https://www.wsj.com/tech/ai/is-openai-becoming-too…

Is OpenAI Becoming Too Big to Fail?

Sam Altman’s ability to intertwine the startup throughout major tech players puts it at the nexus of a vital part of the U.S. economy

By Tim Higgins, The Wall Street Journal, Nov. 2, 2025

Slowly then all at once, OpenAI became something of a juggernaut that’s hard to fully fathom.

It hasn’t yet turned a profit. Its annual revenue is 2% of Amazon.com’s sales. Its future is uncertain beyond the hope of ushering in a godlike artificial intelligence that might help cure cancer and transform work and life as we know it. Still, it is brimming with hope and excitement.

But what if OpenAI fails?

There’s real concern that through many complicated and murky tech deals aimed at bolstering OpenAI’s finances, the startup has become too big to fail.

Or, put another way, if the hype and hope around Chief Executive Sam Altman’s vision of the AI future fails to materialize, it could create systemic risk to the part of the U.S. economy likely keeping us out of recession…

Already, some are talking about how OpenAI might be the first trillion-dollar initial public offering. … To others, however, OpenAI is something akin to tulip mania, the harbinger of the Great Depression, or the next dot-com bubble. Or worse, they see, a jobs killer and mad scientist intent on making Frankenstein. … [end quote]

OpenAI isn’t a publicly traded company (yet). But the tech companies that are investing in OpenAI are driving the S&P500 index which many METARs are invested in.

https://www.wsj.com/finance/stocks/tech-earnings-l…

What Investors Learned From Tech Earnings, in Charts

The so-called Magnificent Seven make up a record 38% of the S&P 500

By Hannah Erin Lang, The Wall Street Journal, Nov. 1, 2025 8:30 pm ET

Big Tech is driving big swings in the stock market.

Investors this past week finally got a look at earnings from some megacap technology companies—and their artificial-intelligence spending spree—and found a mixed bag…

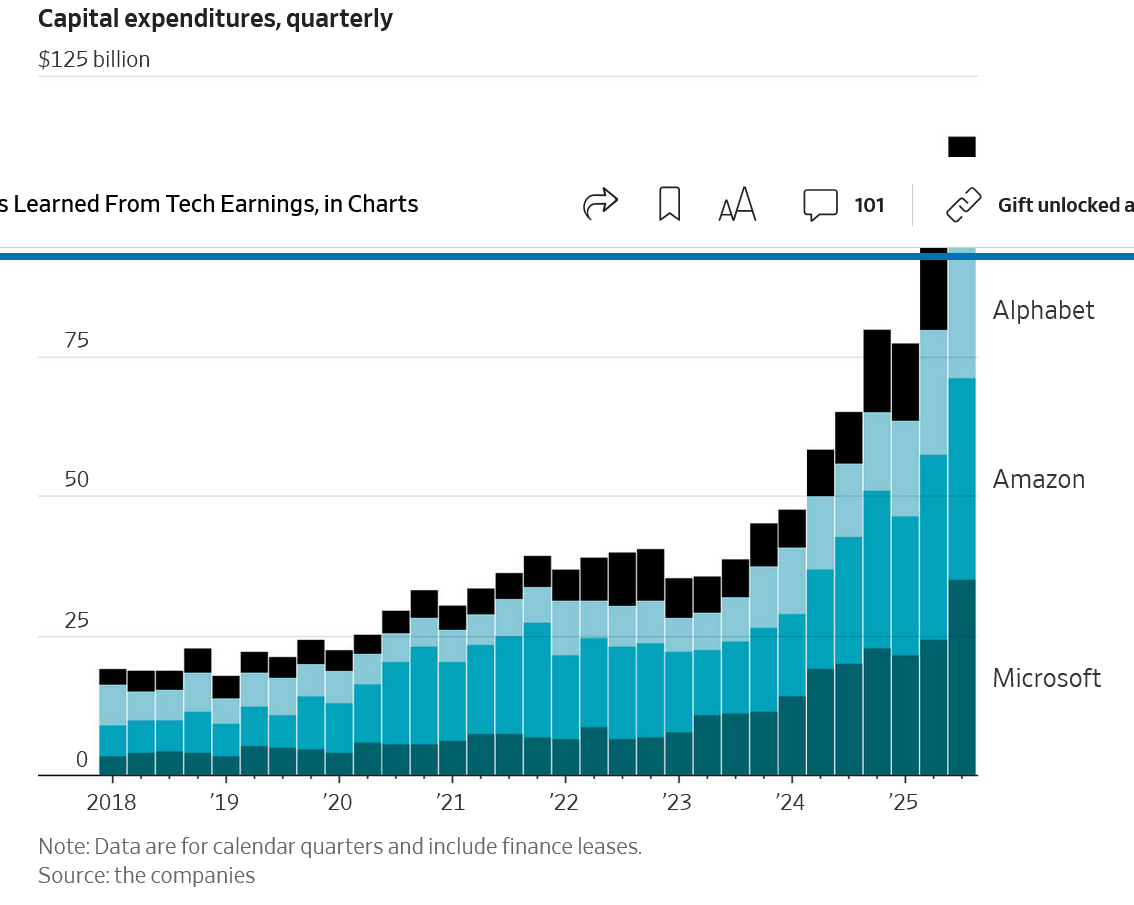

Leading tech companies have already poured hundreds of billions of dollars into their AI efforts—but that bill is only going to get bigger next year. This past week, Meta, Alphabet, Microsoft and Amazon all told investors that they will increase spending in 2026.

