## Calculating Portfolio Returns

I retired in July 1996, so I’ve actually been taking out money to live on for the last 20 years, instead of adding money.

Here’s how to calculate your overall returns ignoring cash flow in or out. Say you start the year with $14,000. You want to equate that with 100% and calculate gains and losses from there. So you ask yourself “What number (factor) would I multiply $14,000 by to get 100?”

By simple arithmetic we have 14000 x F = 100

And thus F = 100/14000 = .0071428

Sure enough 14,000 x .0071428 = 100

Now say three weeks later you have $14,740 and you want to see how you are doing, you multiply that number by .0071428 and you get 105.3 (so you are up 5.3%). If you don’t add or subtract money, that factor will work for the whole year.

Now say you add $2300 of fresh money, but you don’t want that to screw up your estimate of how well you are doing.

You add the $2300 to the $14,740 and get $17,040 which is your new balance that you are investing with. That’s your new starting point. It doesn’t affect how you’ve done up to here. You haven’t suddenly done better because you added money. You can’t still multiply by .0071428 because you’d get 121.7 and it would look as if you were up 21.7%, when you are really only up 5.3%.

So you need to change your factor to make it smaller so it will still reflect just the 5.3% gain you’ve made so far. You figure: “What would I multiply my new balance ($17,040) by to get 105.3, to reflect my 5.3% gain so far this year?”

F x 17,040 = 105.3

F = 105.3/17,040 = .0061795

And that’s your new factor. If you multiply it by 17,040, sure enough you get 105.3. Now you continue to see how you will do for the rest of the year.

If a little later you are at $18,000, you multiply 18,000 by .0061795 and you get 111.2, so you know that your investing is now up 11.2% for the year.

Same, if you take money out. You don’t want it to look as if you lost money. You calculate a new factor so you start from the same percentage where you were.

On January 1st of the next year, you write down how you did for the year to keep a record, and start over at 100 for the next year.

## Dips and Downturns

When the market is in euphoric phase, companies can report poor or mediocre results, but the analysts and investors will find some positive slant to bid the stock up. This will last until it reverses, and then no news is good enough. Whatever it is, the analysts and investors will find some negative way of looking at it, and the stock will go down. So don’t panic at irrational sell-offs. If it’s one stock, then you have to make sure there’s not something wrong with that particular company. When it’s all your stocks and the pundits are all saying the big crash is coming, relax. It’s just something that happens now and then.

Sometimes you can feel shell-shocked from the pounding you get from the market. All your well-functioning, rapidly growing companies, who have had no bad news at all, have sold off sharply for no reason. If the market is down, it will recover. It always does. If anyone says “This time is different, it won’t recover,” you should greet what he says with suspicion. Just hope that the recovery is sooner rather than later.

Remember how scared everyone was at the end of 2008. One financial expert, when asked what positions he’d be in, said “Cash, and the fetal position!” That’s how scared people were. – Well, I was up 110.7% in 2009. The market has now been up for 7 years since then. If I had listened to the doom-and-gloomers at the end of 2008, I’d have been in cash and missed it all.

I wrote this one day in 2014: “Just two weeks ago, people were writing in on the board to ask whether they should sell out of everything and go into cash, long term growth newsletters were taking on “short” ETF’s to protect themselves from a falling market, and someone on this board was suggesting maybe it was the start of a Bear Market. By coincidence, they all occurred on the bottom day for the market. It’s worth keeping that in the back of your mind the next time the market takes a little breather and you get unreasonably scared. If you’re scared, almost everyone is likely to be scared, and we probably don’t have much further to fall.”

My preparations for the next market drop. That’s easy. I don’t try to time the market and I stay fully invested. I try to pick good, really excellent companies, whose stocks don’t have a long way to fall if things turn bad. In other words, companies that have a lot of growth, and whose stocks are reasonably priced with reasonable PE ratios.

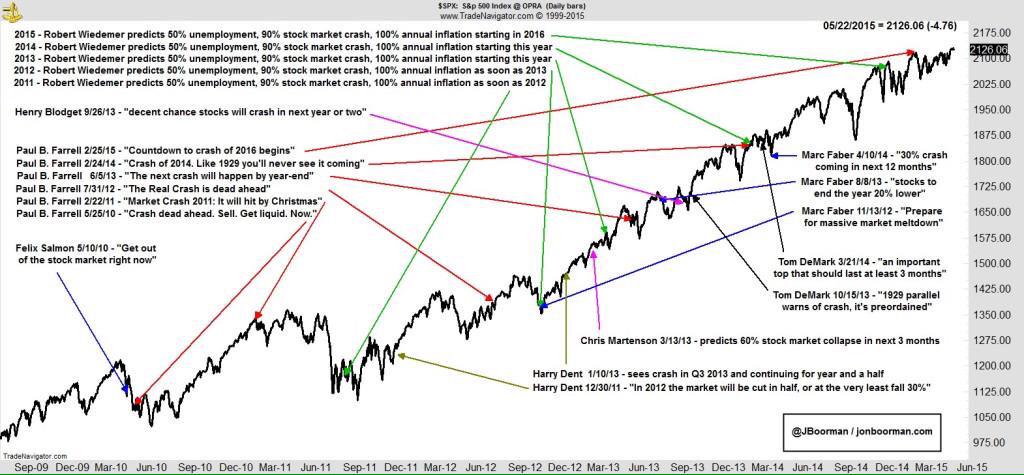

Why don’t I try to time the market? Because the experts can’t do it, so why should I think I can do it. There are people saying “Watch out for a market crash this year!” The only trouble is that they said that last year too, and in 2014, 2013, 2012, and 2011. And in 2010 they were warning about a “Double Dip Recession,” which didn’t happen either. Eventually they will be right, or partially right. Even a stopped clock is right twice a day.

