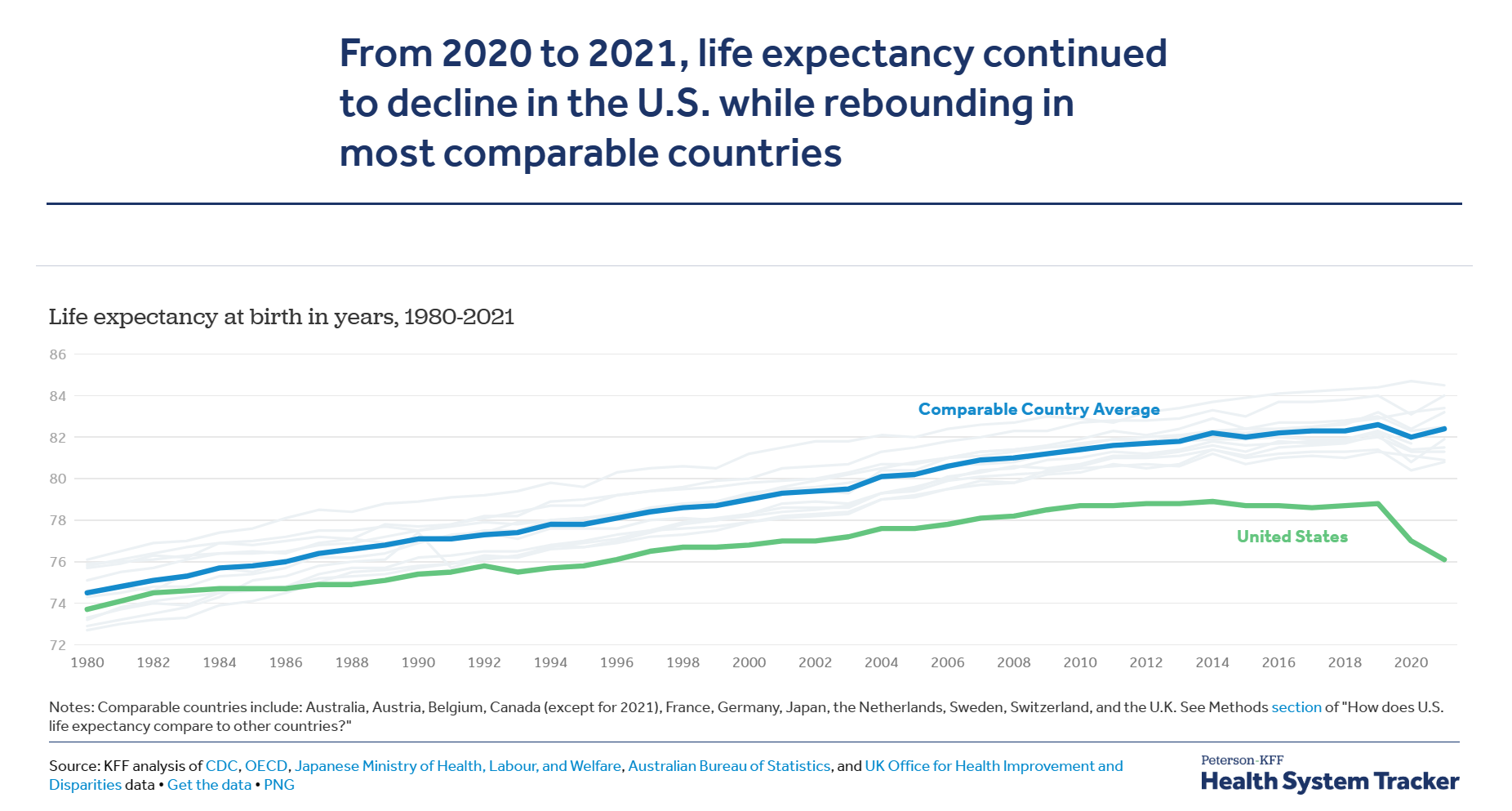

I guess just like all kids are above average and housing prices never drop, life expectancy always goes up in Haley’s world. Got news for her - life expectancy dropped in 2020 and 2021 (the last 2 years we have data for) due, mostly to deaths from COVID and drug overdoses. Why life expectancy in the US is falling - Harvard Health While COVID deaths have decreased, drug overdose deaths have not. Additionally, drug overdose deaths are generally affecting a younger cohort than COVID deaths, so the trend down may not be done.

