Given the recent issues with NYCB, and commercial real estate issues, that will impact regional banks more than big banks, I thought I will start this thread where I could post my thoughts.

Amongst the regional banks, OZK, Bank of Ozark, Little Rock Arkansas, has greatest exposure to NYC CRE at $4.5B (17% of loans) and total office exposure at $5.1B (19% of loans).

The above is from Wells Fargo, and they have taken the price target to $39, while the market price is $42.5. These loans are not going to go bad overnight. It will take some time as the loans mature, the true value of collaterals will be discovered, etc. So, it may be difficult to short the stock, as the catalyst may take some time.

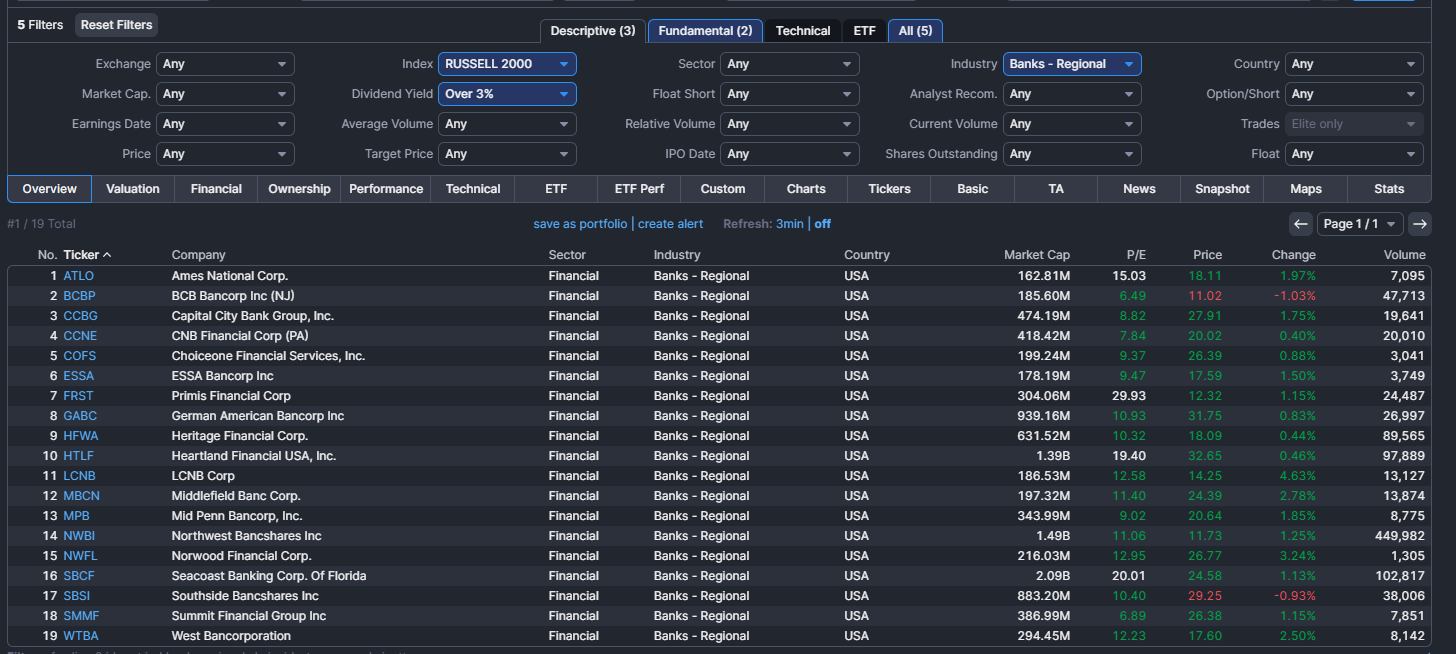

I ran below screen on finviz.com site, Regional Banks, dividend > 3%, part of R2K, and have positive Insider transaction, i.e., Insider buys. There are 19 stocks. If Insiders are buying, it may be worth a bet. Of course like any other screen, it is only a starting point. Please do further research into these names. Separately this tells me the KRE may not be a bad hold.

Yesterday NYCB announced they cannot file 10-K because of internal control issues. So it is not like they suddenly realized they have “internal control issues”. I think regulators are going through with fine-tooth comb. If you do that with any firm, you are going to find few things. NYCB is not going to get out of this anytime soon. I think NYCB is being made an example, but the wider implications is, all banks will be subject to/ or voluntarily they will review their operations, i.e., take less risk, spend more money on fixing issues, i.e., non-interest expense will go up. The small-regional banks have real estate headwind and higher expenses to deal with the regulations.

As of today, I have completely out of all regional banks.

I still own large banks, Citi, WFC and BAC. They have all gone through regulatory review and their regulatory related expenses are well known. On any weakness I will buy more Citi and WFC.

Financials are rallying and the big banks have all moved up. if the interest rates stays higher, it is going to be positive for WFC, and the asset cap could come off sometime this year and that will become a tailwind. WFC could move higher even from here.

The 1st bank failure of 2024 is here… It is relatively a small bank, yet FDIC is going to take $667 m hit. Wondering why FDIC waits so long and why not move early and minimize the hit it takes?

There are still commercial real estate risk, new liquidity requirements (i.e., banks with over $100 B deposits are going to require higher reserves) are going to impact regionals.

