With the exception of the last 4 years of course.

4 Likes

I’m looking into a of couple Stupidity ETFs.

1 Like

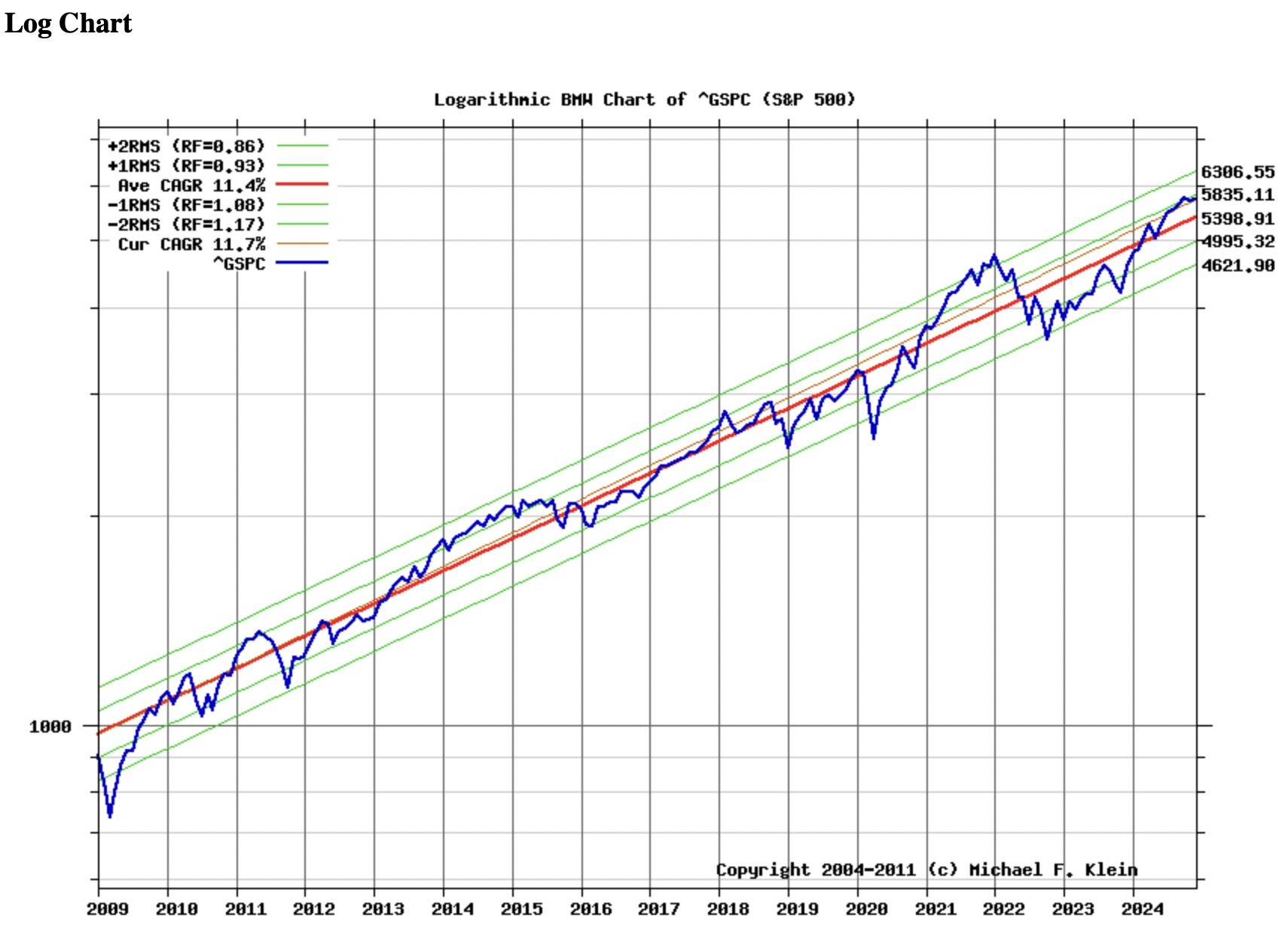

That I think would be a big mistake. The S&P500 mean PE is about 16. Over the past 10 years it has been about 24, pushed up I suspect by the spectacular rise of the Magnificent Seven (which make up an unprecedented 25%-33% of the S&P 500 market cap). Today the S&P500 PE is at 30.

