Annual inflation heated up slightly in September, but not as much as economists expected, giving the Federal Reserve a clear path for widely expected rate cuts heading into their remaining meetings this year. ..

September’s reading keeps the Fed on track to cut interest rates again at its meeting next week as policymakers grapple with a slowdown in hiring. If this milder-than-expected pace of price growth continues, it could soften resistance to rate cuts from officials who have been more anxious about inflation…

The White House said on social media Friday that the shutdown means there likely won’t be a report on October inflation, since surveyors who collect price information cannot work in the field…. [end quote]

The markets are front-running the Fed again!

This so-called “lower than expected” reading doesn’t soften MY resistance to rate cuts. Here’s the data.

No CPI numbers next month. What are some alternative sources that measure inflation? There is the Zillow rent index (ZORI), and the Big Mac Index. The bond market is not worried, with a 10-Year Breakeven Inflation Rate of only 2.3%. Right on the FED’s target!

=== links ===

Government shutdown likely means no inflation data next month for 1st time in decades, October 24, 2025

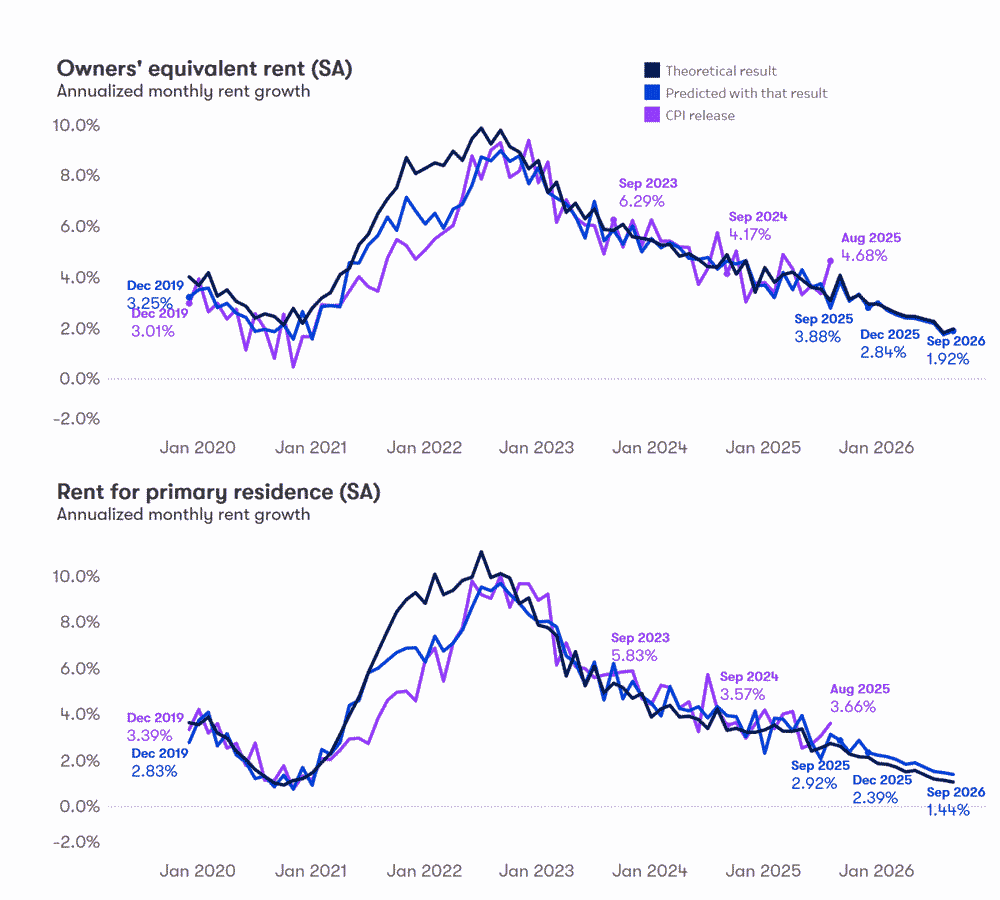

“CPI housing inflation measures should moderate significantly through late 2025 and 2026, driven by a sharp deceleration in market rents over the last few months.” Owners’ equivalent rent (CPI Shelter) is projected to drop to about 2.0% (yoy) in September 2026.