Given all that, and that no one can forecast the market, here is my attempt to do so. Sure this has been a long Bull market. But this isn’t a euphoric market that charged out of the Great Recession. It has inched its way up slowly, climbing a wall of worry all the way. And it had, and could still have a long way to go. Does this feel like a frothy market top? Do you hear any euphoria? Have you heard anyone calling for a massive market rise, anyone at all? Does everyone seem worried about one thing or another? And the market keeps inching up. The economy is growing, unemployment is falling, employment is rising, there’s no inflation, NO inflation, and no wage inflation. The market usually continues to rise for two years after the Fed starts raising rates, and they’ve just made one token little step. Give me a break! Relax and have fun investing. Sure, a correction will come along sometime, but we’ll all live through it.

This is a wonderful compilation of all these guys who predict a stock market crash every year (often using the exact same words even, from year to year): https://pbs.twimg.com/media/CGVzK7_VIAAyCSH.jpg:large

{kind=link}

Right now (Mar 2016) we are in a growing economy, with rising employment, falling unemployment, low inflation, low interest rates, growing GDP, growing corporate earnings, and corporations are loaded with cash. This is a great environment for stocks, no matter what the bear market worriers say.

## On Insider Trading

In late May 2015, someone posted his concerns about insider selling of stock ABC, which influenced him to sell his shares.

I pointed out that, in April 2015, after a long and extensive debate, a MF service sold a third of their position in stock DEF! Why? You’ll never guess! Mostly because DEF insiders had sold a lot of their shares. Really a lot, according to the worriers. The CEO had sold 90% of his position since the IPO in 2013, and others had also sold 50% or more of their shares.

The price of DEF on the day the MF service sold, was $74.60. Most of the insiders sold for less. In fact, when I looked it up, they’d been selling a lot of shares since $46 in December, 2014! In mid June, (about nine weeks after the MF service sold), DEF hit $126!!! That was up over 170% from those insider sales in December, and up 39% from when the MF service got scared and sold. The insiders who sold in December at $46 would have almost tripled their money if they hadn’t sold. What does that tell you? Think about it for a second.

Eventually, many months later, problems did emerge and the price is now back in the low $40’s, but if you had sold when the bad news was clear you’d probably have gotten out at $100 to $105.

I don’t give any guarantees, but insiders sell for all kinds of reasons, and undoubtedly have plenty of stock options that haven’t vested yet. I wouldn’t make any decisions based primarily on insider sales, without some confirmatory evidence.

Heavy insider buying is something else again. It’s much rarer, and much more indicative.

## Thoughts on IPO’s and Secondaries

Little companies that are doing IPO’s or secondary distributions get ripped off by the underwriter (investment bank). It’s not that investment banks are evil. You might as well call a wolf evil because he eats rabbits. It’s the nature of things.

Here’s why: Sure the investment bank gets a fee for sponsoring the IPO and arranging to sell all the shares. But it still has to get rid of all those shares, which normally it sells to its own clients. Now if it’s a big popular company like FB that is having the IPO, everyone wants shares, and all the investment banks compete for the prestige of taking part in the IPO. That gives the company having the IPO a lot of negotiating power.

However, if it’s a little company that no one has ever heard of that is having the IPO, how is the investment bank going get rid of millions of shares? The answer is to pressure the little company to sell its shares as cheaply as possible. Well below what they are worth. What matters to the investment bank is how its own clients who get the shares will do, not how the company who is having the IPO will do. And it’s not only worried about its clients! The underwriter will take some of the shares itself, for its own book, if the price is low enough.

The IPO company is a one-time customer. However, the favorite clients will hopefully be there indefinitely and the investment bank wants to keep them happy so that they will take IPO stock in the future too. That insures that they, the investment bank, can keep getting those IPO fees, etc. In addition, if the favored customers can make instant money on the IPO, that gives them a good reason to keep their banking and investing relationships at the investment bank.

So that’s why you’ll hear of stocks going up 30%, 40% or more on the day of the IPO. The underwriter (think Goldman Sachs, Morgan Stanley, etc.), succeeded in getting a great deal for its clients by pricing the stock very low. Remember that the underwriter’s customers don’t know anything about the company. They just know they are getting a stock cheap and that they will be able to sell it at a profit almost immediately. Pretty good deal for them, isn’t it?

Sometimes the underwriter is able to sweeten it further and package a couple of shares with a warrant to buy at some price in the future. (That seems to be what happened with PN). That makes it an even better deal for the underwriter’s clients.

Usually, it’s a warrant to buy at an average price over a period of time, but for PN, they managed to slip in a clause saying the warrant holders could buy at the “lowest” price instead of the average price. Well PN found out how a little company can have its stock manipulated down for a short time. It got to $3.65! It only had to close that low for a day, you remember, (as I understood it, anyway).

Here’s another post I wrote a couple of years ago about a company having a secondary (slightly edited to make it more generic).

Here’s what’s going on: They are offering 6.0 million shares, 4.5 million by the company and 1.5 million by stockholders. (The shares from stockholders will be non-dilutive).

