The Mungofitch bottom detector fired off. In an email from on of the regulars on the Mechanical Investing board he stated that bottom detector triggered.

At the very least close all short positions. This detector can signal multiple times before a solid rally begins.

Saul has noted that the Saul stocks are up off their lows significantly.

Having seen this game before, I would recommend a lot of time be spent getting a watch list together.

These calls are fascinating. They leave the longs and shorts at odd decision making points. Odd or difficult. Almost over informed.

What is happening in the interest rates swaps market in the UK was our Lehman Brothers moment in September. It would be interesting to see what the Mungofitch indicator said just before the actual Lehman Brothers moment.

The bottom detector is not quite the same as the buy detector in his indicator, correct? Excuse me while I start thinking about things to eventually buy…

I am absolutely no expert on this, not least because I don’t know the formal description for his current MI approach to identifying major bottoms (only the post from … 2011?).

My understanding is that the major bottom detector can keep triggering again and again and again and when it stops triggering, and turns positive, then in the short term it may be a good idea to buy. MAYBE. Because in a ‘deep and tricky part’ of the crash, you may get a couple of false positives before the true bottom.

If I had to guess, from the contagion-like behaviour and extreme moves in the UK government bond and currency markets last Tuesday, and the very high overnight repo rate, we may be in a ‘deep part’ of the crash.

I’m just making this up here, but on the occasions when it works well, the pattern goes something like this:

Day 0-30: negative new high new lows

Day 31: lots of shares dumped -3%

Day 32: lots of shares dumped -2%

Day 33: positive new high new low ← this turns out to be a false positive but not terrible time to buy

Day 34: lots of shares dumped -5%

Day 35: some shares dumped -1%

Day 36: positive new highs new lows <—

Day 37: … short term bounce … ?

It depends whether you want to trade the bear market, or if you want to buy at a particular price point. For example it’s possible to absolute nail several local bottoms with a successful ‘bottom detector’ but then find yourself having lost money when subsequent market bottoms are visited.

25% is not an especially deep market bottom when you consider the sheer range of awfulness we face

market contagion events

housing bubble crashing

general bond bubble crashing including high quality bonds

junk bond bubble

crash starting with stocks at the 1st/2nd most high valuation in history

stocks still far above historical norms of valuation (e.g. CAPE, buffett ratio),

inflation still persistent and also rising (europe now 10%, UK >12% RPI)

rates still rising and central banks committing grimly to more rate rises and faster than expected and further than expected

historically bear markets do not fully bottom till rates stop rising

low probability of a major fed pivot (though in fairness, we have just seen a reluctant temporary pivot from the BOE, likely from heavy political pressure)

downturns in particular sectors that are highly represented in the sp500 like tech, advertising, consumer discretionary

From Jim’s new site:

“The other model is a “major bottom” detector. It’s signals are quite rare, but often quite useful. Occasionally it is too early, giving buy signals several times on the way down during a really bad market tumble. This was really only a problem in 1974 and 2008. But other than those stretches, usually the signals are pretty good.”

The general public, we, never got any accounting from the powers that be of what happened in 08 to the interest rate swap market. In a sense it was written out of the history in terms of buying bonds by the central bankers.

The other catch is that it often signals several days in a row, so the safest interpretation is to wait for the first market day that it does NOT signal. This signal triggered on Sept 29, but not Sept 30, so (to the extent that it has any value) the US market is a buy now. The market might tumble some more, but it’s usually quite a bit higher a year after such a signal. If you were to buy after the first “no signal” day after a signal day, on average the S&P 500 is 12% higher 6 months later, 21% higher a year later, and 36% higher two years later. Not adjusted for dividends or inflation.

It’s far from perfect, but if I had some short term short market positions, I’d close them

So it is a buy within the limitations of the method. Note: It has detected false bottoms two times in the past, in 1974 and 2008.

