This Enphase thread is 40 posts long, so perhaps I am beating a dead horse here. But if people are interested in one more take, here’s what I have:

What does Enphase do?

Enphase, per the investor relations page, “is a global energy technology company and the world’s leading supplier of microinverter-based solar-plus-storage systems.”

Jargon alert - what is a “microinverter”? A microinverter is a plug-and-play device used in photovoltaics, that converts direct current (DC) generated by a single solar module to alternating current (AC). The output from several microinverters can be combined and often fed to the electrical grid.

Enphase investor relations continues, “The Company delivers smart, easy-to-use solutions that connect solar generation, storage, and energy management on one intelligent platform. Its semiconductor-based microinverter system converts energy at the individual solar module level and brings a system-based high-technology approach to solar energy generation, storage, control, and management.”

In my own words, the company enables many pieces of the “solar energy experience”. Their microinverters help you generate solar electricity, their batteries help you store it, and their software helps you manage the system as a whole.

Financials and Why I’m Interested

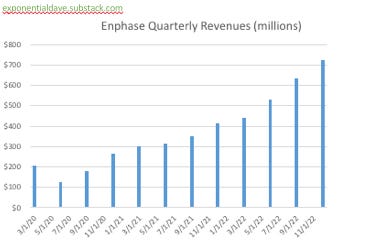

Why is this stock interesting to me? Its past and recent financials are nothing short of phenomenal. Its Q1 2023 revenue is expected to be more than double its Q1 2021 revenue ($740 million vs $300 million). And its Q4 2022 revenue was more than 6x higher than its Q2 2020 revenue. I did a little cherry picking there, but in general it is clear they are enjoying break neck revenue growth.

I mentioned earlier Enphase is GAAP profitable. GAAP profits are up 91% YoY for its most recent quarter to $311 million, and roughly triple what they were in 2020. Free cash flows are strong as well, with FCF’s of $237 million, up 183% YoY and orders of magnitude higher than they were a few years ago.

And the icing on the cake is that gross margins have improved tremendously over the last six years. In 2017, gross margins were a measly 13%, by Q1 2020 they had improved to 39.5%! And most recently, at the end of 2022 they were 44%. I don’t think we can expect more huge margin increases, but nevertheless the company is scaling very impressively.

And a quick look at leadership: I like founder CEO’s with large insider holdings of their own companies, and while CEO Badri Kothandarama is not the founder of Enphase, he has a 1.8% stake in the company. At the company’s recent $25 billion market cap, his stake is worth $500 million, quite a few reasons for his interests to be aligned with shareholders! Additionally, Badri is an accomplished engineer with more than a couple of patents under his belt.

What are the risks?

Although I see a lot to like about this company, I think a lot more caution is warranted than with other companies that I typically invest in, because this is very much not a company I typically invest in. There are a number of risks I’d like to know more about before I would want a concentration in Enphase.

Although software plays a part in the company’s business, the key part of their business is their creation of widgets, in this case the microinverter and the batteries. This means there is risk related to:

-

Raw materials - it takes many different suppliers and materials to make microinverters and batteries. Some of the minerals used by Enphase’s suppliers are “conflict minerals”. According to google, a conflict mineral is when “armed groups use forced labor to mine minerals, and they then sell those minerals to fund their activities, such as to buy weapons”. This poses investment risk, increased government intervention risk, as well as ethical concerns. I’m not here to shame anyone for buying a stock, but I would advocate that if this stock turns into a home run, consider donating some of the proceeds to a charity group that focuses on those affected by conflict minerals.

-

Labor risks - (Enphase relies heavily on contracted labor to do manufacturing).

-

Supply chain - this was all people talked about in 2021 and early 2022 due to the pandemic, but so far this year, it has not been a notable issue.

And because this is an energy related investment, there are also risks related to:

-

Commoditization of solar energy - Energy being a commodity, costs should come down over time, which can erode margins. People have to be able to afford energy, unlike, say iPhones, which are not a basic necessity and so can charge whatever they want.

-

More viable energy sources - (cheapening of natural gas, more availability of nuclear, etc) can cause a decrease in the relative value of solar energy.

-

Unfavorable changes in government policies , such as removal or lessening of subsidies or an increase in tariffs (both domestic and abroad). Enphase found itself affected by the Trump tariffs (that Biden largely continued) intended to punish China for unfair trade policies. Enphase has also benefitted from the IRA (inflation reduction act, which might sound a little confusing - why would Enphase benefit from inflation reduction? Because a lot of the bill had nothing to do with inflation). Benefits could be diluted or taken away entirely if politicians unfavorable to green policies get voted into office in the next couple of years, or if the supreme court finds some or all of the IRA to be unconstitutional.

Enphase will also likely be negatively affected by California’s latest net metering policy, NEM 3.0, despite the company saying it will be a positive. I have more details on this in the conference call excerpts section towards the bottom of this report.