Why are they selling it so cheap? - They are a tiny company and they are getting ripped off by the underwriters of the sale. They have no pull so the underwriters can force them to sell cheap if they want to raise cash.

Why are the insiders selling some of their stock? - Because they own almost all of it, and want to diversify, or buy a house, or send their kids to college, or buy a Tesla.

Why do the underwriters force them to sell cheap? - First so they can buy a part of the shares cheap for themselves. Second so they can give their own favorite clients a bargain, and keep them happy.

Why is the price down today, the day before the secondary? - The underwriters’ clients, who are promised cheap shares, don’t know beans about the company and don’t care. Joe Blow, who is promised 20,000 shares tomorrow at $4.00, sees a price of $4.60, or $4.50, or whatever, and sells his promised 20,000 shares short at that price, knowing that he’ll cover his short tomorrow with the shares he gets at $4.00. So he makes a fast profit of 50 or 60 cents in one day. Probably nearly EVERY ONE of the underwriters’ clients is doing that, which is why the volume is so high. Pretty good deal for them!

## Investing Ethically

I have occasionally not felt comfortable in investing in a company that everyone else liked. For example, I was uncomfortable with ZLTQ because it’s a weight-loss company, with all those before and after ads you are familiar with.

Then there’s HZNP, a little pharmaceutical company whose meds are combinations of cheap non-steroidal anti-inflammatories like ibuprofen, combined with cheap over-the-counter stomach-protectors like ranitidine and omeprazole, all generics. Then they charge huge amounts for the combination medicine (which people could easily take as two cheap generic over-the-counter meds). Their investor stuff is all about how good their marketing is, and how they are convincing doctors to prescribe these overpriced meds, not about how effective they are. With a whole universe of great companies out there, is this really where I want to put my money?

I had the same problem with GILD, a company that the MF, and a lot of people on this board, love. Is it right to charge $80,000 for pills that cost maybe $1.00 to make, using the justification, basically, that they work? They should work. That’s the whole idea of a medicine. And they cure a chronic and potentially fatal disease. Does that mean that the company that makes an antibiotic that cures your pneumonia, which was going to kill you a lot quicker than hepatitis C, should therefore charge you $200,000 or $300,000 for the antibiotic? Or that the surgeon who removes your infected appendix (which was going to cause a very painful and miserable death) should charge $1,000,000, because he’s got you by the unmentionables? Is that the kind of world you want to live in? Is that the kind of company I want to invest in? Nope! It’s probably irrational, but those are just my feelings.

Graphing

Peter Lynch suggested a monthly graph of stock price vs trailing earnings on a log scale map, which I have found very helpful. I scale it so that if the stock is twenty times trailing earnings the price and the earnings graphs will overlap (he set his scale at fifteen times, but he invested in huge companies). That gives you a quick visual perspective of whether the stock is cheap, reasonably priced, or wildly priced, and also give a nice visual of how fast earnings are growing that you can compare with your other stocks, as you use the same scale for all of them.

Starting with a new stock, go back through at least two years of quarterly reports and pull off at least adjusted earnings and revenue. Make a table (pencil and paper) for each. Let’s look at earnings for company ABC.

2012: 02 04 08 08 = 22

2013: 08 10 22 19 = 59

2014: 19

You see what a good visual image this gives you. You can see both sequential change and year-over-year change at a glance, and that huge increase in earnings from 2012 to 2013.

Then do a running 12-month trailing earnings:

12 2012: 22

03 2013: 28

06 2013: 34

09 2013: 48

12 2013: 59

03 2014: 70

Gives you a picture of where they are going and how fast. To compare, here’s the earnings for XYZ. Regular good growth, but of course not as fast.

2012: 58 64 67 70 = 259

2013: 74 78 85 91 = 326

2014: 100

12 2012: 259

03 2013: 275

06 2013: 289

09 2013: 305

12 2013: 326

03 2014: 352

You should graph this on a piece of semi-log paper. On log paper a move from 10 cents to 20 cents is the same length as a move from 50 cents to a dollar (100%). I graph quarterly adjusted TTM earnings on the left side of the log paper and monthly stock price ranges on the right.

The basic sheet goes from 10 cents earnings on the bottom left to $1.00 on the top left, and from a $2 stock price on the bottom right to $20 stock price on the top right. If the price and earnings are at the same level it corresponds with a 20 times PE ratio. That’s true no matter where you are on the page. (35 cents is exactly across from $7, and 90 cents is across from $18, etc). It reflects a PE of 20 at every point on the vertical axis.

What happens when the earnings are over $1.00 or the price is over $20? BOFI was a good example (although the numbers are out of date now). At the time I wrote this it had TTM earnings of $3.52 and a price of $74. Well, instead of starting my graph at 10 cents trailing earnings and running it to $1.00, I started at $1.00 and ran it to $10. Stock prices then started at $20 and ran to $200. I had 11 quarters of trailing earnings points on my graph of BOFI (I start earlier than my buy point to give myself a picture when I first evaluate the company). It goes up at a very consistent 45-degree angle. TTM earnings of $3.52 is, of course, just above the $70 price line, and my monthly stock price line ran from $70 to $76 with a close at $73, so it was evident that it was fairly priced at a PE of just over 20.

At the time the trailing earnings referred to March, as June earnings weren’t out yet, but I had the stock price graphed for April, May, June and July. Thus the stock price can be as much as four months ahead of the TTM earnings. (When June earnings were published the PE dropped to under 20).

