I posted this on the PANW boards and because I know many are interested, I am posting here as well. Randy

PANW Earnings came out after the market closed Thursday and the market clearly loved them as it was up significantly Friday, and after reviewing the release and presentation, I have to agree. Let’s start with the basic headlines from the release:

- Fiscal first quarter revenue grew 25% year over year to $1.6 billion

- Fiscal first quarter billings grew 27% year over year to $1.7 billion

- Remaining performance obligation grew 38% year over year to $8.3 billion

All meeting or beating expectations…nice. Next let’s look at 2023 expectations, all of which were raised over what was reported in August.

For the fiscal year 2023, we are broadly raising guidance and expect:

- Total billings in the range of $8.95 billion to $9.10 billion, representing year-over-year growth of between 20% and 22%.

- Total revenue in the range of $6.85 billion to $6.91 billion, representing year-over-year growth of between 25% and 26%.

- Diluted non-GAAP net income per share in the range of $3.37 to $3.44, using 325 million to 331 million shares outstanding.

- Adjusted free cash flow margin in the range of 34.5% to 35.5%.

This company just continues to hit on all cylinders, revenue growth has been very steady in the mid-twenties and non-gap earnings in the mid-thirties to forties. The adjusted free cash flow margin at 35% is downright awesome, with this quarter’s free cash flow at $1.2 Billion (yes, with a B!). Think about that, so many software companies are trying to turn a profit and these guys are pumping out cash.

Now I know there are SAAS type cloud cyber security companies showing higher growth rates, like CRWD and S, but I think that there is a story behind the story on this company.