- Geopolitical risks , related to and perhaps a continuation of #7 above**,** including a deterioration in relationship between the U.S. and the Chinese Communist Party (CCP). Enphase batteries are made there, and it seems like most days I hear about further relationship strains, such as Xi Jinping announcing his unbreakable “friendship” with fellow authoritarian/super villain Vladimir Putin.

Also, Enphase mentions starting production in Romania this year, a current NATO member and former member of the Soviet Republic which shares a large border with Ukraine. Hopefully the Ukraine war ends soon or at least is contained to Ukraine, but conflict could certainly spill over into Romania and possibly affect Enphase’s production there.

A couple risks that I am more familiar with (because we see them in our software investments) are:

-

Better mouse trap risk : another company could come along with better microinverters (or something that makes microinverters obsolete), better marketing, quicker/better ROI, etc.

-

TAM (total addressable market) risk : Enphase may have already gotten most of the low hanging fruit of their total addressable market. Growth could stall out in 2023, potentially for longer. The company does not provide annual guidance, so we don’t have a worst case scenario for what growth should be for this year. And for Q1, they guided much lower than usual. There wasn’t a great explanation for why on the conference call either (I provide this excerpt further down in this report).

Diving a bit more into the risk of slowing revenue growth, even if you are more interested in profit growth, Enphase’s profit growth has historically been very correlated with revenue growth. So if revenues aren’t going to grow, it might be a big leap to expect them to find ways to grow profits without growing revenues, but of course it is possible.

And many of you would rightly point out that, guidance is not to be taken too seriously most of the time because the best companies tend to strongly exceed their guidance. What I’ve learned in my time studying the best companies, is that each management takes a different approach to guidance. Looking at Enphase, I can see that they have never been a company to trounce their own guidance. At most they beat by about 3% QoQ, and that is pretty rare. They’ve also had more than one small guidance miss. What I conclude from this is that revenue growth really is likely to slow a lot in Q1 of this year.

Will this growth slowdown continue through the rest of the year, or is it a blip? It’s really anyone’s guess, as they don’t give full year guidance. My best guess would be that it’s a blip, not to be taken too seriously. I likely intend to keep this position under 5% for the foreseeable future (probably under 2% barring special circumstances), so it may get a slightly longer leash than a big concentration would. But if they keep guiding to little or no growth, you would likely see me making a quick exit.

A quick look through the financials of Enphase will assure you that, whatever risks they are facing, they’ve done a darn good job mitigating them! However, that does not mean these risks aren’t there. And yet, all investments come with risk, mostly of the “very hard to actually quantify” type. As in, what are the odds it ends up being material that Enphase manufactures in China (lots of successful companies do it), or that revenue has gotten too close to its TAM to continue hyper growth, etc? It is ultimately up to you to decide what sort of risks you are comfortable with in your portfolio.

Excerpts from the latest conference call:

“We are excited to service the U.S. customers better with local manufacturing. We plan to begin U.S. manufacturing of our microinverters in the second quarter of 2023 with a new contract manufacturing partner and in the second half of 2023 with our two existing contract manufacturing partners. We plan to open 6 manufacturing lines by the end of this year adding a quarterly capacity of 4.5 million microinverters, bringing our total quarterly capacity to more than 10 million microinverters as we exit 2023.”

XD: Some quick math here – they are expanding their capacity from 5.5 million to 10 million, an 82% increase!

“We are on track to begin manufacturing at Flex Romania starting this quarter, enabling us to service Europe better. This will enable a total quarterly capacity of 6 million microinverters exiting Q1.”

XD: I see anything that diversifies Enphase’s supply chain as a positive, although I would prefer if the facilities were a bit further away from Ukraine.

“Our GreenCom Networks acquisition, which closed in the fourth quarter helps to integrate Enphase microinverters and batteries with third-party EV chargers and heat pumps, enabling homeowners to control their devices from one app, which is the Enphase App. ”

“Let’s now cover the U.S. We expect our U.S. business to be slightly down in Q1 compared to Q4, primarily driven by seasonality and the macroeconomic environment. We are seeing that our distributor and installer partners are a little more cautious in booking orders . We normally have a 6-month order visibility and that has been somewhat reduced as our partners watch their spending closely. On the sell-through of our microinverters, while December was quite strong for us we saw a more pronounced seasonality in January than normal.”

“The basic thesis ongoing solar and storage remains intact, aided by a few factors: first, the utility rates, which are rising in many states across the U.S.; second, the 30% ITC tax credit, which has been extended for 10 years with the IRA; and third, the desire for energy independence and tackling climate change. ”

XD: This above details out some of the long term tail winds Enphase can ride. For those of you new to this stock, ITC just stands for investment tax credit.

“We also expect to start ramping our third generation IQ battery in North America and Australia in the second quarter. This battery has got 5-kilowatt hour modularity, 2x the power compared to our existing battery and 30-minute commissioning time in addition to being easier to install and service.”

“Next, I’d like to comment on NEM 3.0 in California. The CPUC has finalized its decision on NEM 3.0 in Q4. While we wish the export rates had been stepped down a little more gradually, the policy is generally in the right direction for incentivizing homeowners to adopt storage.”

analyst: “But based on some of the conversations we’re having in the industry, it seems like there is a fair amount of tumult and challenge out there with trade credit being pulled back and some bankruptcies and just some challenges out there.”