(If the graph starts lower and then goes up to a higher page, I cut off the white border of the graph paper and scotch tape the two pieces together so they run together seamlessly, and just fold them in half for storage.)

Zillow, by comparison, had its TTM earnings half way up the bottom page at 53 cents (opposite a 20 times earnings stock price of about $10.60), then a huge amount of empty space and the actual stock price up near the top of the second page at $143 or so. Gives you a picture of how ridiculously it was priced at the time. It’s now in the $80’s. (June 2015. It’s split since then)

I also find some blank place on the graph page for my tables of earnings, revenues and TTM earnings as described above.

To find the semi-log graph paper, go to http://www.printablepaper.net/preview/70_Divisions_5th_10th_… You’ll get a PDF that you can print out. That’s the one I use.

If you have the time, do a weekly graph as well on your stock, on old fashioned large graph paper. It helps you keep things in perspective. A drop from $51 to $49 doesn’t look so bad if you look back and see that it’s been between $52 and $48 for the past six weeks, or if you see that your stock rose from $40 to $51 in the previous two weeks and the “drop” to $49 is meaningless. (The problem with graphs that your computer makes is that a move from $10.00 to $10.05 will fill the whole space if that’s the whole move for the day or week. There’s no fixed scale.) Mark where you made purchases.

Graphing adds to my piece of mind. For example, when the price of EPAM hit $69.50 and finished the week at $66.50, I could look back and see that one week previously, the price had risen from $61.70 to $68.80, so this was just catching its breath and nothing to worry about.

It also gives me a quick visual look at where I’ve made recent purchases, as for every X dollars of purchase I put a little B, and a little S for the same amount of dollars of sales. So if I’m considering adding to a position I can quickly look at my graph and see that I just added 3X’s worth two weeks ago at a dollar less. That may or may not influence my decision. (I do prefer to buy stocks that are going up rather than down, but if a stock is going down for absolutely no reason, I may add cautiously as well.)

I can look at the graph and see immediately what the stock’s price action has been in the past several weeks or months.

## Professionally Managed Money

You can beat any mutual fund over the long run. Since they are investing many millions, if not billions of dollars, they can only invest in very large established companies, and hope to find a pricing anomaly.

I don’t know of any fund manager or hedge manager with a run like mine. It went through a number of recessions and lasted 19 years until I finally had a down year in 2008. But again, if a fund manager does real well for a year or two, not only does his fund get larger because of capital gains, his fund get flooded, swamped, with inflows of dollars and he can’t duplicate what he did when the fund was small.

Also they have lots of people looking over their shoulders for quarterly results (are they equaling their benchmark each quarter?). It makes it hard to get good results, I’m sure.

The average hedge fund gained 6.5% in 2013, when the S&P 500 gained 29.6%, and the best hedge fund manager was congratulated because he gained 25%. It shows how hard it is when you are investing billions of dollars, and how we can beat any mutual or hedge fund on a consistent basis. They are too big to invest in most of our type stocks. Also hedge funds invest in futures and currencies, which are zero sum games. When one wins, another loses and the sum comes to zero.

Money managers: A friend my own age (mid 70’s but in good health and still working part time) asked me for help. He had put all his assets to be managed for him by a broker or asset management company, and they had accomplished all of 3% for him in 2013, one of the best years for the market in recent memory. They invested 75% of his money in bonds (which paid almost nothing due to low interest rates, and then decreased in value in the latter part of the year when rates went up). The 25% they invested in dividend paying stocks made a net return of only 15%, giving him a total return of 3%.

My friend wants to take a quarter of the money and invest it himself. I said investing for himself was only going to work if he put time and energy into it, and if it was fun for him. If it’s an onerous chore, it’s better to let someone else do it. I suggested the Motley Fool to him, but since he was interested in income producing stocks I suggested Income Investor, and Stock Advisor once he got more comfortable. I also mentioned that MF has mutual funds and an asset management service if he decided he didn’t want to do it himself.

What I want to discuss was how asset managers could put anyone 75% in bonds? (Whatever his age was!) How can they ask to be paid for getting results that were one tenth of what the markets produced? I think that they must be covering themselves by investing super “conservatively.” No one can ever come back and sue them, no matter how bad their results, if they could say they invested “conservatively.”

And this was profoundly stupid! Interest rates were at epochal lows, so bond prices were at maximum high prices, and could only go lower when the Fed turned down the stimulation and interest rates started to rise. It had to happen. The handwriting was on the wall. But this didn’t stop them from putting my friend 70% in bonds, following some formula or something.

Lest you think that this was just because of my friend’s age, some months ago, a young guy in his thirties wrote in on the SA Investing Philosophy board to say that his asset managers put him 80%(!) in bonds… a guy in his 30’s!!! That’s malpractice it seems to me.

## Teaching Investing to Kids

You want to make it fun for the kids. I would consider first explaining what a stock is, and then presenting the stock market as the biggest and best game there is. Then I’d tell them what you look for in a company you invest in. I’d explain compounding growth by letting them multiply $100 by 1.2 or 1.3 ten times on a calculator, and then twenty times to see what that $100 would grow to in a company that could keep growing at 20% or 30%. I’d try to pick (and let them pick) companies that they are interested in, or could be interested in, even if they aren’t your first picks. You might consider making a competition between them for a year, say (with a small amount of real money), or for each of them to see how they do compared to the S&P, but warn them that growth stocks will go down more than the S&P in a down market. I’d say that one stock was too risky (you don’t want them to get in bad habits, even with limited funds). Probably 3-4 stocks each. I’d pay the commissions for them at first since they have small amounts of money and the commissions would take out too big of a chunk.