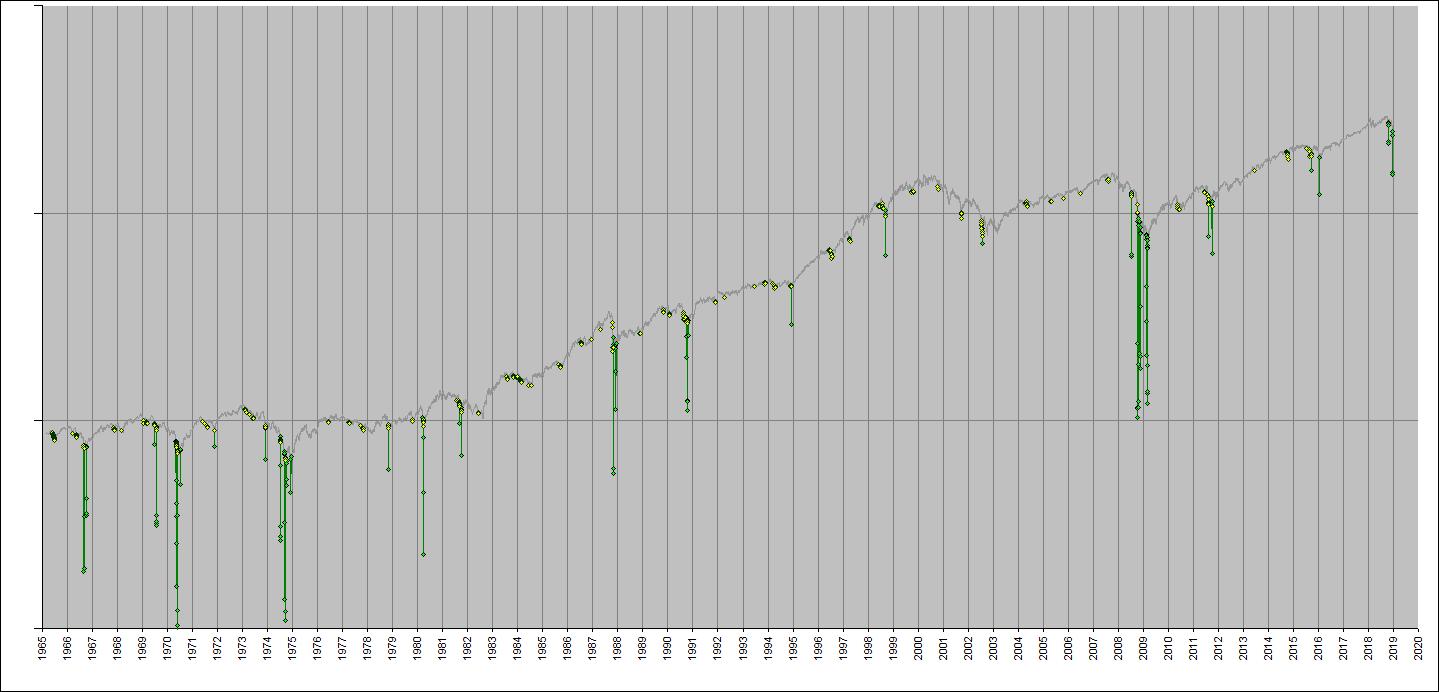

From a Mungo post within the thread, he provides an older graph showing when his minor and major bottom indicators fired:

Question: any prediction as to how many times the bottom might be tested after the major bottom signal has been triggered?

Pretty good chance, if this ends up being a great big bad bear.

It’s hard to categorize the signal’s behaviour for that, but you can look at this graph. http://stonewellfunds.com/CapitulationBottoms_2018-12.png

The vertical lines are the major bottom detector signal dates.

The longer lines mean dates of stronger signals.

You can see lots of “too early” signals in late 2008, but it’s mostly not bad.

The market often drops more, but the one year forward returns are pretty reliably good.

Interesting to read through that thread. Everyone, including Mungo, was somewhat skeptical about the bottom detector being reliable at that time, thinking there might be another leg down. Some people were totally disbelieving. I guess it’s pretty good at identifying times of high pessimism.

Not sure. Jim’s never really said how it works, so I’d just be speculating.

Personally, I don’t think it is necessary to plumb the exact bottom. Good enough is good enough. However, one stock (besides BRK) that Jim has been recommending lately is GOOG. The P/S is 18, with an average of 20 over the last five years. The P/E is also 18, with an average of 32. So it is cheaper than average right now.

All of what I write below is purely my personal opinion, and is not presented as factual! If anyone sees something which is clearly unfair or untrue, I would be grateful if you could highlight it.

I think Google clearly have internet advertising captured. The problem is, revenue growth is going to suck, because they’re the 99.6% gorilla. Hence ‘2 ads before each video’ etc on Youtube. Hence people being annoyed their web and mobile ads are getting shown randomly to totally unrelated audiences they didn’t want to pay for, to drive up ad impression payments.

Frankly, I feel Google are just not good at many things except ads - when it comes to making money from them.

Android phones aren’t as popular as iPhone despite being 1/10 the price and largely similar features.

e.g. Google Stadia suddenly being shut down even as developers complete games built for it. And 100 other shut down projects just like that.

Dysfunctional internal promotion system that promotes ‘making a shiny thing and abandoning it’

They literally had the ability to revolutionise the world of art and design with DALL-E, but greeded on the payment model (pay per image attempt, not ‘till you get success’), and restricted access to invite only. In those months they could have dominated the creative industries, they sat on their hands and made cool youtube videos & powerpoints. Meanwhile, ‘stable diffusion’ came out, totally free and open source, and has overwhelmed and completely obsoleted all their years of work on DALL-E in a matter of weeks. It would be like if Moderna had spent 12 months doing a success tour around the world before actually selling any jabs, then got home to discover Novavax had vaccinated the world.

I don’t see there being much growth in showing 2,3,4,5,10,20 adverts before each youtube video, and frankly Tiktok is beating them with a better algorithm (less ‘promoted’ material) and fewer ads.

I feel Google basically have an amazing track record of failure, inability to monetise, or just giving up randomly overnight in so many industries they’ve tried to break into. I can hardly think of a company with less natural ability to expand its moat. I can hardly think of a company I would be less willing to trust for basing a new business model upon e.g. for their APIs, cloud services etc… Well, OK, there’s a certain database company. But still.

