I wrote and then forgot to publish my May summary, so I’m combining May and June, which have been great months for my Portfolio. Some of the company notes might be a little clunky due to the combination. Looking at my year, despite all the chaos I really just had a terrible March and it’s been a long road to recover to what is now a decent gain for the year.

May was a hell of a month with many of my companies up 20% or more. I was up almost 25% which got me back to green for the year. Much of this seemed to be due to the easing of the macro/tariff situation, but I had some very promising earnings reports as well.

June was more of a mixed bag but I had some more huge gains with half of my positions to lead to another really solid month. I’m not quite back to my February ATHs but I’m approaching it.

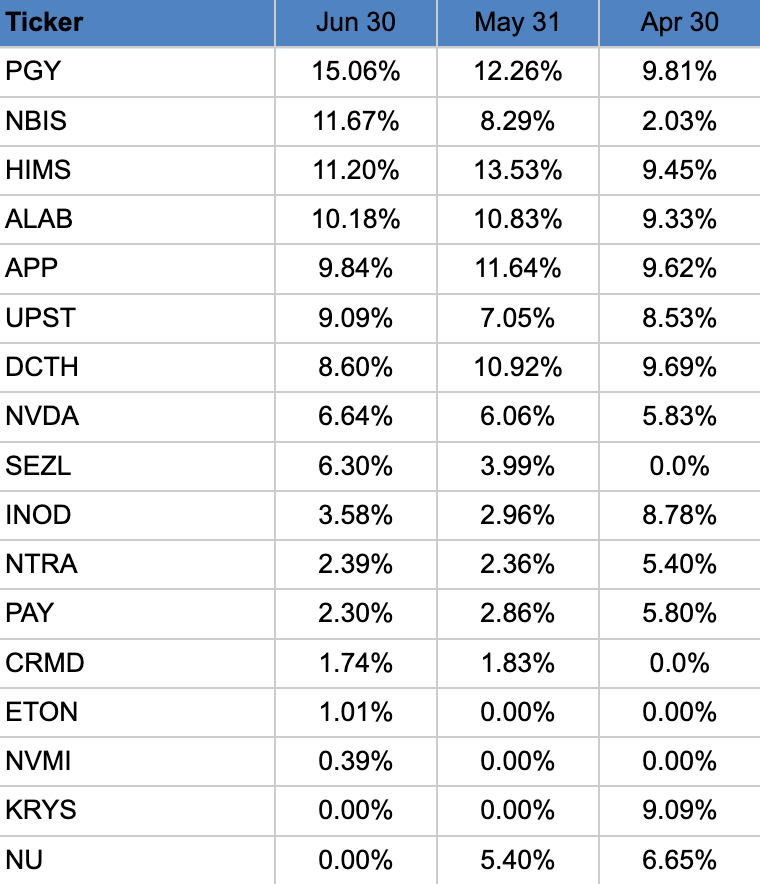

I have 14 positions now, which is a few more than I’d like and I’ll probably cut a few over earnings which will kick off for me at the end of July. I’ll cover each company below and how I reacted to earnings as well as any decisions that were made.

Here are my results to date and current portfolio:

JAN: -1.54%

FEB: +2.77%

MAR: -14.77%

APR: +7.91%

MAY: +24.92

JUN: +11.48%

YTD: +14.68%

(I think the huge off-hours drop from Jan 31 to Feb 1 is not reflected in the above monthly changes)

What I Sold & Why:

NU: -3% May

Another frustrating earnings report where things seem to be going pretty well, key metrics continue to be impressive but also slipping, and I can’t imagine the share price improving unless they were to accelerate revenue or net income growth. After digesting the conversation on the board and the seemingly immovable stock price over the past, I decided to sell out as I believe my money can be better used elsewhere.

What I Trimmed & Why:

INOD: +4.7% May, +29% June

At earnings, they reported a drop in revenue from Q4 to Q1 which should not happen at this size of a company, and only reiterated their guide. I trimmed it from a tier 1 to a tier 3 position in case this is just a blip on the radar, so we will see next earnings if I keep it around. The stock price has recovered some but there has been no news that I’ve seen.

PAY: +17.7% May, -14% June

I wrote about my feelings for Paymentus’ earnings when they dropped. They are predictable sandbaggers, actually guiding to ~5% QoQ drops in revenue pretty consistently, before beating by a wide margin. However, their actual QoQ numbers are dropping quickly: 17% to 11% to 7% to most recently, 3%. So in anticipation of the trend continuing, I sold half my position after earnings and they are now in my third tier. I will also say that I’m really just following numbers with this company vs. my other holding where I understand more about the actual business and the trends surrounding it.