## Investment Primer:

We have members of this board with all different levels of investing experience, and from some recent questions, we have some members who are just starting out, and some with more experience. I prepared this primer for my wife, but you are all welcome to read it.

The Difference between Stocks and Bonds

Bonds: If you “buy” a bond, it means you actually lend money to the company. You receive interest payments for the term of the bond and then get your money back at the end of the loan.

For example, if you buy a thousand dollar, 5.6%, 20-year bond from GM, that means GM owes you a thousand dollars which they will pay back in twenty years from the issue date, and will pay 5.6% per year interest in the meanwhile ($56 per year).

Bonds trade on exchanges on Wall Street, just like stocks, so if you want to sell the bond and get your cash before the due date you can sell it just like a stock. The price will vary though and won’t always be exactly $1000.

For example if interest rates are very low (like now), and all you can get from the savings bank is 1% or less, that 5.6% can look very good to someone who is interested in income.

She might say to herself “I’d be willing to pay $1040, $1050, or even $1080 for that bond. It still has 18 years to run, and I’ll get $56 per year in interest. That’s $46 per year more than I’ll get from the bank. I know that I’ll only get $1000 back in 18 years when the bond matures, but even if I pay $1080 I’ll more than make the difference back within the first two years.”

On the other hand, if interest rates are high, at 7% or 8% for a fully guaranteed treasury bond, for example, the same person might say, “I’m not willing to pay $1000 for a GM bond paying 5.6% when I can get a better rate from the Treasury. I’m only willing to pay $920 for it. That way the $56 per year I get will actually be 6.1% on the money I’ve invested. It’s less than I’d get on a 7% bond, but when the bond matures, I’ll get a full $1000 back and make $80 profit.”

Also if there is any question that the company may fail, the value of their bonds will fall in value, because they may not be able to pay you back that $1000.

Note that if it’s closer to the maturity date, the price that people will pay will be closer to $1000, because they are about to get $1000 for the bond.

A new company starting out, or one whose finances are shaky, in order to interest people in lending them the money, will have to offer their bonds paying a higher rate of interest, than say a company like General Electric, for example. The question is “Is this company sure to be able to pay back the $1000 in 20 years?”

I personally never buy bonds. You have no chance of profiting in the success of the company, but all the risk if the company fails or goes out of business. In twenty years the company’s stock could be worth 50 times what it is now, but the bond is just a loan, and you’ll just get back what you loaned them - which will be worth only a small fraction of what you actually loaned them due to inflation.

My father called bonds “guaranteed confiscation,” because the money was guaranteed to lose value over time.

Stocks: about which we will talk at length, are ownership of a piece of the company. If the company has a million shares and you own one hundred shares, you own one ten thousandth of the company. If the company is successful and increases in value, your shares will go up proportionally.

If a company has 1 million shares of stock and each share happens to be trading today for $80, the company is valued by the market at $80 times 1 million, or $80 million. This is called the Market Cap, which is short for market capitalization.

Since the market sets the price of the stock, the price, and thus the Market Cap, can be more, or it can be less, than what you think it’s worth. It varies from day to day and can go up or down depending on how people estimate the company’s chances for success, or just for irrelevant reasons such as a big mutual fund deciding to buy the stock or sell it, or even because a large holder of the stock decides to buy an apartment in New York, and thus sells $1.5 million worth of shares.

Several factors go into how the public values a stock. One is growth, another is profit, a third is how much publicity a company gets, and a fourth is how much the company is in the public eye. Let me touch on these:

Growth is very important and people will almost always pay more for a company that is growing rapidly, even, usually, if it isn’t yet making money. (That is, they’ll value the fast growing company higher for a given amount of sales and earnings than they will another company with identical sales and earnings but which is not growing. They value the first company higher because they figure it will be worth more next year).

Profitability. I generally won’t buy a company until it’s profitable, but I do make occasional exceptions. A company can be quite profitable, but can be making the same nice amount of money each year, or be growing very slowly. In this case it won’t be valued as highly as a rapidly growing company. Its P/E ratio - how high its stock is priced relative to its earnings or profits - will be lots lower. (More on P/E ratios later)

Publicity is important because people have to hear about a stock before they can buy it. The stock is like a product that needs advertising. For example, if a newsletter recommends a stock, or if a brokerage house like Morgan Stanley recommends a stock, the price will go up because more people will be bidding for the same supply of stocks after the recommendation. There are even newsletters which make paid recommendations (recommendations for a fee)!

Public Eye. Everybody knows Google, for instance, and Amazon, so they will sell for higher multiples than a company like Ellie Mae, which automates the mortgage origination business. Everyone in the mortgage origination business may know Ellie Mae but that is a tiny fraction of the number of people who are familiar with Google or Amazon.

Size of the company. In general, smaller companies can grow faster and therefore often sell for higher valuations in relation to the size of their sales and earnings. In other words, they often sell at higher PE ratios. Part of the reason is “The Law of Large Numbers.” A little company, say with $20 million in sales, which is doubling each year but controls only a 1% share of its potential market, can double again next year, and the year after, and the year after that, and still have only an 8% share of its potential market. Maybe even less, if the potential market has grown in the meanwhile.