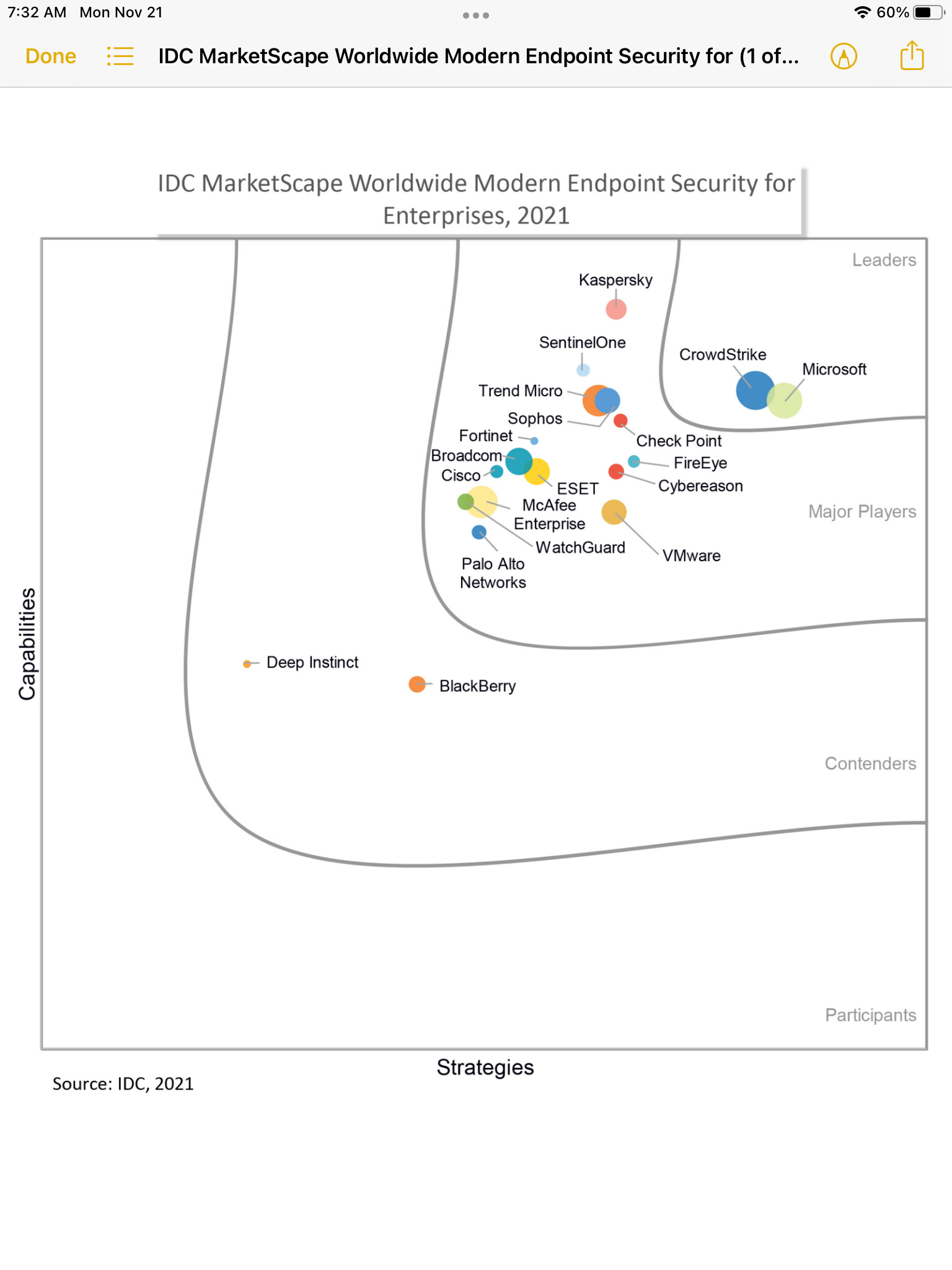

Palo Alto has two sides to thier business, one is the traditional firewalled security software business. It is and has been a great business. In fact, PANW was a growth darling just a few years back. But then along came the cloud with Amazon’s AWS. Shortly thereafter Microsoft and Google joined the fun and now the movement to the cloud is a major theme in the business world. Cyber security is no different and a few cloud only based companies have taken the industry by storm. Crowdstrike and Sentinel are cloud based cyber security companies with Crowdstrike being the first and Sentinel, a more recent entry. Both are growing like gangbusters. In addition, Cloudflare has now joined the fray in offering cyber security along with it’s many other cloud based software offerings.

And ever since, there has been a lot of talk of PANW being the old technology, being out-dated and just living off the old firewalled business. The talk fit the mold of business in general (and being sold hard by the new comers). When there is a technology change, the old dog can’t keep up. They don’t want to cannibalize their existing, growing business so they are slow to change, until it is too late.

But this may be the exception. PANW recognized that cloud cyber security was critical a number of years back and developed their own version. They definitely started behind but it appears they have caught up and are doing just fine. If you look at the presentation they released with the earnings (links at the bottom), you will see on page 15, that the Next-Gen Security (their version of cloud software) has an Annual Recurring Revenue of $2.11B. This is very similar to CRWD, and just as important, it grew at a yr/yr rate of 67%. This accelerated from last quarter when it grew at 61%. The 61% matched CRWD last quarter and it will be interesting to see if CRWD can keep up this quarter. In any case they do not appear to be losing. Yes, Sentinel’s is growing faster but from a much smaller base. The question for them is can they keep it up as they get bigger, definitely someone to keep an eye on.

So we have the big dog incumbent with a great traditional firewall business growing (by my count) in the low single digits with tremendous free cash flow and a cloud based business growing like gangbusters. To me, it is not hard to believe that there are many companies that have a need for both firewalled (extremely sensitive data) and cloud based cyber security and PANW would have a big advantage there. There will also be companies that are in the process of switching to a cloud based system but need to continue firewalled systems for some time, these companies may find it easier to work with one company during the transition as well.

It would seem that if PANW handles it well, they have many advantages in this hyper growth market that it would be wise to not ignore. Not too mention the huge free cash flow to drive further improvements.

To be clear, I like and actually own all 4 companies mentioned here, but I have a feeling that there are many people who think PANW is going to be swept away in the near future. The numbers don’t seem to be suggesting as much. Some food for thought from the PANW tickerguide and happy stock holder.

Link to earnings release:

Palo Alto Networks Reports Fiscal First Quarter 2023 Financial Results | Palo…

Fiscal first quarter revenue grew 25% year over year to $1.6 billion Fiscal first quarter billings grew 27% year over year to $1.7 billion Remaining performance obligation grew 38% year over year to $8.3 billion SANTA CLARA, Calif. , Nov. 17, 2022…

and presentation: https://investors.paloaltonetworks.com/static-files/ca2aa305-a346-46f6-bd48-c09ff2a3e0c9

Randy

Long CRWD, S, NET, and PANW, as well as PANW Tickerguide