Hi 12x

These portions of your post all kind of go hand in hand.

And in this transition from hardware to software only to subscription, it is not clear to me if they are actually growing if their subscription growth is just being offset by declining non subscription software sales…

…The only metric that suggests to me that they are still growing is their non stop increase in customer count. That hasn’t let up…

…If I could see what their comparable revenues would have been to get a gauge if they are still growing it may give me a different perspective on this company. But when I look at lethargic overall software sales growth I don’t get too excited.

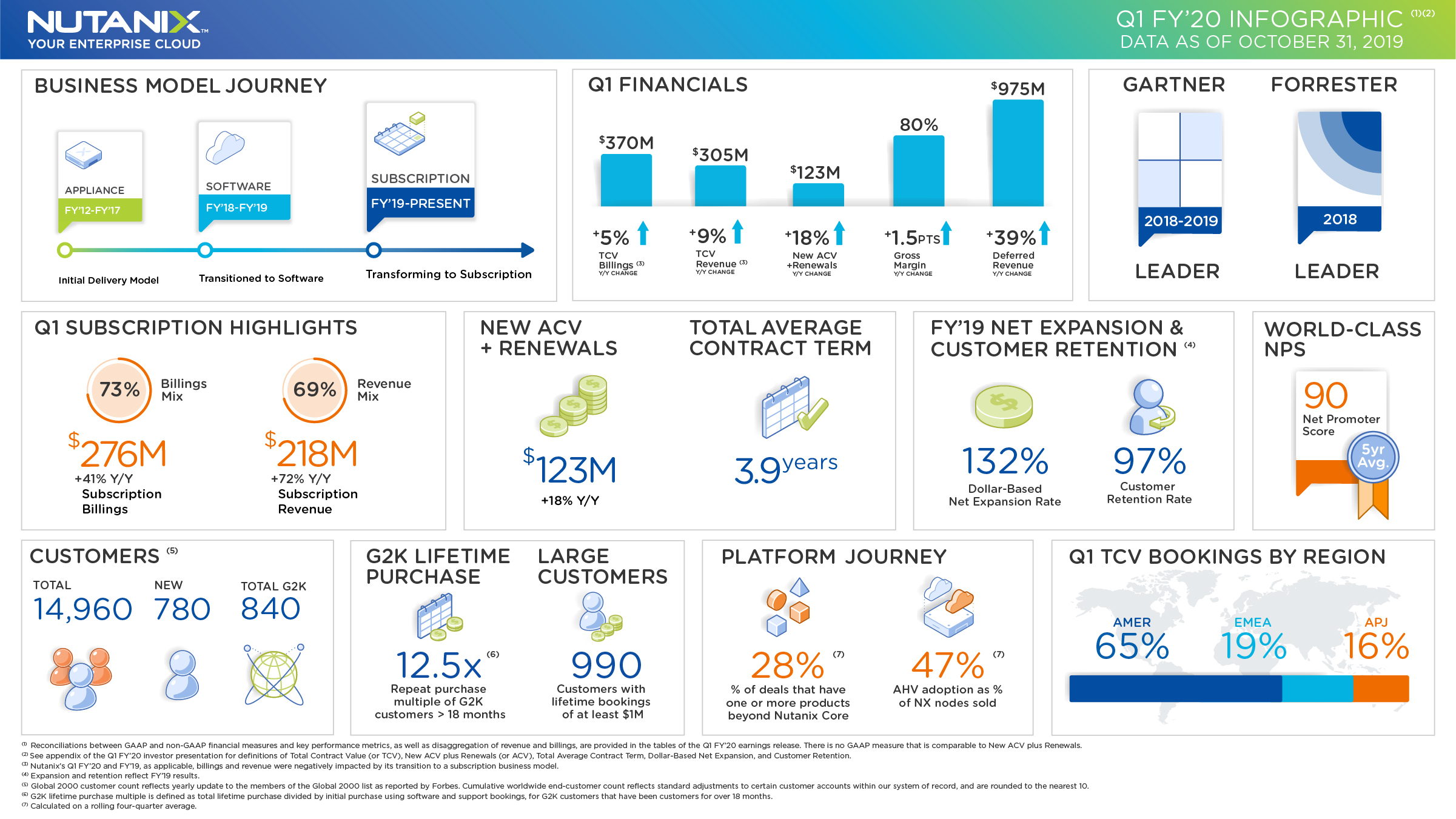

I think you are essentially asking - how do we know how they are doing apples to apples since so much has changed recently?

