Tech name valuations are getting richer. In this thread, I will be looking at some of the names and some comments about where their current stock price vs valuation stands.

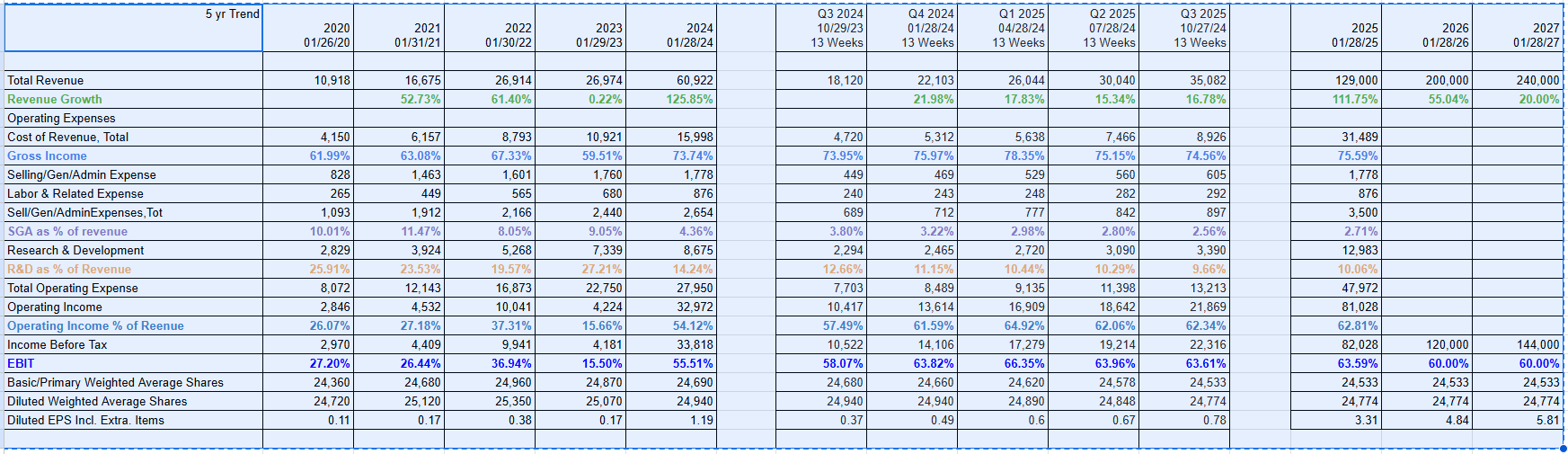

Nvidia’s revenue growth has been astonishing, with a 125% increase in 2023 and an expected 112% increase in 2024. By 2026, revenue is projected to be nearly nine times higher than in 2022. Let it sink. How much more runway they have in terms of revenue growth? Their EBIT (that is earnings before interest, and tax) is whooping 60%+, for comparison MSFT has only 40% margin.

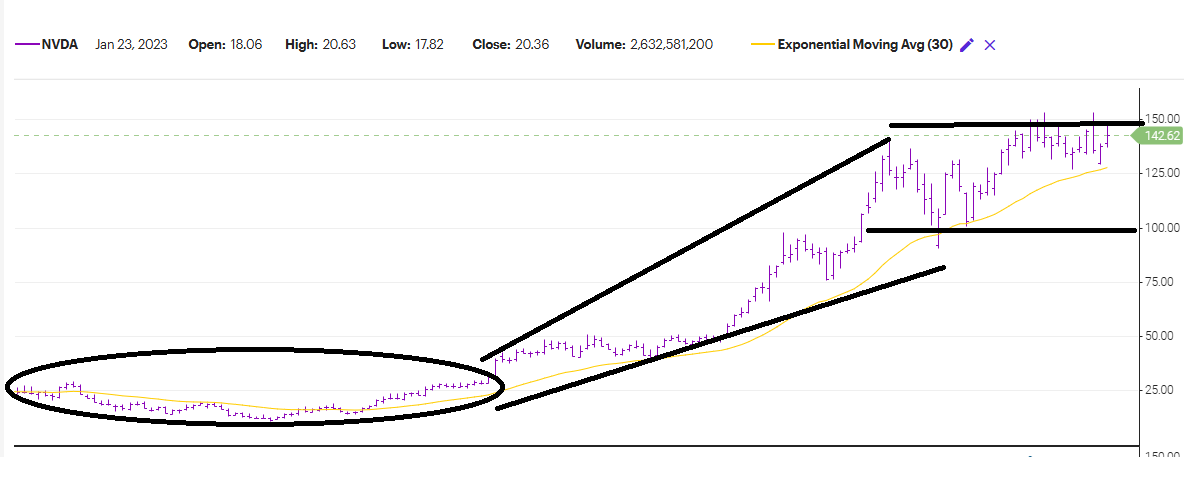

NVDA is the leader of this AI cycle, they are leading this innovation cycle, and their customers are willing to spend $100’s of billion to buy their chips, network gear, and accompanying software. At least, growth is going to be at a very high level in the next 4 quarters. There are many who argue, the valuation is not expensive for such a quality, growth name. NVDA current market cap is $3.3 T and there are analysts calling for $10 T valuation. The entire AI market is expected to be $15 Trillion in the next 10 years.

I know trillion is not a big number any more.

These are really very big numbers. However, it’s important to note that several factors could impact this growth trajectory. Increasing competition from other technology companies, potential regulatory hurdles, and economic downturns could all pose challenges.

OTOH, many countries are slowly waking up to the potential of AI and feel they need to have “their own AI”. There are folks in US arguing against open source AI citing national security reasons. Already Biden administration started some protectionist measures, and Trump ran his campaign and the folks who are appointed all have a big anti-China bias. The other countries in the world can infer only one lesson from this. If you want to be independent, maintain your sovereignty, you need to reduce your dependence on US companies, technology. Will that result in a sustained tail wind for NVDA? Only time will tell. BTW, why is this important? Currently all the major cloud providers (US based ) are pouring 10’s of billions in buying NVDA chips. How long will they be able to do it? How much more runway they have to increase these investments? So you need additional deep pocket customers. That’s where the state players come in.

Separately, we are seeing reports about LLM’s hitting scaling fall. Unless there is a breakthrough with AI architecture, the incremental benefit vs the investment is going to be very stretched. For those new to this, the paper “attention is all you need”, a landmark machine learning research paper in 2017, which introduced the “transformer” architecture is behind the current LLM foundation models.

This paper is from Google research scientists. Tech companies for all their fault, are not just getting very big, but they are contributing significant technologies thus a significant contribution to the society.

The million, billion, trillion $$$ question is where is the plateau and whether current valuation already discounts it? I think we will not have an answer until late 2025 or early 2026. The initial clues are slowing q-o-q growth.

For now, I have sold some $250 Naked calls. Please don’t try this. Selling naked calls are very risky, exposing you to unlimited losses. You need to be very nimble and willing to have a very high risk aptitude. Either you are a sophisticated rich hedge fund or crazy person like me will try that. Don’t do it.