The concern among some investors is that it is unclear how, and when, all that investment will start to pay off. The size of the boom implies that a massive shift in the economy would be needed to make current spending worthwhile…

Both Meta and Alphabet reported record revenues this past week.

But all the AI spending is starting to take a toll: The 12-month cumulative cash flow for Meta, Alphabet, Microsoft, Apple and Amazon has dropped in the past couple of years…Once known for holding giant piles of cash and relatively little debt, tech giants have changed in recent years. While they still hold plenty of cash, they have added debt to fund share buybacks, and more recently have started borrowing heavily to fund their AI investments. … [end quote]

The inflation of the AI bubble is based on debt. Even the cash-rich Magnificent tech companies are borrowing to fund their growing investments in AI with quarterly capital expenditures growing exponentially since 2023 to a breathtaking $110 billion in 2Q2025.

The stock market bubble is also driven by debt with Debit Balances in Customers’ Securities Margin Accounts growing 38% between September 2024 and September 2025 (to a record $1,126,494 Million - this blows my mind!).

When the bubble pops there will be a ferocious storm of margin calls which will drive the entire stock market down as speculators sell everything to raise cash.

The Chicago Fed’s National Financial Conditions Index (NFCI) which provides a comprehensive weekly update on U.S. financial conditions in money markets, debt and equity markets, and the traditional and “shadow” banking systems shows that financial conditions are very loose.

As expected, the Federal Reserve cut the fed funds rate by 0.25% but said that the predicted December cut may or may not happen. The options market now has a 66% probability of a December cut to 3.50% - 3.75%. The CPI was 3% and all inflation predictions are for no relief so the Fed shouldn’t cut the fed funds rate. However, the job market is slowing (though not losing jobs) so the Fed has a potential reason to cut. Of course, President Trump has put tremendous pressure on the Fed to cut.

The Fed also announced that it is stabilizing its asset base and will no longer be allowing longer-term Treasuries and mortgage bonds to roll off. That will remove the Fed’s impact on longer-term Treasury yields.

Treasury yields are beginning to rise again. The Treasury yield curve is positive between 2 and 20 years.

The stock market is still in a rising trend though it pulled back a little because of the Fed. The Fear & Greed Index is in Fear.

Gold, silver and bitcoin pulled back a little. USD rose.

President Trump met with China’s President Xi last week.

https://www.wsj.com/opinion/china-trade-deal-donal…

Lessons From Trump’s China Trade War

Beijing fought back, and it’s hard to see what tariffs achieved for the U.S.

By The Editorial Board, The Wall Street Journal, Oct. 30, 2025

President Trump and Chinese leader Xi Jinping struck their third trade truce in a year on Thursday, and the best we can say is that the deal averted more economic damage. Mr. Trump called the deal a “12 out of 10,” but markets were nearer to the truth when they yawned. The deal mostly restores the status quo that prevailed in May…

Mr. Trump has tariffed China, Japan, India, South Korea, the Philippines, Canada, Britain and the European Union… [end quote]

Tariffs are taxes on the consumer. To the extent that importers choose to absorb the tariffs they reduce profits. They are a drag on the economy. They are also inflationary.

Since the government shutdown has close the BLS we won’t know the inflationary impact on the crucial holiday buying season which many retailers need to be profitable. With Trump in power I’m not sure how much we can trust the BLS statistics anymore.

This week’s “Dividend Cafe,” by David Bahnsen, was particularly good and should be read by all investors. Bahnsen stresses that increased rewards come with increased risk. He compares public equity and the bond market with private equity and private credit with a warning about how ILLIQUID private equity and private credit are compared with the liquidity of most investment vehicles in the public markets. This is a critical point also reiterated by Jason Zweig of the Wall Street Journal.

There are no major news stories to upset the markets.

The METAR for next week is sunny but perhaps partially cloudy.

Wendy

https://www.finra.org/rules-guidance/key-topics/ma…

https://www.chicagofed.org/research/data/nfci/curr…

https://www.cmegroup.com/markets/interest-rates/cm…

https://stockcharts.com/freecharts/candleglance.ht…

https://stockcharts.com/freecharts/candleglance.ht…

https://stockcharts.com/freecharts/candleglance.ht…