Glad I retired before it hit the fan.

intercst

Glad I retired before it hit the fan.

intercst

I think you mean: Glad I have medicare before TSHF.

Right?

Retirees who are looking for ACA marketplace plans are in question here.

No. I was one of the pioneers of “free Obamacare”.

The last few years before I reached age 65, my premium was $1.42/month – less than $20/yr.

I’d budgeted $20,000/yr for age 60-65, for-profit, unlimited price gouging, private health insurance.

intercst

Thanks for sharing, I’ve never watched Breaking Points. Good production and the hosts dropping F bombs…I love it!

I think you misunderstand my point. You were able to reduce income by reducing consumption to below the threshold levels and by converting income appearing retirement account values to minimum through taxable conversions, right?

You’re on Medicare now, so, it’s a moot point.

They don’t usually do that. But they understand the arithmetic of US health care and get very angry when talking about it.

intercst

No, not consumption. Taxable income. i focused on taking my income as qualified capital gains and tax-paid returns of capital to the maximum extent possible while reducing interest income and dividends. And of course, any kind of wage & salary income.

If I sell a $100,000 block of stock I bought for $80,000, I have $100,000 in annual spending money but only $20,000 in taxable income.

Of course, with time you end up with a portfolio of long held positions with a tiny cost basis. Everything I could sell today is almost all qualified capital gains with a near zero cost basis.

intercst

Yes, thanks. I understand what you did (though my post wasn’t precise in explanation).

Perhaps we can turn this around:

Would you mind starting (at 38 years old) again “today” and deal with the reduced subsidy for “poverty” income.

Potential changes for 2026

If Congress does not extend the enhanced subsidies, significant changes will occur >for the 2026 plan year, including:

- The 400% of FPL income cap for subsidies will be reinstated.

- Enrollees, particularly low- and middle-income families, will face higher premium costs. For example, a family of four at 140% of FPL with a $0 premium in 2025 could see premiums rise to over $1,600 per year.

This is quite an interesting evolution because, presumably, even if you slanted significant savings to “post tax” or ordinary account types, an early retiree would risk running out of savings which maintains this artificially low “income” declaration.

If your budget is $96,000 (total portfolio of, say $2.4 Million and 4% swr) like the example above, and you have 50% post tax/ordinary sources, the portion of income which could be supported to minimize health care expenses is ~ 20% or $21,150 for 2025 (Married. Even less, if single).

The 2025 federal poverty level (FPL) starts at $15,650 for a one-person household in the 48 contiguous states and D.C.. For Alaska, the level is $19,550 for one person, and for Hawaii, it’s $17,990. The poverty level increases with each additional person in the household.

This means that no more than 16.3% of your annual requirements can come from pretax savings accounts. ($15,650).

With a 50/50 mix of pre/post-ordinary accounts, you would be depleting “only” 1.3% of your taxable income retirement accounts and 8% of your post tax/ordinary accounts.

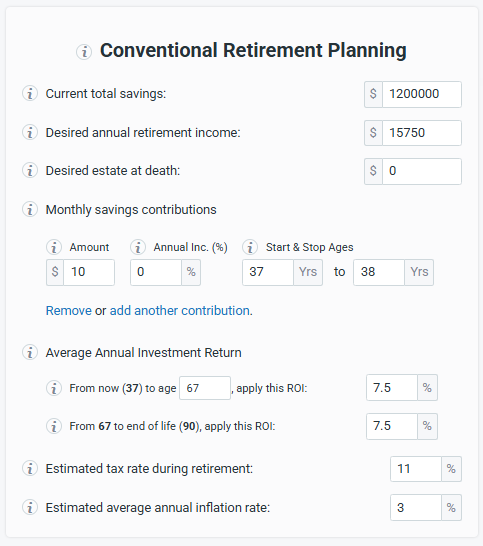

Over the course of many years between today (at 38 years old - again starting over) and your eventual future 65 years old self. 27 years! would have to elapse at an 8% withdrawal rate. We can see the results of this overburden on the charts below:

Calculation details are presented here:

Alternatively, the taxable portion of retirement is shown here $15,750 in taxable income (as required to maximize ACA subsidy).

- Marginal Rates: For tax year 2026, the top tax rate remains 37% for individual single taxpayers with incomes greater than $640,600 ($768,700 for married couples filing jointly). The other rates are:35% for incomes over $256,225 ($512,450 for married couples filing jointly);

32% for incomes over $201,775 ($403,550 for married couples filing jointly);

24% for incomes over $105,700 ($211,400 for married couples filing jointly);

22% for incomes over $50,400 ($100,800 for married couples filing jointly);

12% for incomes over $12,400 ($24,800 for married couples filing jointly).The lowest rate is 10% for incomes of single individuals with incomes of $12,400 or less ($24,800 for married couples filing jointly).

As we can see below (and, you referenced above in earlier posts), the problem of account type imbalance becomes clearly in focus. You must underspend on your taxable income streams and OVER spend on your tax free streams to maintain the subsidized health care regime.

While this scenario does not imply anyone falling short of goals, the implied risk is that more and more income must come from the taxable sources, which magnifies tax regime change risk and health care expense inflation risk as well (by extension of subsidies no longer applying to annual income stream declarations).

Indeed, while health care needs increase, subsidy as a proportion of expenses decrease. In this scenario, the retiree would be faced with a triple whammy if health care inflation, taxes and subsidies work against the plans.

This was my point above. Am I missing something?

Yes!

I only had Obamacare coverage for 5 years, and I started getting my portfolio “Obamacare ready” shortly after the legislation was passed in 2010, when I realized that they were only using income (and not assets or net worth) to determine eligibility.

intercst

Don’t forget that the income required to maintain a big tax subsidy varies by state. The last year I was on Obamacare (2020), you could have an income over $50,000/yr in my WA State zip code as a single person and still get my $1.42/month premium.

The first thing I did when the Obamacare premiums were released each October was find the maximum income that allowed a $0 month premium. It looks like for 2025, it’s about $47,000/yr

intercst

We are LTBH, mostly. You are correct that our cost bases are often small. I can specify lots since I started doing that with company stock prior to the rule that you couldn’t do that anymore. I have ESPP where the cost basis is around $1, while the stock is roughly $70. If I have to sell any, I can specify the shares acquired shortly before retiring (or my RSUs which I had to pay tax on at the time, so the cost basis effectively was stepped-up).

1poormom’s assets were mostly cashed-out. I took advantage of the stepped-up basis, and have been living on that cash for the last few years. Just the RMD from her IRA has to be taken today.

I’m not looking forward to seeing the premiums next month. Fortunately, I haven’t had to sell anything this year (except the RMD). I am stuck with dividends from my company stock (liquidating it would create large gains very quickly). All I can do is minimize the income by not selling anything (without offset losses, which I have a little).

2.5 years to Medicare for me. 3.5 for 1poorlady.

Last year, we paid $3900/month for a period (never made a single claim on that policy). My wife quickly got tired of paying that much, so she took a part-time job with medical benefits and we’ve been using those for the duration.

That is quite a lot. I think our unsubsidized premium would have been something like half that. Just a bronze high deductible plan. Really only covers us if something major happens. Otherwise, we get whatever insurance discount the provider has to do, and we pay the rest of the service. Gets applied to deductible which, hopefully, we’ll never meet.

That would be great. This year, we exceeded our family deductible ($10,200 I think) and now my wife has been making appointments for everything before the end of the year. Had a cardiac test last week, a gastro appointment last week, dermatologist next Monday. PCP appointment next Wednesday. And in about 3 weeks a colonoscopy (last one was in 2019 so it’s time for the next one).