On the other hand, a big company with $20 billion in sales, which controls, say, a 40% share of its market, will have a very difficult time doubling its sales even once. (It’s hard to find $20 billion in new sales, and it’s almost impossible to go from a 40% share of the market to an 80% share).

Note that you can easily find a small company that has no room to grow. If it sells widgets and has $20 million in sales, but there are only $30 million in worldwide sales of widgets, where’s it going to go? Or if it has nothing special about its widgets, how is it going to get more sales, etc.

Similarly, a larger company with $5 billion in sales, may be facing a $200 billion worldwide opportunity, and thus have plenty of growing room. Rules about size are not hard and fast.

Quarterly Reports:

Each company in their quarterly report gives a rundown of its quarterly results, and usually compares them to the same quarter a year ago.

This starts off with their Revenues, or Sales (the money they brought in from selling things).

This is followed by the Cost of Sales, which is how much it cost to make and ship whatever they are selling. What is left is their Gross Profit and their Gross Margin (or Gross Profit Margin), which is what percent their Gross Profit made up of total revenue.

In other words, if they had $80 million in sales and their cost of sales was $30 million, their gross profit was $50 million, and their gross profit margin (or gross margin, for short) was 50/80 or 5/8 or 62.5%. It’s usually listed as a percent.

Then they list Operating Expenses, which are the cost of running the business, and are usually listed in categories like:

R&D - which stands for Research and Development and means pretty much what it says: the cost of research and of developing new products or improving the old ones.

SG&A - Which stands for Sales, General and Administrative, and includes everything from salesmen’s commissions to electric bills, legal and accounting expenses, and right through to the CEO’s salary.

Depreciation and Amortization - This is an accounting thing: If they bought or built a factory five years ago, they may be depreciating the cost over twenty years. That means they didn’t count (“write down”) all the expense in the year they built it (which would drop earnings that year enormously and not give a true picture of the business). Instead, they take 5% of the cost each year for 20 years for accounting purposes. This would be considered the “useful life” of the factory.

Other - This is miscellaneous. For example they sued someone for infringing on one of their patents and they received a payment. Or someone sued them, etc. Or they paid interest, or made interest on money the company had in the bank or had invested. It really is “other” and it’s usually minor.

Note that a lot of this is considered “fixed costs.” That is to say that doubling sales usually won’t require a doubling of salary expenses, or legal expenses, or accounting fees, or electricity in the home office. It won’t change depreciation or amortization, and probably the company will just increase research expenses marginally. That means that an increase in revenues can often increase profits by a larger percentage, once fixed costs are covered.

What’s left after you subtract operating expenses is Operating Profit, or Operating Income. The importance of this number is that one year the company could have a tax loss carryover and have lower taxes and higher profits, and another year pay full taxes and have lower profit. But, operating profit gives the amount that the company actually makes in running the business. It’s sometimes referred to as profit before taxes.

The percent that operating profit is of total revenue is Operating Margin. (In other words, operating profit divided by total revenue and expressed as a percentage. For example, if they had $80 million in revenues and $20 million in operating profit, their operating margin was 25%).

Another useful side-figure that is often referred to is EBITDA. (That stands for: Earnings Before Interest, Taxes, Depreciation and Amortization). It’s useful because it tells you how much money the actual business is making, and year-to-year comparisons can add to your understanding of the company’s business.

If you subtract taxes from Operating Income, you get Net Income, which is what’s left at the end. This is a very important figure. Net income divided by the number of shares gives you Earnings Per Share, or EPS.

The above covers the majority of the basic terms you need to understand. I’ll talk about two other terms, adjusted earnings and diluted EPS below, but they are just modifications of the basics.

For example: Basic EPS is Net Income divided by the total number of shares outstanding. However there may be additional potential shares that are not currently outstanding.

For instance, consider if employees have been granted options to buy an additional 100,000 shares, and the company sold someone else warrants to buy 50,000 shares more, you have to add that additional 150,000 shares to your outstanding share count to get the number of Fully Diluted Shares.

Then Diluted EPS is the net income divided by the fully diluted share count. Diluted EPS is usually a smaller number than basic EPS because the earning are divided among more potential shares.

The company will always list Basic EPS and Diluted EPS (as well as basic shares outstanding and fully diluted shares), but when people refer to Earnings per Share, they are almost always referring to Diluted EPS.

Adjusted earnings are another important term. The accountants preparing the quarterly reports have to follow what are called GAAP rules, which stands for “generally accepted accounting principles.” The problem is that some of the rules distort the true picture of how the company is doing, and others are just stupid.

Therefore, many, many companies give non-GAAP or “adjusted” results alongside the GAAP results. If the company had a large one-time expense or windfall, a legal expense or suit settlement, for example, they would remove these from the calculations to get adjusted results.

Also stock-based compensation, or option grants must be counted as an expense by GAAP rules, although there is no cash expense, and in spite of the fact that they are already counted by an increase in the diluted shares. Almost all companies remove this double counting expense in figuring adjusted earnings.

I ignore GAAP results almost entirely, and almost always use adjusted results, which usually make more sense and are more useful.

Now lets talk about the price to earnings ratio, or PE. (The terms “PE” and “PE ratio” are used interchangeably). The PE tells you how highly the market is valuing the company for the amount of earnings that they have. Simply, it tells you how many times the price of the stock (the price of one share of stock) is of the EPS (the earnings for that one share of stock).