The broader market is currently expensive by most any historical measure. It is far more likely to go down than up over the next couple of years.

When Trump took office in 2016, the market was still in the recovery phase from the Great Recession. The S&P leveled off during the Trump years before the pandemic. The Trump impact on the broader market was undetectable. Look for yourself:

I will be gradually moving money out of the broader market until the S&P 500 PE drops below 25 (at a minimum).

2 Likes

A Nobel Prize is not a guarantee that the recipient knows what he is talking about! ![]()

The Captain

3 Likes

Nice chart! But if you are going to start from the lows of the Great Recession, it is not surprising to see a rising S&P. Here is another Chart showing S&P 500 performance over a longer period.

Note that an S&P 500 investment in 1999 would have been in the red for another 15 years. Those approaching retirement may not have a long enough investment window to withstand something like that.

Keep in mind that the stock market performance since WWII occurred during a period of favorable age demographics for the West and economic globalization. While globalization can disrupt specific industries in specific countries, the overall effect is to stimulate economic growth by greatly increasing productivity and efficiency.

We are now entering a far different period. Demographics in most of the advanced economies favor economic decline rather than growth. Globalization is in retreat and protectionism is on the rise, suggesting we may be heading to patterns of stock market performance more representative of the preWWII mercantile age.

We also have this strange situation where Americans want to restrict immigration at a time when aging dependents are growing faster than the work force. The result of a declining workforce in an aging population can be seen in Japan’s Nikkei stock performance:

This is a collective shooting ourselves in our foot. The question we all should be asking is whether the US market is approaching where Japan was in 1990. How many here can withstand 30 years of flat returns?

Raising tariffs, restricting immigration, and deporting a big chunk of the workforce doing essential manual labor strike me as being absolutely the wrong things to do at this time. We are burying ourselves in a Quixotic effort to keep America White.

I see tariffs and worker shortages in major industries slowing the US economy in 2025, which combined with rapidly slowing economies in China and the EU and a still stagnant Japan will lead to a global recession by 2026. This will likely be led by the decline of legacy automakers in the west who are all carrying huge amounts of debt. I don’t believe the growing economies of India and Africa will be enough to mitigate this slowdown. I also don’t believe the incoming administration or congress has the expertise to deal with such an economic crisis so it wouldn’t surprise me if it lasted awhile.

We have had a good run since 2009 thanks to Obama and Biden who rescued us from the Bush Bubble Economy and the Trump Pandemic Fiasco. It may be time to get defensive.

12 Likes

From 2017 to 2021 he was very ineffective.

The splits in congresses will be the largest seen in American public life since the Civil War. Except some states were not seated during the civil war.

We do not know who will control the house. Either way it will be ungovernable.

Yes you have nailed Musk. He is a transactional business leader. He wrung subsidies from both the US & China! A great move.

Mr. Trump is widely regarded around the world as a transactional leader.

Does the president pull the rug out underneath Musk after Elon aided the president’s election? I think not as long as Elon continues to make nice with him. Because then no one would deal with him.

1 Like

Also in this case, the person had won the prize as an economist, but he has since changed to become a social commentator. He’s not getting any prizes for that.

Where are you putting the money in the meantime? And how long will you give it to hit that 25 mark? (By the way, 25 is also historically kind of overvalued!)

I also expect a market downturn someday. I am not convinced that the fed has cured all recessions even though it sometimes appears to be that way. The one big issue I have is that almost the entirety of my equity investments comprise long-term capital gains, so if I sell, it’s all taxable.

