Highlights

-

Revenue growth continues to accelerate (YoY: 22.80% → 22.97% → 30.76% → 37.51%).

-

Profitability continues to improve on a GAAP Net Income basis. (GAAP Net Margin: (0.63%) → 2.1% → 3.54% → 4.79%)

-

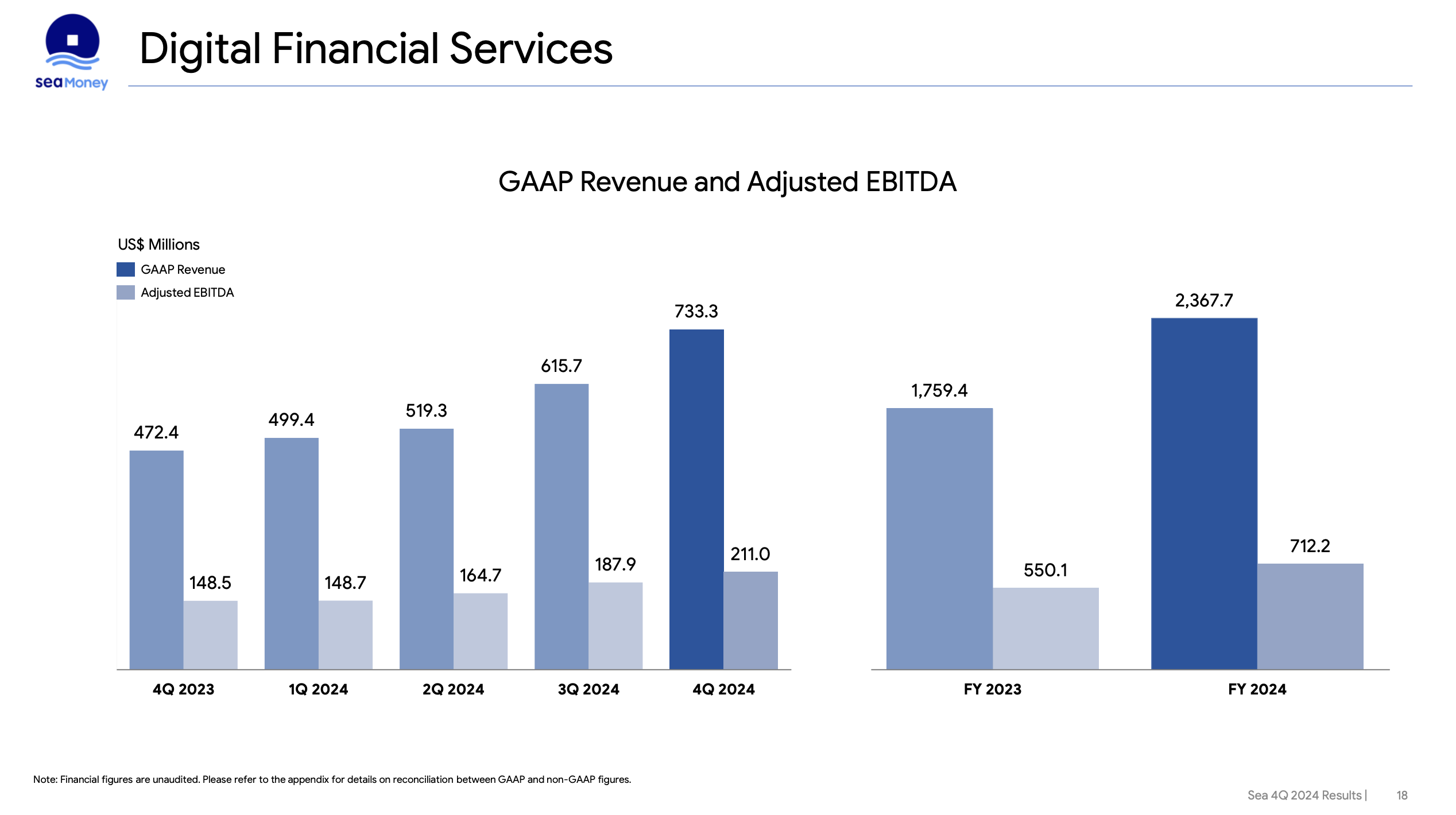

The Digital Financial Service segment was the biggest driver of acceleration. (growth YoY: 21.36% → 37.99% → 55.23%)

-

The E-commerce segment remained strong. (growth YoY: 32.66% → 45.45% → 42.31%)

Some downsides

- E-commerce take rate stayed flat QoQ.

- The gaming segment is still dragging down the overall growth with booking shrinking 2.39% QoQ. It currently only accounts for ~10% of the total revenue.

Outlook (copied from Seeking Alpha AI)

- The company expects Shopee’s full-year GMV to grow around 20% in 2025, with continued profitability improvements. Management stated that improving service quality and operational efficiencies, particularly in logistics, will drive this growth.

- SeaMoney’s loan book is projected to grow meaningfully faster than Shopee’s GMV in 2025, with further SPayLater penetration both on and off Shopee in markets like Indonesia and the Philippines.

- Garena expects double-digit growth in bookings and user base for 2025, supported by the sustained popularity of Free Fire and new content collaborations.

Links

Long 5%

Luffy