You get the PE ratio by dividing the price of the stock that day, by the earnings per share over a full year. If you base it on the previous four quarters (which is a common method), it’s called the trailing PE. On the other hand, if you base it on what you think it will be this year, or the next four quarters, it’s called the forward PE.

For example, if the stock is selling today at $80 per share, and the company made $4.00 per share last year, their trailing PE is 80/4 = a PE of 20.

Note that I specified that it’s the price today, because the PE changes from day to day according to the price of the stock. If tomorrow or next week the price of the stock has gone up to $88, the PE will be 88/4 = 22. Thus higher PE’s mean the stock is more expensive.

Let’s go back to that stock with earnings of $4.00, a price of $80, and a trailing PE of 20. If you think that next year their earnings will be up 25% to $5.00, you can say that their forward PE is $80/5 = 16, which is quite reasonable for a stock growing at 25%.

A company’s PE can be quite different for the same earnings, depending on what the expectations are for the company and how fast it’s growing and what industry it’s in. For example a high-flying Internet stock making $4 per share, that people expect to be increasing its earnings by 50% per year for the next five years, could have a PE of 50 instead of 20, and be selling at $200 per share instead of $80 per share. And a stodgy company that makes electric lawn mowers and makes about the same $4 every year, with maybe 5% growth, might be selling at $40 per share, which gives it a PE of 10.

Companies with very high PE ratios (like 100 or more, because people have very high expectations for them) often don’t turn out well as investments, although the company itself may do well. That’s because it takes a long while for the company to grow into its stock price. These are often called “story stocks” because they have a great exciting story, which makes investors bid up the price of their shares.

Some companies keep growing like that though and end up making a lot of money for investors. The trick is to know which ones.

I would advise you that if you are going to invest in stocks you really, REALLY, should read EACH of the earnings reports of the companies you invest in.

The earnings reports are actually made up four things:

The Press Release (also called “the Earnings Report”). This is the press release the company puts out in which they give the outline of what they did in the quarter, their revenues, earnings, adjusted earnings, progress during the quarter and financial tables. The basics are important, but there is often stuff that I skim.

Then most companies have a Conference Call in which they give more color on what the quarter was like, and then answer questions from analysts. This is VERY useful. You can tell a lot from the tone and from the questions and answers. You can listen to this live, or go back and listen to it recorded. You can find it on Yahoo Finance or on the company’s investor relation website.

The problem with the recording is that, while you can hear the voices, which sometimes is wonderful, if it was an hour conference, it takes an hour to listen to. Thus Seeking Alpha does a transcript of each call. It only takes 10 to 15 minutes to READ. You can find the transcript on Yahoo Finance, or on Seeking Alpha (but not usually on the company’s investor relation website.

Finally there’s a government filing of the results, which if you’ve paid attention to the other three, you can probably skip unless you have serious questions. It’s available on the company’s website.

What do all those letters stand for?

To help you out, if you are a relative beginner, I thought I’d give some definitions. Let’s begin:

TTM or ttm (sometimes it’s in caps, sometimes in small letters). This means “trailing twelve months” and refers to the previous four quarters that have been reported. If the reference is to TTM earnings and the last quarter reported was Dec 2014, that’s easy. It refers to the sum of the March, June, Sept, and Dec 2014 earnings. But what if they have already reported Mar 2015 earnings? Then you use the sum of June, Sept, and Dec 2014, and Mar 2015, earnings, but you drop off Mar 2014 (which would be a fifth quarter).

GAAP is short for Generally Accepted Accounting Principles and refers to a set of fixed required accounting rules. These were created to avoid cheating on quarterly reports, but for all the good intentions, they unfortunately sometimes give bizarre and nonsensical results. For this reason, in addition to the GAAP results, which they are forced to give, most companies give:

Adjusted or non-GAAP results, which they feel (and I agree) give more consistent and more helpful results in allowing you to see how the company is doing from quarter to quarter. They are usually obtained by removing various non-cash expenses or gains, or extraordinary one-time gains or losses that don’t reflect how the underlying business is doing. (These can also be abused, but in my opinion are almost always preferable to GAAP).

YoY or yoy is short for Year-over-Year. Okay, but what does that mean? Well, for example, if you say March quarter results were up by 12% year-over-year, that means compared to March results a year ago. This is contrasted to sequentially.

Sequentially, which refers to the quarter just before. Thus, if you say March quarter results were up by 5% sequentially, that means compared to the December results, the quarter just before. Investors like to see earnings and revenues going up sequentially as well as you, but sometimes it isn’t possible because you also have to take seasonality into account.

Seasonality? What the heck is seasonality? Think Christmas. If you are a major retail store a large part of your years results will come during the December quarter. But if you are a manufacturer, your big quarter is likely to come in the quarter before, the September quarter, when you are shipping out to the stores who are stocking up for Christmas. And some businesses renew a lot of contracts in December and get a lot of business then, or get orders when other companies are closing their books for the year in December. Companies that do business in China are light in the first quarter because of the Chinese New Year. Those who do business in Europe may be light in the Sept quarter because every one is on vacation in August in Europe. Outdoor construction companies will do less business in the middle of winter, etc, etc.

