TMDX performed exactly as I was hoping it would and followed the strong flight data that is easily tracked daily. No idea why anyone would sell going into earnings.

-I was looking for at least $140 million in revenue and FY guide raise to 30%. This is exactly what happened so I’m happy. $143.5 million and they raised FY Guidance to 30% at the mid-point.

-The Price Action tomorrow will be very interesting. Might get a short squeeze as shorts will likely have to start covering soon. I’m surprised its only up 10% AH.

TransMedics Group press release (NASDAQ:TMDX): Q1 GAAP EPS of $0.70 beats by $0.45.

Revenue of $143.5M (+48.2% Y/Y) beats by $20.11M.

Raising full year 2025 revenue guidance to $565 million to $585 million

Owned 21 aircraft as of March 31, 2025

Announced strategic plan to open design center of excellence and new disposables manufacturing facility in Mirandola, Italy

“Overall, we are very pleased with our first quarter performance, which we believe underscores the unique attributes of our business and the ability to deliver strong top and bottom-line financial results,” said Waleed Hassanein, MD, President and Chief Executive Officer. “We are confident in our ability to sustain this momentum through 2025 and beyond by remaining laser focused on operational execution and leveraging the unrivaled capabilities of OCS NOP to expand the utilization of available donor organs for transplantation. Ultimately, this will enable us to deliver what we believe to be the best possible clinical outcomes and most cost-efficient therapy for our transplant patients. We are grateful and humbled by the unwavering support of our clinical transplant partners and the resilience of our exceptional team.”

I’ve got a bit of history with Transmedics. I bought a good sized position not long after they were introduced here on Saul’s board. The stock price didn’t exactly take off, but I kept my position until they announced their intention of buying their own aircraft and becoming a logistics company as well as a medical service provider. It just seemed like too much diversion of attention to manage a complex business inside of another complex business. I sold my stock and missed the run up. I don’t know why I didn’t buy back in sooner, but I didn’t.

But then later, I bought back into TMDX a while ago. My timing could not have been worse. After the substantial runup after I sold my initial position, I bought just in time to catch the erosion in the stock price.

But, I bought in again recently primarily due to the flight info posted here on Saul’s board. I don’t recall the name of the poster, but if it was you, thanks. This time my timing was spot on, I got on board just in time to catch the pop after the earnings report.

It’s very unusual for me to take a position without doing more intensive research, but I’ve always liked the company. I think they deliver an invaluable service in the critical medical area of organ transplants. In addition, the management team always seemed to be very competent. And they proved that they could gainfully manage the logistics business along with the medical services that was the initial reason for their venture.

So my confidence in the company was already quite high. I figured the flight information was indicative of a return to growth. On the basis of the flight information and my gut, I bought back in. I’m glad I did. I expect more quarters like this one will follow - but yeah, I’ll do a bit more due diligence.

I’ve owned TMDX for a couple years. The slowdown last year was tough but I trusted the management team and averaged down. The flight data is key. They continue to execute in real time. Tomorrow will be interesting with 27% short interest.

Is anyone concerned that the full year guidance implies no growth from Q1 '25 to Q4 '25? Revenue this quarter was 143.5 and the yearly guide is 565-585. Are we hoping they’re sandbagging?

In the past, I would have bet that they were sandbagging. They have a history of sandbagging 95% of the time. The problem is that the one time they wound up not sandbagging, the stock got crushed. I don’t think we can any longer assume that they are sandbagging. (They probably are, but I’m much more cautious about it now). Personally, I think hypergrowth is over, but I think it’s a great long term hold with potential for solid YoY growth for many years. I am still holding some shares that I have held almost since they were public - although many less shares than I used to have. I too have made many mistakes in how I handled this investment. It’s been a great learning experience. I made a lot, but I could have made so much more. I had extremely high conviction, but I let myself get scared into selling at times of extreme downturns.

Its been a volatile stock that tested conviction for sure. Now that we have the flights to track, you can just follow that so there is a lot less guessing. Q2 flights are up 17% QoQ so we might be looking at another strong print if they can keep it up.