AJ

9 Likes

Ok but plenty of people are living longer than they used to. Averages are just that.

1 Like

A guy I spoke with at a car show Sunday was sounding off on retirement. He trotted out that old canard about how life expectancy is so much longer than when SS was enacted. He continued that, when SS was enacted, people were not supposed to live long enough to collect.

Nice story. Just isn’t so. The life expectancy he was quoting was from birth. Child mortality is lower now, than 70 years ago. Thanks to OSHA, people in their 20s and 30s don’t get killed off at work in the numbers they used to, before they paid much into SS. Emergency medical care is must better than it was only 50 years ago. People now have a better chance of surviving being young and stupid, and into middle age, when their FICA taxes paid really start to add up.

Male life expectancy in the US, at age 65, in 1940 was 11.9 years. In 2001: 15.8 years. Not that much of a difference.

What people miss in advocating for requiring people to work years longer, before retirement, is whether people are still physically able to do their job when they are 70 or 75. I could do my desk job as well now, at 70, as I could at 58, but an assembly line worker in an auto plant? All that lifting, stooping, and pushing to get the parts together? People wear out after years of that sort of work.

I could put my Simon Legree hat on and redesign the system so that no-one receives SS until they are so broken up and feeble they are useless to an employer.

-impose a work requirement for Medicare, so that able bodied people, regardless of age, are required to work, and continue to have FICA deducted from their pay, to receive the benefit (no employer would want to pay the cost of group medical for people in their late 60s and 70s). Only when certified useless to employers would a person have the work requirement waived for Medicare.

-convert SS to disability only, regardless of age. People who are able bodied are denied SS benefits, which will force many to continue to work, and pay FICA, until they are so broken up and feeble, that the employer certifies them useless.

That I submit, is what the SS “reformers” are looking for: squeezing every last bit of work possible out of people.

Plan Steve, for years, has been to shift SS funding away from it’s current model, based on the pay of a shrinking workforce, working for progressively lower wages, to something that is actually growing, like GDP.

Steve

7 Likes

Well, looking back, luckily for myself, 62 was available as Lucent was heading down the drain, and they made an ‘Offer’ to reduce the National workforce. I jumped on it atone quite 62, DW was still working, so a little tight for a while, but we survived. I can’t see, knowing the work involved, that I’d have made it to, at that time, for me 65+8 months… It would have meant living out of a suitcase, on the road, most likely out of state, and most to the talent, other talent, had already bailed… It was time… Raising it to 70, no way…

4 Likes

Not as many as did in 2019 and before. And if you look at the data for the US, in 1980, life expectancy was only slightly below the average for comparable countries (UK, France, Canada, Australia, etc.) How does U.S. life expectancy compare to other countries? - Peterson-KFF Health System Tracker Since then, the average life expectancy for the other countries has increased at a much faster rate than the US. Additionally, the drop in the other countries in 2020 was much less significant, and rebounded in 2021.

Yes, and the US average certainly isn’t keeping up with the rest of the developed world when you look at average life expectancy.

AJ

5 Likes

In the context of retirement planning, retirees still need to plan for 30 years of retirement rather than the 12 years of retirement 50 years ago.

The averages matter in total costs for Social Security, nursing home capacity, etc, but Not so much for individuals.

Was “planning for (X) years of retirement” even a thing in the past? 50 years ago, many people, certainly those working for a large company, had a company paid, defined benefit, pension, and company paid retiree supplemental medical. 30 years ago, it became acceptable for employers to welch on those promises to the people who had given 20-30 years of their life to the company.

The best known, was McDonnel Douglas, who cut off the retiree medical, for all their non-union workers, with no grandfathering. The first company I worked for after graduating college, in the late 70s, had a company paid, defined contribution, pension, and company paid retiree medical. Those benefits were taken away in the early 90s. “Givebacks” became common in the early 90s: employers demanding workers accept pay and benefit cuts. I remember one worker commenting “It’s like the Community Chest. Every year, they are back for more”.