First off let me address your first thought regarding whether new subscription revenue is just replacing non-subscription software sales. While yes, there are certainly going to be customers switching from buying a software license to now be on a subscription, but keep in mind if customers move from one to another without any real growth from new customers, your revenue would not stay flat overall, it would go much lower. That is because non-subscription software licenses were recognized by Nutanix “upon transfer of control to the customer” (e.g. Up Front), as per their Form 10-K. With the subscription model, the revenue for their SaaS software offereings get recognized “ratably”, over the life of the subscription. Hence the much higher Deferred revenue today, much of which would have already been recognized as revenue under the old non-subscription software license sales model of yesteryear.

The company recommends using “annual contract value” (ACV) to get the best apples to apples comparison. Here’s some commentary from yesterday’s earnings call:

…we believe the single best metric to measure the true growth profile of the company during our transition to our new subscription based model is new annual contract value plus renewals, or ACV for short, booked in the quarter, which includes sales of life of device licenses based on an assumed five-year term. By calculating in this way, we take into account the changing term lengths, while still showing the impact of our continued sales of life of device licenses.

Having aggregate ACV in any given period will allow us for a cleaner apples-to-apples comparison of period-over-period growth rates. In its most simplistic form, we define ACV booked in the quarter as the annual contract value of new business plus the annual contract value of renewals. And we calculate ACV booked in the quarter by taking the value of each transaction booked in the quarter including renewals, but excluding professional services divided by its term length and then summing the total of those values.

and for the quarter just ended October 31st:

ACV booked in the quarter was $123 million and up 18% from the year ago quarter. New customer bookings represented 24% of total bookings in the quarter, the same as Q1 '19 and up from 23% in Q4 '19.

So they are telling us that they closed deals this past quarter that, on average will generate $123 m per year (which assumes that any non-subscription software sale would have a theoretical 5 year life). And they are saying that is +18% vs the same quarter of last year so they want us to consider this 18% growth.

For the full year fiscal 2020 (year ending July 2020) they forecast ACV to grow +25% for the full year, and that is despite not increasing their full year forecast yet, even after the Q1 beat. This would mean an acceleration from 18% last quarter, and would imply that they will be well above 25% for the second half of the fiscal year, given that they are forecasting an average of 25% for the full year despite that year being weighed down by only 18% in Q1.

So that tells me that if they achieve their forecast for the rest of the year, their growth will accelerate from a fairly negligible amount last year, to 18% last quarter, to 30%+ by the end of the fiscal year next summer. Obviously a big “if” for them to achieve their forecast given their stumble in early '19, but they did beat expectations in Q1, so it might be realistic.

One other comment they made is that, typically, due to Q1 being a seasonally weak bookings quarter, their backlog historically declines by 25% from the end of Q4 to the end of Q1, and management says that, in each of the past three years, this has consistently been the case (-25% backlog drop during those three months of Q1). However, this year, there was no dropoff in backlog from the end of Q4 (July 31st) to the end of Q1 (Oct 31st). Total backlog stayed essentially flat. That sure looks like a positive indication that the year will continue strong. I believe that Q2 and Q3 are the seasonally strongest quarters of the year, so having that higher than usual backlog already lined up to juice the upcoming quarters sure sounds like a good sign to me. Not to mention all of that (growing) deferred revenue that still hasn’t been recognized yet.

Overall, I certainly get why a lot of people don’t want to touch Nutanix stock. Management got it really wrong earlier this year, it caused a lot of pain for shareholders including myself, and I don’t blame anyone for going with whatever feel like the best deployment of your investable dollars, and avoiding NTNX if you have more confidence in other companies.

But yes, I think that, despite the challenges in comparing their results from each of the past few years, there is reason to believe that they are really growing recently, and setting themselves up for accelerating further growth going forward. As I mentioned above, I am not adding to my large position at these prices right now, but I am not planning to sell off anything in the near future either.

This could still go very well or very wrong for NTNX owners, but I am excited to see how it plays out!

-mekong

{kind=link}