TMDX just filed a 15G because Fidelity now owns 15% of shares outstanding. SEC Filing | TransMedics

TMDX up 115% from January lows, up 84% ytd. I’m hearing rumors that overall transplant numbers were up bigly in April. I’ll post once we get some numbers. I have a 25.5% position in TMDX. I’ll probably start to trim a bit if it goes above $140. Fair value is somewhere around $170. Today is a good reminder that you shouldn’t try to time the market. My portfolio is up 10.5% ytd, even with my hedges dragging a bit, so not too shabby. Still a lot of uncertainty but the chances of a recession seem to be reduced. TMDX is recession & tariff proof anyway but certainly has other risks.

More bullish news from TMDX. The stock is up 91% ytd and I have no plans to sell a single share anytime soon. The monster numbers from the overall transplant volume are out.

Total transplants up 10% YoY

DCD transplants (mostly TMDX)… up 79% YoY

Liver DCD transplants up 84% YoY

Heart DCD transplants up 73% YoY

Lung DCD transplants up 59% YoY

TMDX up 112% ytd and almost 150% off of Jan lows. June Flights up strong, averaging 30/day so far. I’m still holding a 25% position and looking to start gradually trimming a bit if it runs up to $140-170. Large Institutions seem to be getting on board. Large beat almost guaranteed next quarter. Will be likely at least 15% over consensus.

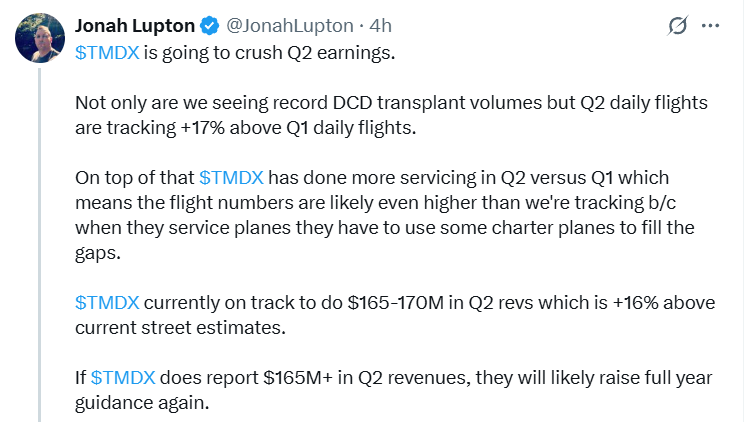

TMDX flight tracker... 304 flights through 10.9 days... on pace for 2472 flighs in Q2 which is 16.9% above Q1. The stock is up about 122% ytd. Still sold 26% short, which will likely continue to get slowly squeezed out of the game. 2 months ago the short interest was 34%. According to Jonah Lupton's calculations, TMDX is on track to beat Q1 estimates by about 17% and revenues are tracking to be up 20% QoQ.

I was invested in TMDX long time ago, believed in them when they first announced the plans for building their fleet and everyone got scared and sold the stock. I kept and kept until they stumbled last summer. Now it looks selling the stock was a mistake, although the stock took lots of time to recover.

Now, thanks to you @FoolishJeff , I am back in. The data you share with us helped me to start re-building my trust with their CEO, which I find a very capable person, knowing what he is doing and how to achieve his plans.

I too was in TMDX until they announced that they were going to buy a bunch of aircraft. That sounded just nuts to me. I couldn’t think of what they might do to depart further from their core business. In my mind medical equipment/procedures and logistics didn’t mix. I sold my position. Turned out I was wrong until I was right, after missing quite a runup in the stock

But, just like @IamM, I saw renewed opportunity after reading a post by @FoolishJeff. I did a bit more investigation and a pending recovery seemed very likely, I bought back in last April. Then I doubled my position a month later. TMDX is now close to 10% of my holdings. I don’t plan on buying more, but I don’t plan on selling any shares either. So I owe a big thank you to @FoolishJeff.

Glad some folks are doing well in TMDX. If OCS 2.0 gets approved soon, then it will likely cause the stock to spike 5-10% and should contribute meaningfully to the 2nd half of the year. TMDX has had a little pull-back to the 20 day moving average. I think it’s a healthy pull back after the big run-up. I even added a little at $124. Flight numbers continue to look strong, although things have slowed the past few days due to more servicing. It’s in the bag that TMDX will beat this quarter by at least 15%. Go TMDX!

TMDX is going strong and we know that they will have big beat next quarter. They will also have to raise their full year guide, which should really get the stock moving.