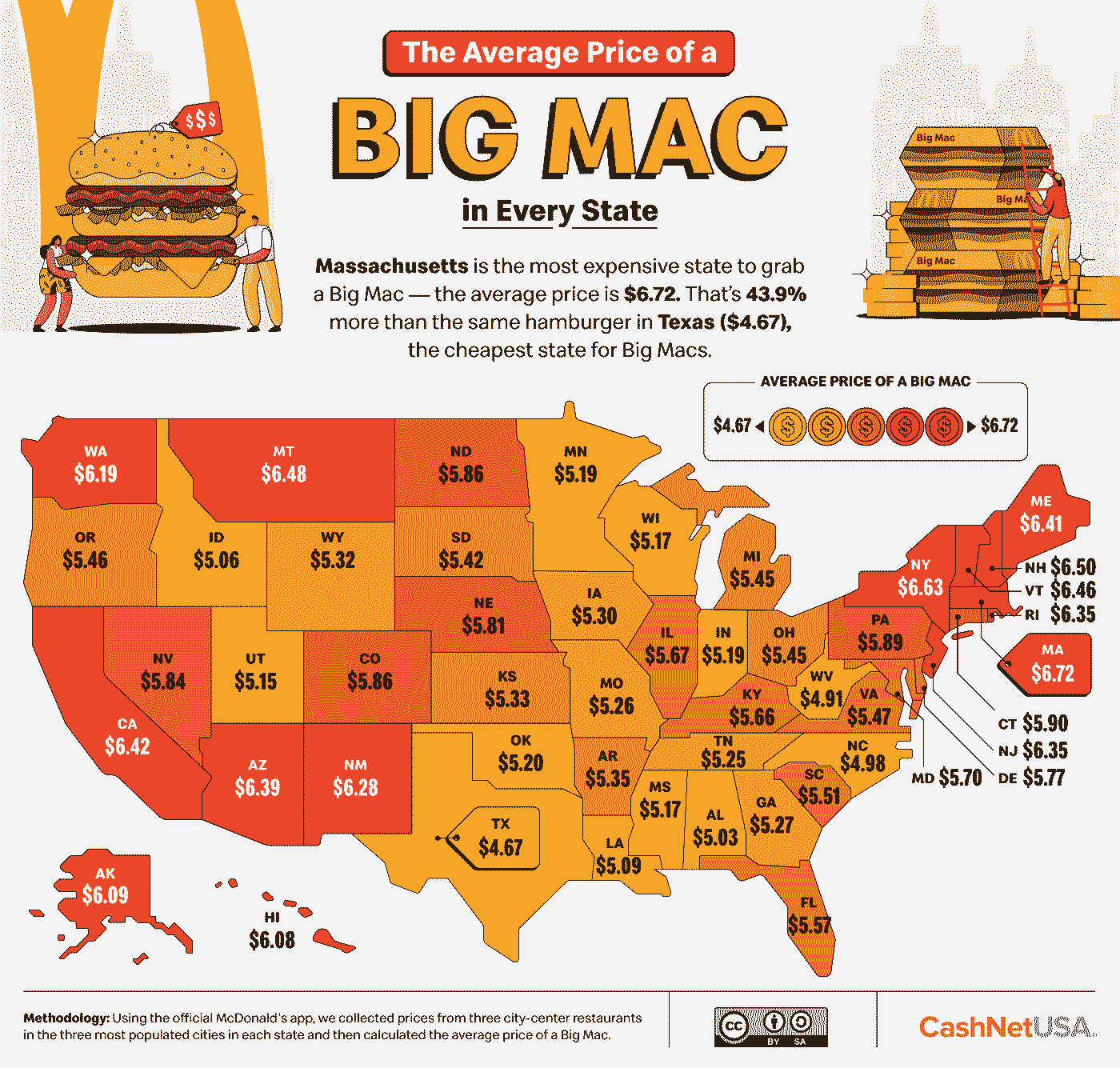

How the Big Mac Index Relates to Overall Consumer Inflation, April 11, 2024

“From January 2018 to January 2021, the two inflation rates move similarly, with both being around 2%.”

AI search for: big mac price 2025

Average (U.S.): Approximately $5.79 to $6.01.

California: $6.42

Maryland: $5.70.

Alaska: $6.09

Alabama: $5.03.

Massachusetts: $6.72.

Canada: $5.43.

United Kingdom: $6.01

Switzerland: $8.17

These prices match the cashnetusa April 2025 numbers.