Huntington Bank yesterday in Morgan Stanley conference mentioned their NII will be -1% to -4%, they reduced it from 2% to -2%. The reason behind that is deposit costs are high and loan growth is slightly bad. Both are not unknown, the FED data was showing loan growth is weak and we all know the deposit costs are going to be higher than original forecast because the expected rate cut hasn’t materialized yet. Still banks are forecasting rates will be lower in the second half and this could bring some more pain. Separately, the buyback is going to be on hold.

In addition to this, PIMCO is forecasting CRE defaults is going to start anytime … so far the banks are not talking about any CRE deterioration and most of the office challenges are known and hopefully banks have provisioned… It could be PIMCO trying to talk about real estate deals but nevertheless it impacts the market.

One of the interesting facts/ data to emerge from the stress test is the the cumulative loss expectations for banks on CRE is flat y-o-y. This is significant, it means the banks are addressing the CRE exposure risk. You could see that reflected in almost 3%+ move in KRE since.

Texas based First Foundation bank basically sold 50% of the company… This is to address any potential issues on their multi-family loan book. So banks have learned a lesson they are raising capital first before selling parts of their existing loan book unlike SVB.

Today’s inflation report is very encouraging for the regional banks. The inflation is down and down way more than folks expected. The interest rate cuts are coming. This may the ideal time to get into KRE and probably get out after the initial cuts are done.

With lower interest rates, and the bond prices appreciating, many banks will be erasing some of their AOCI losses, and pushing their book value higher. Some of the banks have already taken the loss and locked in higher rates. Two regional banks where I have some small allocation Key, and TFC are going to benefit. Of this KEY has already moved up due to the stake sale, TFC is at the sweet spot, with 5% dividend, a good candidate for covered call.

I kept buying some more subsequent to this. Overall, my position is up 30%. While I am booking profits on big banks and few regionals I directly owned, I am keeping this one. Some of the catalysts for regionals are:

Loan growth

NII growth, many regionals have recast their balance sheet, i.e., sold some legacy bonds and bought higher yielding bonds, basically booking some losses, but setting up better NII in the future

M&A and capital market is going to boost many banks. It is not just Goldman and Citi

Regulatory relief, reduced capital requirement and buyback, many had missed the opportunity to buy at low’s

Lastly on risk, CRE issues are still there, and would play out over 2025, and 2026. So you need to know which bank has issues, where the risks are hidden. If you cannot do that kind of analysis, stick with the index, that’s what I am doing here.

I originally bought on 5/22/2023 for $40.35 and sold at $49.30, excluding dividends 22% gains I booked, subsequently again I bought 06/06/2024 for $47.2… now I want to sell but worried about taxes.

Even though selling and buying back at lower price and avoiding difficult 6 month holding, I have made overall $2.15 per share, because of taxes, long-term and short-term tax rates, after tax i will have $3 less now, instead if I just held my original shares on I bought and sold them today.

I have so far not paid much attention to taxes… now I am waking up to short-term vs long-term gains and the difference…

One of the earliest lessons I have learned as a programmer, over a quarter century ago is, a single module optimization should not lead to sub-optimization of the whole. Yet, I keep forgetting that lesson. Trying to optimize my taxes, stopped me from exiting many positions. I should have sold at $70.

I think the post SVB recovery is mostly done. From now on, picking the correct stock will provide the most of the alpha. Some of the headwinds are:

Commercial real estate

banks hold most of the CRE debt; and big banks have reduced their exposure, OTOH regional banks hold the most (70%);

Banks with $100M to $10 B assets have loans that are 30% to 35% of their assets; Compare this to money center banks have only 6% exposure and they have higher quality assets

Funding cost

Still Big Banks pay very little on their deposits (0.01%) Savings and Certificate of Deposit (CD) Interest Rates | Wells Fargo, whereas Regionals have to increase the interest rates to stop the bleeding of deposits to money market, i.e., their cost of funds are far higher

$1.5 Trillion moved to money market

Interestingly, after Fed started the interest rate cut cycle, the long-term rates have increased!!! that means the funds in MM are not coming back any time soon; in simple words, higher for longer

The small banks have higher % of brokered deposits, that is they are not able to attract deposits from their customer base and are paying higher for the deposits

I will try to find some names where the balance sheet strength exists, loan growth is possible, have strong deposit franchise. But the low hanging fruits are gone. For now, I need to find a way to get out of KRE , shake the price anchoring.

The big banks have mostly addressed their CRE-Office exposure or they can take any write offs’ in stride. The regional banks/ small banks are the ones who have exposure. Especially on the multi-family side.

If the mortgage rates continue to stay high, refinancing the multi-family homes are going to be a challenge. This may provide pockets of opportunity. The time to long KRE (regional bank Index) is over and go selective on individual name is here. Still I am dragging myself from switching from KRE to Individual names.

$TFC in a industry presentation reduced revenue estimates, primarily related to capital market. Expect many more banks are going to do that. The so called “animal spirits, IPO Book, M&A boom” are not happening or at least on hold for now. So everyone is going to adjust their estimates and walk back some of the estimation they baked in.

The good news, it is also going to reduce the expenses associated with those activities. Overall EPS is not going to be impacted big time, but will come down a bit. For $TFC no EPS impact.

$TFC’s price decline presents an opportunity for anyone wants to buy long-term. The dividend yield is getting to 5%, and the tangible book value is $30. Alternatively you can sell $30 Jan 16 Put, for $1.05 and just benefit from the volatility coming down in few months or take shares at $30, at which point the dividend yield will be… 7%.