3 Likes

Then we get government by “Executive order” and rulings by SCOTUS.

Steve

2 Likes

One of the items on the agenda is a Federal work requirement for Medicaid. This is something TFG experimented with in the last go around. Michigan, firmly in the control of the Shinies at that time, was one of the states that participated in that experiment. The (L&Ses) who pushed the legislation through admitted the entire objective was to force people to take the lousy jobs the “JCs” were crying they could not fill.

Demand for manufactured goods may be limited, but, I would suggest, the capacity for financial manipulation and speculation is unlimited.

Steve

1 Like

Auto Zone is already announcing price hikes and lay offs due to what is about to come. We are entering the “find out” phase of his policies already.

I have been thinking more. Broad indices I think are not where to be, simply because of the extreme weighting of the Mag 7, which I think will get hit harder than the average stock. So I’m thinking more VTV, more VFMV. Maybe individual short duration Treasuries, held to maturity. Will not buy a bond fund.

1 Like

Why would you not buy bonds?

I will not buy a bond fund. Individual bonds a different story. However, I’ve learned that researching corporate bonds involves much more work than I currently have the bandwidth for. Treasuries are a different story.

Speaking of government bonds, I’d avoid any agency bond as well, not in this climate.

2 Likes

I’m inclined to be in btresist’s camp.

First of all, the majority of my equity investments are in an IRA, where capital gains are irrelevant. I can trade all day long with no immediate tax implication. However, everything withdrawn is ordinary income. My biggest mistake was missing out on putting more of my retirement savings into a Roth, but that’s water under the bridge for me (I’ve taught my kids to be wiser).

My plan is to build my cash position, putting the money in ST CD ladders and keeping all my CDs below the FDIC levels. I haven’t set a target for when I’ll reinvest. I’m assuming it will be like corn (ok, use your imagination, auto censor at work), I’ll know it when I see it.

I’m seeing a “Be fearful when others are greedy and be greedy when others are fearful” moment. Currently, I’m seeing a lot of greed and stupidity. And you can’t fix stupid. I’ll leave it at that for now.

9 Likes

That has been the trend since Nixon.

Why else all the recent foreign adventures.

You might enjoy:

That last sentence is the big downside. The second big downside is no basis reset on death. That’s part of why I had most of my aggressive equity investments outside an IRA, because it is taxed at 15/20/23.8% instead of 24/32/35% and when I die it is taxed at 0%. The second reason, of course, is because most of the money I saved was outside tax-deferred (or tax-free) accounts.

I made the same mistake, didn’t open a Roth IRA until late, and then became ineligible. Didn’t ever do a backdoor Roth contribution. And only switched to Roth 401k two years before retiring.

Same here! My kids that are working have started right away in a Roth. It’s a literal no-brainer at their current lower tax rates.

When Treasury bills yield higher than CDs, I use T-bills.

When CDs yield higher than T-bills, I use CDs.

Right now T-bills have been winning the race for the last few months, and twice a week I buy all the T-bills (just to keep a nice wide ladder because those T-bills are what fund my daily/weekly/monthly spending). Sadly, the last of my 5.4-5.5% CDs are maturing next month.

1 Like

Would you prefer this over money markets? If so, why? Curious as I have too much in money markets right now.

1 Like

Morgan Stanley floated that idea to me in 2008 but they did not push it very hard. The problem was taxes and an inability to predict the future. And do not fool yourself, your kids will have that very same problem a few decades down the road. I was in a high tax bracket then, expecting to be in a low tax bracket in the future, so the choice was not clear. I did not convert.

When I was young I thought I was doing everything correct, compared to my parents who relied on whole life insurance and pensions and social security. They, of course, thought they were doing everything correct when they were young. Now we are learning we could have done better, different. Young ones today will have the same experience we had, and our parents had.

Do not think you can predict their situation 3 and 4 decades down the road. We could not predict ours.

7 Likes

Because of inflation expectations?

DB2