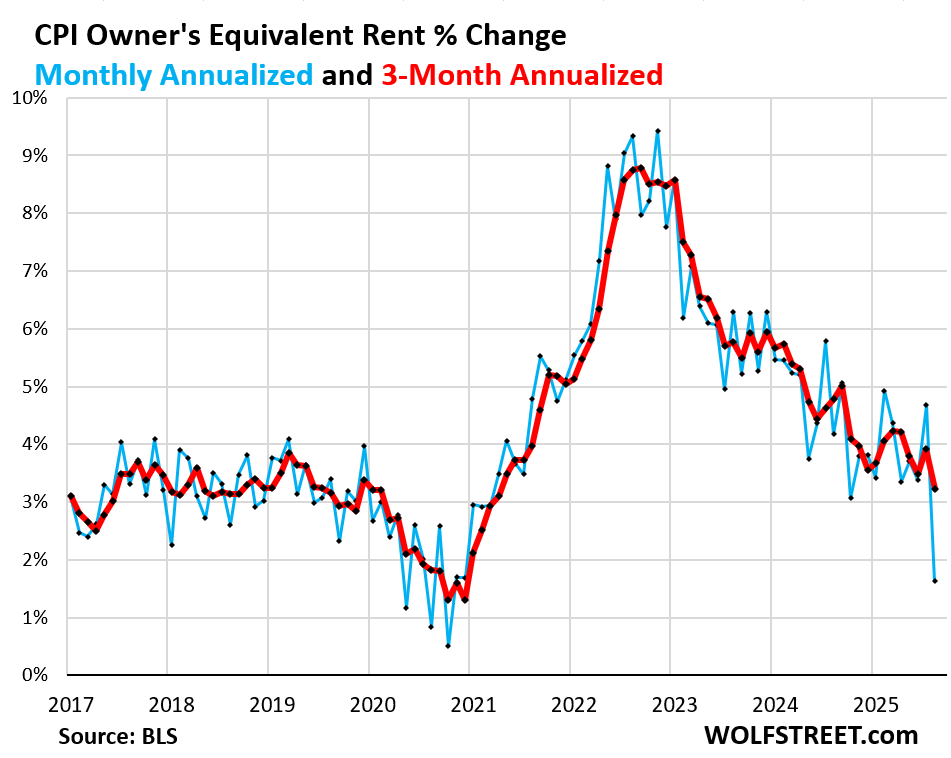

There’s a big error in the inflation report for Owners Equivalent Rent. Also, the report contains no corrections to errors or omissions. These are both signs that the report was produced with minimal effort.

OER rose by only 0.13% in September from August (blue line in the chart), according to the BLS today, compared to 0.38% in the prior month, and compared to the 12-month range between +0.27% (May) and +0.41% (July). Something went wrong there, and given its huge weight, OER significantly pushed down the month-to-month readings of overall CPI, core CPI, and core services CPI.

If this situation with OER hadn’t happened, the inflation readings today would have been a lot hotter than they were, particularly core services CPI where OER weighs 44% and core CPI where OER weighs 33%.

A couple of business writers I follow (subscription site) have been writing now for some time that they expect 3% to become the “new normal” or standard that the Fed shoots for. They gave several reasons why 2% will no longer be the target.

Many thought the markets had priced in Fed rate cuts back in the beginning of October -

“Markets have priced in a 100% probability of an October cut and an 88% chance of another in December. Both are higher from when the lockout began at midnight Thursday.”

Since rate cuts were reportedly priced into the markets 10/1/2025…

The veteran economist says the economy “looks better than it feels” because the very data used to measure it is eroding, and the illusion of resilience could shatter heading into the fourth quarter.

Swonk pointed out that many of the categories holding inflation steady are either insulated from tariffs or benefiting from temporary waivers: computers, smartphones, and some vehicle imports. Once those fade, “goods prices are still moving up,” she said, with few signs of broad-based disinflation. Core services less shelter—a metric the Fed watches closely—rose about 0.4% in September, Swonk estimated, and remains more than 3% higher than a year ago, “well above anything we saw pre-pandemic.”

That stickiness, she warns, is amplified by a bifurcated consumer base, what some economists have called the “K shaped economy.” Affluent households continue to spend freely on travel, entertainment, and premium goods, keeping service-sector inflation stubborn. Lower- and middle-income consumers, by contrast, are pushing back, trading down, stretching budgets, or delaying purchases altogether.