NTRA: +4.4% May, +8% June

YoY Revenue growth slowed from 53% to 36% and they still are net income negative, and also my 2nd most expensive stock when comparing revenue growth to EV/Sales. So I trimmed them back to a tier 3 position as well, selling half my shares.

KRYS: -25.7% May

For a small company, they had a big miss with a drop in revenue in Q1. A shame really because they have great margins and profitability, but I sold out right after earnings.

What I Added To And Why

NBIS: +63% May, +50% June

Big thanks to the board and in particular @Jonathan1 for clueing us in. I doubled my initial position before earnings and then tripled it right after they reported. The annual revenue guide was staggering and represents enormous acceleration in the next few quarters. They moved their way into my #2 position after these two tremendous months.

SEZL: +38.6% Since Purchase in May, +68% June

I was late to the SEZL game even with all the board chatter. My mistake! I wrote it off as a late entry into BNPL but they are continuing to accelerate revenue and income quarter after quarter, and even though the stock has taken off, they are reasonably placed in my affordability rankings.

CRMD: -4.6% Since Purchase in May, +1.5% June

Thank you @ryshab for bringing them to the board! I took a small position after seeing the revenue growth, high margins and profitability. It will stay as a starter position until next earnings since as WPR noted, they did guide for a drop in revenue.

ETON: +1.42% Since Purchase in June

Another from @ryshab, this stacks very high in my growth affordability rankings (#2) so I took a small position that I will add to most likely during earnings.

NVMI: +23% Since Purchase in June

This one is a little pricier but the major metrics are accelerating and so I wanted to get in before it rises much further.

Untouched

HIMS: +70.9% May, -12% June

I thought it was a great quarter and really blew my personal expectations out of the water with 111% revenue growth YoY. They explained that the outlook was temporary. I am not concerned about the fallout with Novo, as I believe it proved that they are scaring the big pharma players. I’m following the numbers and the very confident leadership team.

PGY: +49.3% May, +31% June

I wrote about Pagaya’s earnings, which gave it a modest boost, but the bigger news may have been the latest ABS deal which expands funding capacity by $1B in the POS vertical. Hopefully this gives them no problem getting back to 25% or greater revenue growth moving forward, even with a conservative, profitability-focused tone right now. I’m hoping after a couple more positive earnings results, the market stops discounting this company, who is at 1.8x EV/Sales. They’ve had a great couple of months in share price, hitting a 52-wk high, but have a ton more room to run if they continue to execute come earnings season. I do have some long calls here but I don’t report them to my overall performance.

APP: +44.5% May, -10% June

Another strong earnings report, while they announced they are selling their less-profitable apps division as well. This will make them even more of a money making machine, and eCommerce hasn’t even ramped yet. Happy with them as a tier 1 position even though they are my most “expensive” stock based on rev growth and EV/Sales. I’m not concerned with any of the short reports as they are largely arguments against the entire digital advertising industry. They are annoying, however, for the stock price temporarily.

DCTH: +34.4% May, -16.10% June

Still growing revenue quickly and are on track with their treatment centers, and are now participating in the Medicare Drug Rebate program to accelerate adoption. Staying in Tier 1 until something changes, although the pullback in June has it hovering in the middle of my portfolio.

ALAB: +38.6% May, Flat in June

Earnings saw 144% revenue growth and a strong raise. I have full confidence in ALAB even though the price got demolished in Q1. With the strong NVDA earnings, hopefully people realize that the AI run is nowhere close to over, and neither is ALAB growth. They seem to be expecting a big 2nd half.

UPST: -1.3% May, +37% June

I was super encouraged by earnings and was pretty shocked they actually dropped in price in May. But it has started to increase again in June. In their seasonally slow Q1, they beat earnings by 6.5% which added up to 66% revenue growth, increased Net Income even in the slow quarter, while putting forward solid raises. With a solid beat they’ll be at almost 80% revenue growth…it seems like the market is still recalling getting burnt due to the initial interest rate chaos, but this seems like a different company since then.

NVDA: +24% May, +17% June

I’m sure we all read about their great earnings report, so I won’t cover it much. It’s nice to see it finally hit another ATH, although I can’t imagine it doubling from here like I can with many of my other stocks. But it’s a nice foundational stock I don’t have plans of selling while they keep delivering.

That’s all. Thank you for reading and as always, thank you to all the board contributors for their knowledge sharing. Best of luck in July.