-This is pretty exciting. A big part of the On thesis is that they eventually will be able to generate significant revenue from Apparel. This is their first tennis specific apparel.

"On made waves in the tennis world almost exactly a year ago, when it announced world No. 1 Swiatek and rising American star Shelton had signed head-to-toe deals with the brand—joining a team that boasts 20-time Grand Slam champion Roger Federer as an investor.

But while fans of both players haven’t been able to buy the outfits worn by Swiatek, Shelton or fellow ambassador Joao Fonseca, the players themselves have regularly talked about [giving the brand their feedback] during [various points in the partnership].

The result will be a comprehensive racquet-sports focused collection that goes from on-court to off-court with ease, comprising 17 pieces across apparel and footwear. From Shelton’s pink-accented tank top to Swiatek’s signature two-piece match outfits, this collection will emphasize “sleek, modern designs that make a statement” and are designed to be snug yet flexible for ease of movement around the court."

-On Also just dropped the new Roger Federer shoe: “designed for today’s “casual but competitive tennis player.” Think of it as the perfect middle ground between its pinnacle performance shoe THE ROGER Pro—worn by players like Shelton in professional competition—and the heritage off-court style from other “Roger” models.”

Full Article:

First look: On to launch tennis apparel line in collaboration with Iga Swiatek and Ben Shelton

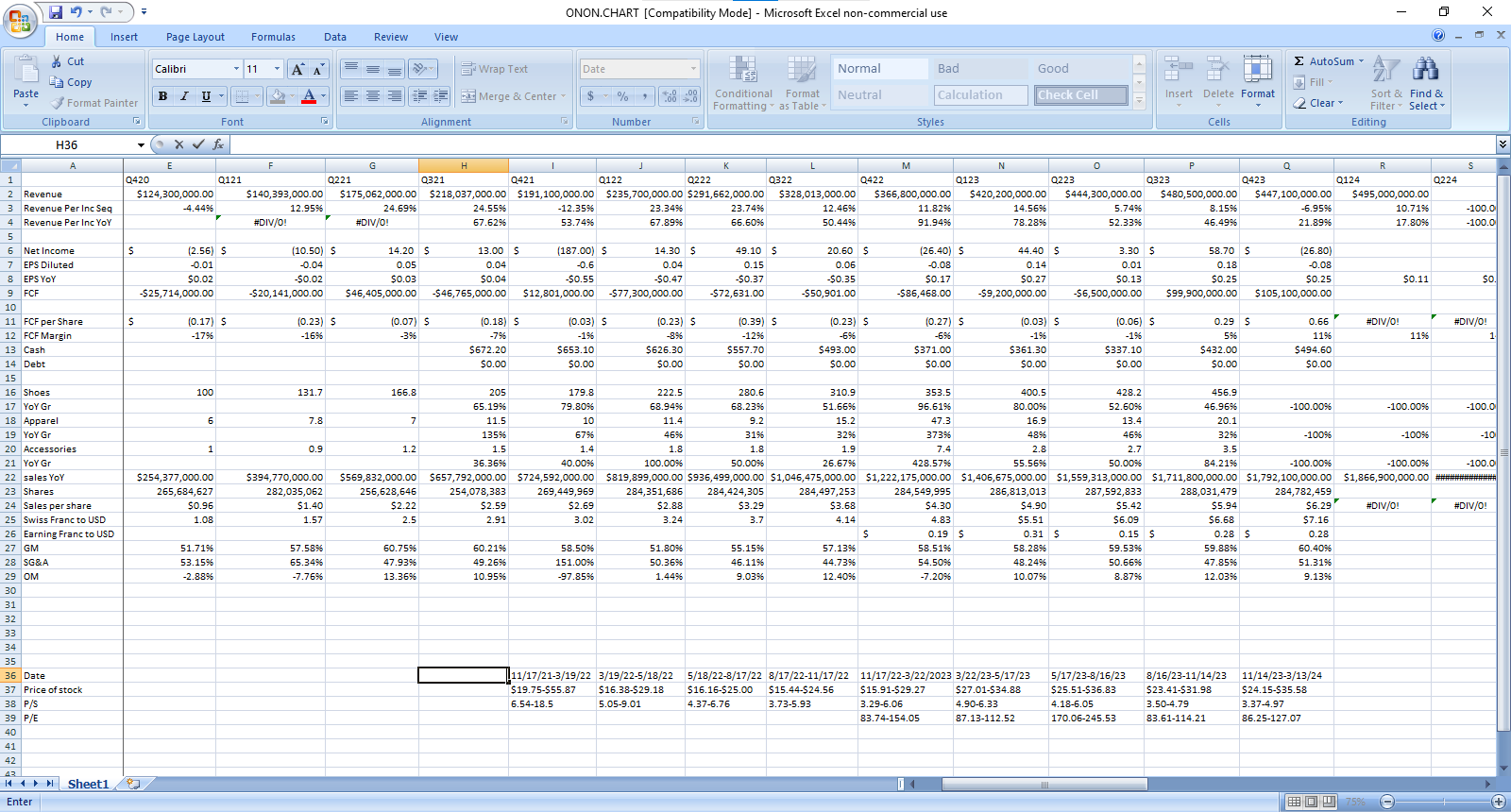

Long ONON, 3.8% position