El Supremo:

Ok - went back and looked for a chart that displayed performance results for the HDO folks for 2008-2009. There are none because HDO was founded a bit later. But here is - and what I think I originally saw on the issue - an article that goes over what would have happened to the HDO portfolio during that time frame - and a similar event - using their holdings when the article was written way back in 2022:

Now - truth be told, I just don’t see any horror story here; just the market doing what the market does, but admittedly, I tend to look at things a little differently and maybe I am missing something. Moreover - I would urge anyone and everyone to read this article. Especially my growth brethren cohort.

Here are a few quotes from the article that may provide leverage for discussion of differing opinions:

"While “Value” stocks like we hold in the HDO Model Portfolio are still outperforming year-to-date, they are down nearly 18%. This is an amount that a lot of people get concerned about. Yet in the stock market’s history, this is not an abnormal event. Bear markets come around from time to time, and through your investing career, you will see several of them.

For the S&P 500 and the Nasdaq, this is the deepest bear market since the Great Financial Crisis. For Value stocks, it isn’t as bad as COVID was.

Today, I want to focus on dividends. Share prices will do what they do. Will the market recover next week? I don’t know, and frankly, I don’t care. The market will recover eventually. Until it does, I’ll focus on growing my income and buying dividends while they are on sale. As far as I’m concerned, prices can stay low for the next few years.

I’ve seen many comments asking about dividends in relation to the share price. Questions like “what use is a dividend if the price is down X%?”. Today I want to answer that question in-depth and include some backtesting analysis of the Income Method using Portfolio Visualizer.

I preach about focusing on income. Today, I want to pursue more deeply why I am such an evangelist about income investing and why swings in market prices really don’t faze me at all."

"At HDO, a large part of our due diligence is determining whether a company is outearning its dividend. We aren’t interested in high yields from companies that don’t have the earnings to support them. We look for companies that are covering their dividend and can reasonably be expected to cover their dividend from earnings.

In other words, we are looking for dividends that stem from profits earned by the company.“Sometimes, there will be “black swan” events that can put a normally safe dividend at risk. COVID was an example of that, as numerous companies saw their revenue plummet almost overnight. During that period, many dividends that could have been considered solid in late 2019 were cut. Yet black swans are called black swans because they are very rare.”

"The instability of prices and the relative stability of dividends is why I created The Income Method. Prices are temporary, they come and go. Often the price changes before I can even place my buy order! How rational is it to base your performance on something that changes every second that the market is open? "

"Forget “beating the market” – this isn’t a game for me. I’m not out to be like a star athlete, winning for the sake of winning. Whether someone out there makes more money than I do in the market does not impact my life. My goal isn’t to have “the most”. It is to have enough to support the lifestyle I choose to live. I can live perfectly fine knowing that I didn’t get the highest score in the market game. If I don’t have the cash I need to support the lifestyle I choose, now we are talking about something that impacts my quality of life.

When I think about it, there are a few facts to use as my base:

- Prices change, and I can’t predict what they will be in the future with any significant precision.

- My cash needs in retirement are not a single lump sum. I need recurring and preferably growing cash flow.

- I can’t predict how long I will live with any significant precision.

I need cash flow, not some random sum of money. My goal is not to have $1 million, $5 million, or $10 million. Such a goal doesn’t even make sense because if I live to 75, the amount of money I need is very different than if I live to be 100.

Why would I set a goal at some random dollar amount? I don’t know how many dollars I will need. I don’t know if inflation will average 1%, 2%, or 5% over the next 30 years. I don’t know if I will live for 30 years. I could guess at these values, relying on historical averages and life expectancies. Maybe my guess will be close, but I don’t want my future to rely on a “guess”.

So instead of making my goal to have $X million in my portfolio, my goal is focused on my annual dividend stream. Even when the market is down, I can look at my income stream and see whether I am closer or further away from my goal. Often, I am closer to my goal even when share prices are down."

And now we get to the meat - an example of a HDO holding during the Great Financial Crisis and for Covid. Note: Plot Reveal Follows:

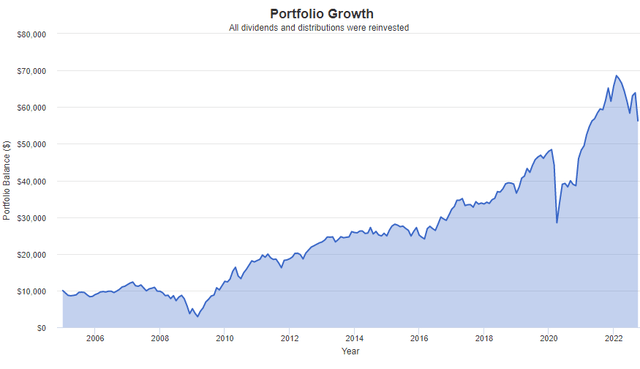

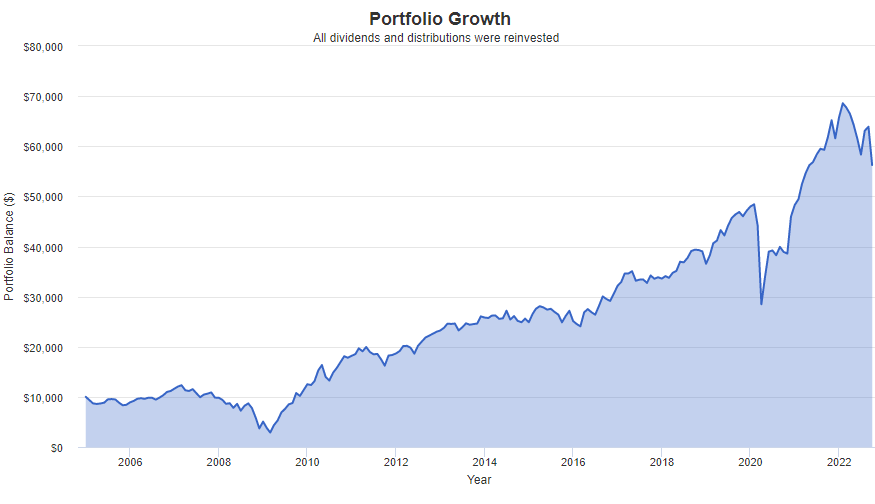

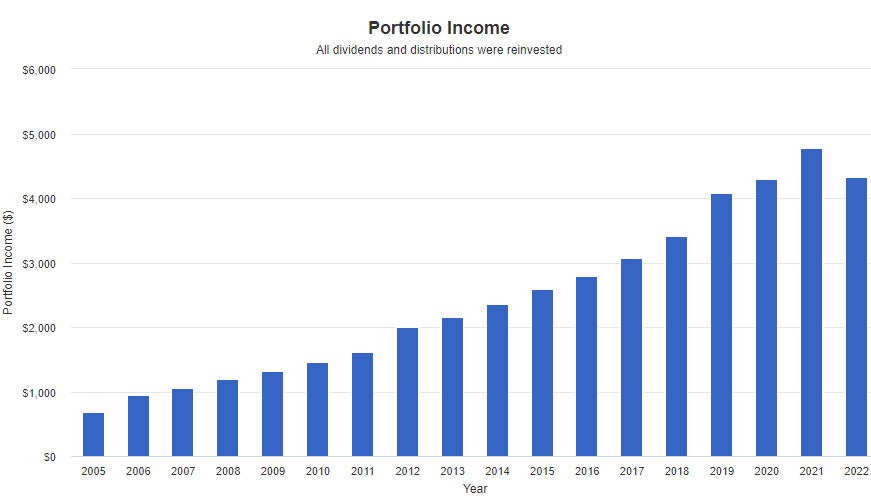

Consider one of HDO’s longest-held holdings, Ares Capital (ARCC). The top graph is the changes in price, with reinvestment of all dividends, and the bottom graph is the income. (Source: PortfolioVisualizer)

Note that the price declined over 80% during the Great Financial Crisis. It was relatively flat for many years and crashed 40% again during COVID. You likely panicked during those years if your goal was to get to a lump sum. In both cases, you lost about 5 years of progress in terms of portfolio value.

If your goal was income, from 2007 to 2009, your income increased 26%. Note that this increase occurred despite a 17% dividend cut in 2009. The reason for this is that reinvesting at lower prices drives future income upward.

In hindsight, there was no reason to panic about ARCC during the Great Financial Crisis, nor was there a reason to panic during COVID. In both cases, the price eventually fully recovered, but when ARCC went from $20 to under $5, many investors panicked. When it went from $19 to below $10 during COVID, they panicked again. After all, that was “6 years of dividends just to get even!”

Investors who focused on the income saw that being able to reinvest in ARCC at 30% yields was the bargain of a century. The price for ARCC has been all over the place, the income has steadily climbed.

By focusing on the income, investors got a clearer picture of how their investment was actually performing. By setting an income goal, as opposed to a value goal, investors can rely on a much more consistent measurement. Price varies wildly from year to year, while income doesn’t, even through very difficult times."

And now the final act:

After setting the table with all that - we get to the Bottom line: Man to Man combat - a sort of Grand Finale on performance results vs theory and ancillary opinion during the timeline in question. But you’ll have to read it - posting it here as a quote just won’t have the same impact as reading it. But if you want to save time - well, as Patton once said, “We’re gonna grab them by the nose and kick them in the a**”. Or…alternatively, as that great philosopher Shakira put it:

Evidently - neither hips nor performance results lie.

Lastly, If you do read this article - and I realize you are a busy man and your time is limited; but if you do/can take the time to read it - then perhaps we can get past the cryptic lunch thingy comment and focus on specifics within the strategy that you find quarrel with. That would be wonderfully valuable, respectfully appreciated, and overwhelmingly worth the price of admission to this subject.

All the Best,

BDH Investing

ft. Wyclef Jean")