The PE ratio or PE. This is the Price of the Stock divided by the earnings over the past year (These are the trailing-twelve-month earnings, or TTM earnings). It tells you how many times bigger the price is than the earnings. Lower is better. For example, company ABC has a price of $91.70 and adjusted earnings of $3.52, so it’s PE is 91.70 divided by 3.52, which gives a PE of 26. That means the price is 26 times the earnings, or that the earnings are just about 4% of the price. Generally a faster growing company will get a higher PE because the price is bid up by investors anticipating future higher earnings. Also, a company with a lot of hype will often get a higher PE, again because investors bid the price up based on dreams. (For example, last time I looked, company DEF had a PE of about 90 or so, which is huge, although it was growing at a quarter of the pace of ABC, but DEF had a lot of hype and TV ads, etc).

PEG ratio. This is an attempt to see if the PE is appropriate by comparing it to the rate of growth, (PE divided by the estimated rate of yearly growth of earnings over the next five years). It’s a noble effort, except that guessing the rate of growth of earnings over the next five years has no more accuracy than estimating how many angels can dance on the head of a pin. To avoid this problem, I suggested the 1YPEG.

1YPEG, or One Year PEG. This is the PEG looking back over the past year: the PE divided by the rate of growth of earnings over the most recent twelve months. It has the major disadvantage of looking backward, but has the advantage of using a real number, not a guess, for the growth rate. And the rate of growth over the next year will probably approximate the rate of growth over the past year, more than some five-year guess. The 1YPEG is just a screen though, to tell you if the price is in a reasonable range, and not the end-all and be-all.

TTM Rate of Growth of Earnings is calculated by taking the earnings of the last four reported quarters, and seeing how much they have risen over the four quarters previous. For example, you’d get it by taking the sum of June, Sept, and Dec 2014, and Mar 2015, earnings, and divide it by the sum of the sum of June, Sept, and Dec 2013, and Mar 2014, earnings.

## How To Post in Italics, Bold, and make Tables - This is copied for the most part from the Fool’s instruction page.

In simple terms; “i” is for italic. “b” is for bold. “tt” is for monospace font. All of those follow the usual Fool posting conventions. The only one that’s slightly different is for charting or tables: “PRE”. (see below)

You use them like this:

Italic

Bold

Monospace

``` Chart in monospace Year ChartValue Chart Value2 Chart Value3 1969 45 56 45 1970 61 55 42 1971 83 44 31 ```

You can avoid the “PRE” command by clicking the “Table Data” box directly under the “submit message” button, but that changes the entire post to Monospace and makes it a bit harder to read (especially if you have long lines of written text, which will cause the post to be really wide and force people to scroll back and forth to read it).

Most fonts use variable spacing (technically: Proportional spacing) so narrower letters don’t end up with a bunch of “white space” on each side. But variable pitch letters are a nightmare for column formatting, so you use “monospace.” Monospace means every letter is exactly the same width, whether it’s an “i” or a “w.” Note the difference between the “h” “i” and “j” in proportional spacing and monospace below:

abcdefghijklmnopqrstuvwxyz

abcdefghijklmnopqrstuvwxyz

POSTING IN ALL CAPS is considered mildly IMPOLITE, like shouting.

## Post Index

You’ll find more interesting and useful posts on the topics discussed in the Knowledgebase, on our board at the posts listed below. For the most part, extracts from these posts have gone into compiling this Knowledgebase.

About This Board: 2913, 5735

Saul’s Historical Results: 20, 4, 4952, 8618

General Approach and Philosophy: 5, 6, 7, 27, 40, 18, 1366, 3115, 3218, 1401, 1433, 435, 1315, 1368, 2151, 2350, 2387, 3943, 3946, 4025, 4037, 4830, 6092, 6131

Evaluating an Individual Company: 6, 1234, 5, 3115, 2003, 2011, 2165, 1416, 1451, 2537, 3619, 3924, 3930, 3943, 3946, 4568, 4830, 5305, 5794, 6951, 7143, 7427, 7435, 7768, 8225, 8263

GAAP vs. Non-GAAP or Adjusted: 197, 985, 6, 970, 4680, 5606

Prospecting for Companies: 120, 122

Investing Ethically: 6636

Portfolio Management: 6, 5, 50, 9012/9013, 64, 114, 18, 21, 22, 51, 52, 383, 78, 907, 964, 1392, 1438, 2110, 1129, 41, 435, 1416, 4, 3313, 4065, 4665, 5305, 5320, 5392, 5532, 6972

Benchmarks and Financial Indexes: 5

Thoughts on Multibaggers: 7, 63, 4

Calculating Portfolio Returns: 26

Buying: 5, 78, 8796 (New!), 1007, 1146, 1160, 1164, 21, 2350, 2387, 2898, 4665, 4830, 6156, 8392, 8402, 8418 7156

Price Anchoring: 40, 18, 5, 78, 8796, 71, 4517, 4807, 8822

Selling: 7, 50, 27, 64, 40, 21, 5, 18, 51, 52, 78, 8401 3218, 838, 907, 964, 1392, 1401, 1433, 1438, 71, 1417, 2151, 2489, 3867, 3858, 4065, 4807, 4517, 5305, 5320, 5392, 5532

Dips and Downturns: 1129, 1295, 1380, 2332, 1297, 2405, 1285, 3313, 3508, 3689, 3867, 3858, 3968, 6552, 9025

Dividends:

Insider Trading: 5056, 6556, 8980

Thoughts on IPO’s and Secondaries: 17229

Professionally Managed Money: 5, 8, 17, 79

Secondary Stock Offerings: 2207

Graphing: 2003, 5, 2893, 2112, 8373

Teaching Investing to Kids: 1075, 3119

Investment Primer: 84, 677

Board Basics: 2450, 2460, 2794, 8019