(I say that as someone who occasionally gets recruitment attempts from G. I always say no.)

For me it’s very hard to justify buying Google when I can just buy more Berkshire.

While I appreciate the sentiment of the overall post this piece of it is beyond ‘just’ wrong - it’s incorrect on a number of levels including:

Android is the largest OS in the world period - and the vast majority of the devices are phones. By greater than a factor 3-4x. It’s tough to get a good total number on either Android or iOS (and its derivatives iPadOS etc.) but by just adding the Google hints to Chinese Android estimates gets to well over 4 Bn devices compared to iOS derivatives at circa 1 Bn (perhaps a little more). As an aside iOS et al are also behind Windows at an estimated 1.5 Bn devices.

There maybe some Android phones that retail as low as 1/10 the price of Android in markets like Africa & India etc. but in the West where Android matches or beats the iPhone for market share (it has similar but lower share to iOS in the US and quite a bit higher share in the EU for example), pricing can generally comparable to iPhones. Android has its flagship phones that can even retail at higher prices (Samsung’s Fold & Flip lines for example), for the same price (Samsung’s Galaxy S lines as an example) and then models that compete with the iPhone SE (Samsung’s Galaxy A series as another example). You’d really struggle in the West to find a model for sale at 1/10 the price of the iPhone SE.

Today on Walmart.com –

Cricket Iphone SE 2nd gen (2020) $199, (current gen SE is $429 on apple.com)

Cricket Vision 3 (Android 11) $29

Not quite 10% but pretty darn close considering I looked for less than 5 min

I do agree that Android is not necessarily cheaper – you can certainly pay as much or more for one – but I do think part of Android’s popularity for the masses (in spite of seeing several sites that claim that IOS has overtaken/passed Android in the US ) is the availability of very cheap phones.

That is about what I was wondering. Would such a mechanical device signal “a” bottom, or “the” bottom? I keep thinking of the nonsense I see passed off as “news”, with shrieking headlines like “Motley Fool issues rare all in buy alert”.

How can a mechanical rule measure the myriad things that panic the market one way, then the other? We don’t often have a full on European war, with one party threatening to go nuclear, so how can it be factored in to a mechanical rule?

The mob can always find something else to panic about, even if the “crisis” is entirely fabricated.

Apologies, you are quite correct. The fault is mine, I should have explained what I mean by the word ‘popular’. I mean ‘fashionable, desirable’, not ‘purchased’. One might argue that fashionable desirable things are ‘whatever actually gets purchased’. But that leads us to the conclusion that bread and milk are profoundly fashionable. I suppose that also means I’m talking about the developed world (where profit lies) and not those countries where people are paying $80 for a phone.

I wonder what it would be if the price of iphones didn’t have such large profit margins embedded. But that is not the case.

Anyway I’ll happily concede you are correct that android is more ‘popular’ than iphone in the sense more people choose to use them.

You’d really struggle in the West to find a model for sale at 1/10 the price of the iPhone SE.

Yes, I suppose it is hyperbolic. In my head I was comparing ‘an iphone I’d be OK to buy (probably the 14)’ against ‘an android phone I’d be OK to buy (probably the Moto G31)’. Not a fair fight.

Historically average iphones have cost a multiple of the price of average android phones (2.5-3x), I can’t find current data right now:

There’s also the question of whether ‘what you pay’ is merely the up-front cost of a phone or the total by the time you resell it and upgrade.

That is significantly different between android and iphone. If this point seems unreasonable, consider, would it be unreasonable when comparing cars?

Question to the crowd: Can anyone name any large company in history with more of a track record of buying & building ‘toys’ that are not monetisable, or not monetised, ultra-low margin, or simply straight out abandoned, than google.

I’m not qualified to answer that direct question, as I don’t have any facts about abandoned projects across large companies.

However, I think I can add a little fuel to the fire wrt google and abandoned projects. I worked for a global electric / gas utility from 2008 - 2010 in their IT function as a Director of Data Architecture. This role put me in an area of responsibility to be deeply involved with many of the initiatives throughout the organization. One of those initiatives was “smart metering”.

Smart metering was the term used to measure and manage distributed energy production in the home as well as managing power hungry devices / appliances within the home.

We were contacted by google to “partner” with them to use their resources (data storage, analytics, AI and research people) so that they could use the information in a way that could be useful to them. Obviously we all know that the more google (and other FAANG) companies know about you and your lifestyle, the better they can target ads and other offers to you.

Google spent a lot of time with us trying to sell us the idea of a partnership that offered us these “free” services in return for access to the data, but no way would the execs in the corner office allow that to happen.

I attended a national utility conference a year or so after we terminated our relationship with google and learned that they had abandoned that idea. However, they then bought out Nest in 2014, which got them another step closer to energy monitoring (as well as other home management services).

So, while they may have abandoned the “we’ll offer free services to utilities in exchange for their data” initiative may not have taken off, it may have lead to them considering an alternative strategy of just flat out buying a company that was on the ground floor of the energy management service.

{kind=link}