I have yet to read it, but here is a link. From the title, guessing he likes Pure.

Pure Storage: A Company That’s Here To Stay https://seekingalpha.com/article/4162116?source=ansh $PSTG

I have yet to read it, but here is a link. From the title, guessing he likes Pure.

Pure Storage: A Company That’s Here To Stay https://seekingalpha.com/article/4162116?source=ansh $PSTG

It’s a nice deep dive, and yes he still likes and owns shares.

Summary:

Pure recently sold a substantial issue of convertible debt.

The interest rate was 0.125% with a premium of of more than 32% at the time the debt was sold.

Pure’s valuation continues to languish at levels suggesting a murky future for this high-growth company.

All indications continue to suggest that guidance will prove conservative and growth will remain at elevated levels.

This is one high-growth company that’s showing noticeable increases in profitability due both to growth and strong expense discipline

Matt

Some key take-aways from Bert (emphasis added by me):

The current revenue for forecast for Pure is for 38% revenue growth this current quarter, moderating noticeably to 31% for the entire fiscal year and to 26% for fiscal year 2020 (ends 1/31). At some level, current estimates do not mean a great deal. Estimates have been steadily rising for both revenues and for earnings. The company has been public for almost exactly a year and it has beaten its forecast in all of the quarters it has so far reported.

If revenue growth exceeds the current guidance of just greater than 30%, the opportunity for substantial margin expansion is substantial.

My guess, which is all that it can be, is that free cash flow margins next year will be in the 7%-8% range and that free cash flow dollars will reach about $110 million.

Based on a slightly more positive growth estimate for this company for this year, my belief is that the EV/S ratio is currently at 2.4X. I think a 2.4X ratio, even for a hardware company, is quite modest given the strong improvements the company is achieving in profitability and cash flow.

I expect it to produce strong positive alpha in the next year.

I think Pure is still my favorite bet to double in 2018 even though they’re only up 18% so far. (Ok maybe Wix would edge them out since it’s already up 46%.)

My favorite part of the article is where Bert laments the shortsightedness of analysts, Goldman’s in particular:

The GS analyst simply refuses the evidence that Dell remains as it has been since its consolidation, a market share donor. He continues to feel that rhetoric, particularly about pricing and sales execution, is a substitute for product benefits. Dell may have hired storage sale specialists and it continues to talk about its “refuse to lose” initiatives, but lose it does.

Dell? Really? That’s not even a good Cisco/Arista comp. Dell hasn’t been really relevant since the “Dude, you’re getting a Dell” guy. https://youtu.be/8BsWijdM0W0

Very glad to see Bert affirm that he’s still excited about Pure, too. He’s been writing about them on Seeking Alpha for close to two years now, and he certainly realizes that though they’re up some 80% in the last 12 months, they are still a company with a lot of room to run.

Bear

Dell? Really? That’s not even a good Cisco/Arista comp. Dell hasn’t been really relevant since the “Dude, you’re getting a Dell” guy.

Maybe you’ve forgotten that Dell bought the 800lb gorilla in storage, EMC, a few years ago?

I’m growing more positive on PTSG, but I don’t yet have anywhere near the conviction that I have in ANET, for instance. Seems like Pure has more nimble competition than Arista does, for one, and Arista has made a bigger dent in Cisco than Pure in EMC or NetApp, etc.

But, Bert’s article is a good read. And I’m glad he at least acknowledges the margin expectation differences with software vendors.

“The GS analyst simply refuses the evidence that Dell remains as it has been since its consolidation, a market share donor.”

“Dell? Really?”

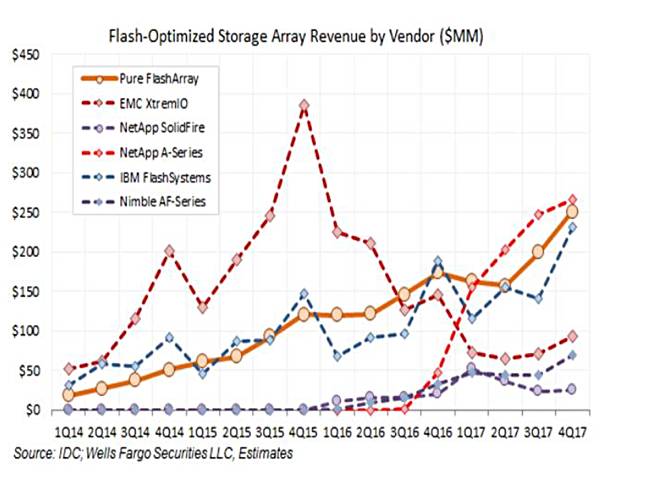

Yeah Dell’s share of the Flash pie has just fallen off a cliff. This was batted around a while back from a register article. It has a chart that shows Flash Revenue by vendor.

https://regmedia.co.uk/2018/03/02/rakers_afa_supplier_shares…

That’s the chart. Here’s the full article.

https://www.theregister.co.uk/2018/03/02/pure_billion_dollar…

Seems to be a lot to like with Pure.

Maybe you’ve forgotten that Dell bought the 800lb gorilla in storage, EMC, a few years ago?

More importantly, that purchase of EMC made Dell the majority owner of VMware.

Their products are heavily integrated.

vSAN is in at the kernel level of the VxRail HCI solution that competes against Nutanix HCI.

Nutanix wants to grow broaden their markets and be software only. VMware already software-only.

Nutanix wants to be the O/S for the multi-cloud. DellEMC+VMware has Cloud Foundations running on VxRail which is basically what Nutanix is trying to accomplish. (with the difference being that Nutanix doesn’t care about the hardware, while DellEMC is still in the hardware biz so they care about that piece too).

Both VMware and Nutanix will compete against Microsoft’s AzureStack for years to come to lay claim as the share leader of the expected-to-be-significant multi-billion TAM of “Enterprise / Multi-Cloud Management”.

All of these solutions are creating an SDDC (Software-defined Data Center) which reduces risk in the Enterprise by eliminating many opptys for human error from traditional IT mgmt.

Of all those stocks, I like NTNX best for potential. No idea if they can execute, but they have momentum and a good plan and the most upside compared to MSFT massive mkt cap and VMware is already very large too.

-Dreamer

{kind=link}