Badri: “Yes. I mean, look, seasonality has always existed in the solar industry from Q4 to Q1. And historically, I would say that, that seasonality is a 15% number. That means, in general, the sell-through in Q1 is usually 15% down compared to the sell-through in Q4. Now right now, and I’m giving you a lot of data from January, and that’s the data we have. Our Q4 was very strong, including December. January, we start to experience a little more than 15%. That’s why I said more pronounced seasonality. And of course, we think it is due to the macroeconomic environment, but what we saw interestingly was the activations remain the same. I mean approximately and they were a little bit down they didn’t have that much of a seasonality.

So that basically was somewhat good because the customer demand at least whatever we saw was – I mean, did not get that much affected. But having said that, I think the installers are quite cautious. Therefore, they basically are only buying what they need from their distributors, which is a stark difference from 2022, where they were focused on supply. They were focused on maximizing what they had in their warehouse. Now is that they are worried about their spending, they are worried about their OpEx, they are worried about their cash flow. Therefore, they are going to make sure they do exactly what is required.”

XD: This was probably management’s best attempt at explaining why their guide is so weak for Q1. He is right that there is seasonality between Q4 and Q1 (there is usually a big drop in the QoQ growth rate), but it is more pronounced than last year’s.

“Now on talking about NEM 3.0 in general. NEM 3.0 is going to be incredibly positive for us. Because NEM 3.0, I mean, just so everybody gets it, I’ll talk about NEM 3.0, the features of NEM 3.0. Basically, the – previously, the import and export rates were the same. So therefore, when you exported electrons with the solar system didn’t really matter. As long as you exported, it got directly subtracted from what your input. That’s why it’s called net metering, and that was net metering 2.0. With NEM 3.0, it matters when you export these electrons. So you have 24 hours a day, 365 days a year. So basically, 8,760 data points, and there is an export rate for each of those data points. Each of those hours, there is an export rate. And – but what it works out to be is if you are interested in a pure solar system, your payback dropped understandably from, let’s say, 5 years, it increases actually to something like 7 or 7.5 years with the pure solar system. But the moment you add batteries, you can add batteries in steps of 5-kilowatt hour, 10-kilowatt hour, 15-kilowatt hour, the moment you add batteries, that payback comes right back in to that 5 to 6-year time, to that 5 to 6-year period. That is the stock difference with NEM 2.0. With NEM 2.0, the grid was the battery. Batteries didn’t have an ROI because batteries were primarily for resilience only. With NEM 3.0, batteries are going to be financially attractive. But it is complex. NEM 3.0 is definitely complex. So the installers need to demystify it for the homeowners.”

XD: I had never heard of net metering before Enphase, and I’m sure many of you are in the same boat. This was my introduction to it, and frankly I didn’t find Badri’s summary all that helpful.

For an explanation of NEM 2.0, I found this site helpful: Customer Generation

And for NEM 3.0: What is NEM 3.0 and How Will it Impact California Solar Owners? | Solar.com

I think the most important thing to know here is that California, which is a significant portion of Enphase’s business (later in the call they confide that it is 20% of their total revenue), is switching to NEM 3.0, and under NEM 3.0 solar systems will receive 75% less money on average for each KWh. So this lowers the incentive to get a solar system and is clearly not “incredibly positive” for Enphase, despite what Badri is trying to spin.

analyst: “And then secondly, if I just look at your numbers, battery volumes for your shipment guidance in Q1 will be down year-on-year for the first time since you guys started breaking that out. So, batteries all of a sudden don’t look like they are growing for you. What should we be thinking about for the next few quarters into the back half? Like does NEM 3.0 drive growth again, or is this a sort of more uncertain period of battery growth at least in the next couple of quarters until, again, the market kind of figures it out.”

Badri: “We think you should think that NEM 3.0 is going to be great for us. We are going to be growing with – along with NEM 3.0, we are going to be growing. In addition, we are going to be growing outside California too, because I am not sure whether you cut the color on what I have said, the – we are working on the battery transition right now”

XD: Badri plays defense and goes back into spin mode after a sharp question from an analyst.

“We basically told you that the revenue mix between U.S. and international is 71% and 29% and most of our international revenue is Europe.”

Conclusion and Final Thoughts

In the bull case for this company, the three straight years of stellar financials are the forest, and the litany of risks from NEM 3.0, tariff wars, manufacturing in China, conflict minerals, and a weak Q1 guide are just distracting little trees. They appear to be intelligently navigating their risks and growing their business tenaciously.

Everyone should come to their own decision, but for me, I’d like to either keep the company as a small allocation (under 5%, probably under 2%) to watch, or just add it to the watch list and check in after Q1 comes out.

However, if they resume strong guidance for Q2 and have a strong Q1, this stock will likely bounce up very quickly. People would find themselves wishing they bought in beforehand.