When GM and Chrysler were bankrupt in 09, the workers agreed to a broad slate of concessions, to help the company survive. Entry level pay at the big three, now, is $10/hr less than it was in 2007. People hired since then do not have a pension, do not have retiree medical, do not have a COLA, on top of their short pay. With the companies booking record profits, the union is negotiating to regain what was taken away in 09. Stellantis’ response is to demand cuts to employee medical coverage and cuts to the employee’s profit sharing.

Working people, now, certainly are on their own, when it comes to retirement. The “three legged stool” of retirement is looking like a post now: the company pensions have been taken away. It is increasingly hard to accumulate personal savings, due to short pay. That leaves SS and Medicare as the only remaining support for many people.

Steve

5 Likes

I am in complete agreement with the idea full retirement needs to be moved to older age. But there is another issue. Over the years the “age of retirement” has declined a lot. The obvious one is taking benefits before the full retirement age. Another is adding disability and other benefits to the system.

3 Likes

"When GM and Chrysler were bankrupt in 09, the workers agreed to a broad slate of concessions, to help the company survive. Entry level pay at the big three, now, is $10/hr less than it was in 2007. People hired since then do not have a pension, do not have retiree medical, do not have a COLA, on top of their short pay. "

And yet the prices of new vehicles march ever higher, despite less money & benefits being paid out to labor. But we’re all kind of between a rock and a hard place, as the cost of used vehicles is too high ( in many cases ) to make them a viable alternative.

Not sure how I’m going to approach my next purchase, been buying new and driving them for about 10 years. Very much in the travel/go-go years, so the reliability is very important, but I can see getting priced out of the new vehicle market sometime relatively soon.

2 Likes

You seem to be using the life expectancy at birth to define how long of a retirement to plan for. That would be poor planning, since even in 1970, (53 years ago), the ‘average’ life expectancy for a 65 year was 15.2 years - meaning that half of the 65 year olds would have a retirement that was longer than 15.2 years. That would mean a prudent planner should have been planning for at least a 25 year retirement, if not a 30 year retirement, even at that time. Given that prior to 2020, US life expectancy was still increasing, even if not at the rate of the rest of the developed world, I would argue that currently planning for a retirement to age 97 (FRA + 30 years) may not be enough.

That said, retirement length is also highly dependent on the age that one retires at. As has also been pointed out in this thread, many people are retiring before they reach 65 - so even if they are only planning for FRA + 30 years, if they retire at 57, they have a 40 year retirement to plan for.

Edited to add data source for historic life expectancy Life expectancy at birth, at 65 years of age, and at 75 years of age, by race and sex (cdc.gov)

Exactly - one’s particular circumstances are critical to retirement planning.

AJ

7 Likes

That’s true BUT higher income people have enjoyed most of the gains.

Lower income people—those who benefit from Social Security the most—aren’t living much longer than they did in the 1940s.

4 Likes

Yep. If you’re in the top 10% of the income and wealth pyramid, you live at least 5 years longer than the average SS beneficiary.

http://www.equality-of-opportunity.org/health/

intercst

2 Likes

Hey when you become “useless” and they accompany that designation with a package I suggest you take the money and run.

3 Likes

Saw an interview with the head of the UAW last week. He claimed that Mexican autoworkers average about $45/week, but the automakers still want $60,000 for the trucks they build.

Decided to fact check that wage myself. Average for a Mexican assembly line worker is 13,000MXN/month ($773.89 US), with the low end at 6,630 MXN ($394.68). so the union guy was overstating things a bit. Seems the entry wage for a Mexican line worker is under $100/wk, but not as low as $45, unless management takes a really big bite out of his gross pay.

Escalating prices is the thing to do at auto manufacturers now. Items on the news wire have reported Ford has dropped the bottom trims of both the Maverick and Bronco, which will, of course, push ATP higher.

2 Likes

SS is for lower quintile earners who can’t save enough for their retirements. Keep it fully funded and expect the rest of us to save extra for our own retirements. I am investing my SS checks at the age of 67. I don’t want to force the poorest of us to have to work till they die just so that I can die a little bit richer.

5 Likes