It is a shame we lost all the earlier posts on this name.

Lumber prices are declining and at this level soon lumber manufacturers will not be making money and they will start cutting production. Alternatively China demand may pickup, btw, it has never really recovered post COVID. I am not sure the industry has an ability to adjust quickly. We need to see.

WY stock price is slowly declining and it is at 3 year low. WY has increased its revenue streams but their primary business is lumber and if the prices goes down it will impact them.

If $WY gets closer to $20, I will be a buyer. I am not expecting it to happen quickly, it will be like watching paint dry or if you prefer, watching the trees grow, in Southern US trees typically grow for 20~25 years before they are ready for harvesting for saw logs and in Western US (my backyard Washington) it can grow up to 30 to 40 years. So patience is not a virtue but a basic requirement in this business.

China manufacturing is weak, PMI @ 49.1, employment and raw material inventory are at contractionary territory. Yet across the world for ex: Brazil new capacity are coming online.

The price moved up to $30. The below 5 year chart shows a strong support around $27.5 and resistance around $35.

There was a period I used to trade stocks in range, no longer. REIT’s often trade in ranges and generally I was successful trading them in range. However, option bid-ask is so wide, that makes using options suboptimal. So you have to buy the stock, collect the dividend and get out near the upper range and then wait again patiently.

For those who enjoy clipping coupons, these are good ideas.

Interesting that you mention WY in the context of clipping coupons.

Got into their 7-3/8 of '32 back in '08 at 69 and change for a projected YTM of 10.7%. Got into their 7-7/8 of '26 the same year at 64 and change for a projected YTM of 12.6%.

And I agree that those kinds of opportunities still exist if one knows where to look and is willing to do the needed due diligence and to accept the obvious risks.

The lumber prices rose from July bottom and along with that the stock price moved up and now lumber price is rolling over and the stock is declining.

WY, showed how difficult for the lumber companies to reduce the harvest, they guided for 4Q the timber harvest will be reduced 35.5 mn tons to 34.5 mn tons, that is less than 3% reduction.

The industry and WY in particular faces headwinds that they can hardly control:

Housing demand

China Demand

Regulatory issues, currently China has excluded retaliatory tariffs on lumber, so it can remove that exclusion anytime; Don’t blame china, blame US policy on this.

On the positive side,

Their lumber and wood products neutralize each other in pricing cycles;

WY has strong balance sheet

reduced dividend commitment, i.e., before 2020, they had slightly over $1 B in dividend payout; now they switched to fixed+variable; This is still hefty ($600 M) in committed dividend and the rest is based on FAD generation

The timberland recycling resulting in better timber holdings

Lastly, they own 10 m timberland, valuing at $2000 per acre (note they have different types and in different geography, I am just using a short-hand here), that is worth $20 B, then they have wood products division and $5 B in long-term debt. The cash on hand is equal to various other liabilities and a wash. So one has to be patient to enter at the right price. This is not your typical growth company… here things take decades to grow!!! OTOH, the land, and timber are true store of value!

WY has 7 million acres in the US South. WY has $45 per acre EBITDA on the south, compared to the industry average of $60. These trends cannot be reversed quickly, as this involves location (closer to mills, ports), silviculture (higher yield plants, species, etc), age of the stock, etc. However, this is a long-term potential. If they can get this to the industry average that would be 35% increase or $100 M higher EBITDA. Of course it will take time, given their size they may not be able to optimize and they may never catch up.

Separately, in PNW (WA & OR) WY has the industry leading EBITDA per acre.

While in the short-term it is a headwind, in the long-term it is a tail-wind. US has a housing shortage and aging housing inventory. How it is going to address is to be seen. However it is a tailwind for timber REIT’s and home improvement duopoly.

After reviewing Q4, Q1-2025 and overall 2025 guidance, nothing much has changed. 2 items of note are:

they announced a $500M new timberstrand facility, expected to be completed and operational by 2027

Cost overrun, project delays is a concern, also capex takes away cash otherwise available for buyback.

Timberstrand is typically produced from Hardwood, and $WY is trying to produce this from Southern yellow pine, which is a softwood lumber; We need to see whether market embraces this; but there is that acceptance risk.

Announced natural climate solutions did $84 M EBITDA and expect $100M EBITDA

This is a nice development for the company; However, with the current administration, the ability to monetize carbon credits is a risk; Having said that $TSLA makes significant money from the monetization;

Challenging 2024 didn’t offer any opportunity with the stock price. Will wait…

Q1 is okay, and Q2 guidance is bit weak. Lumber demand is weak (Due to residential construction and commercial construction), prices are weak. Tariffs to have some impact. Unless the demand for Lumber improves, this stock is not going anywhere in hurry for sometime.

For now, I have Oct $22 puts sold. If they are assigned I will take.

On May 8th company announced, a new $1 B buyback program, since the earlier program was completed. Looks like they have done some repurchase under the new program.

But for $1 B buyback outstanding shares have not gone down as one might expect. But it puts a bid under the stock.

Not really. Due to British columbia pine beetle infestation already Canadian timber coming into US is limited. But the timber mills in north are dependent on the canadian Timber and they will be impacted.

Specifically for $WY, they have 14 million acres licensed in Canada. Compare that to 10.4 million acre they they own in US. Now, they have mills in Montana that rely on Canadian timber. Because, timber is heavy and the transportation cost is a major drag on profitability, companies locate their mills closer to the timber forests. So, the prices in US/ US South are not going to be influenced much.

The biggest challenge for the Timber REIT’s now are housing industry weakness. Housing starts are weak due to economic uncertainty, high mortgage rates.

Longterm, the household formations, demographic, US housing stock age (they are really old), all are significant tailwind.

Tariffs may end up making countries buy more US agricultural and wood products. I know that is not the goal of tariff, but unintended consequences and compromise..

I think Wehyerhauser is mostly douglas fir. Yellow pine tree farms are popular in the south. Closer to customers. Georgia Pacific used to be a leader. Who has mills in the south now?

I was surprised to find tree farms on the east shore of Maryland.

They tell us tree farming was a popular investment some time ago. They expected to be marketable at abt 30 years. But demand has disappointed.

The timber industry of the northern states for a century was mostly white pine. We don’t hear much about white pine tree farms. Weather makes yellow pine in the south more productive.

Missouri is well known for its hardwoods. Especially oak for whiskey barrels. Barrel staves is big business some places.

White pine is what covered the northern states when colonists arrived. The British were impressed with American forests as Britain had a wood shortage from the use of charcoal to process iron. The poor could not afford firewood and were cold and hungry.

White pine was the timber in New York, Pennsylvania, Michigan, and Wisconsin. The industry began in the east and slowly moved west as old growth trees were cut. Initially logs were floated down river to saw mills. As they got west railroads became a factor. I think WY was founded in Wisconsin and moved to the Pacific Northwest.

Railroads brought lumber to plains states which had few trees.

Weyerhaeuser Company began more than 100 years ago with 900,000 acres of timberland, three employees and a small office in Tacoma, Washington. Founded in 1900 by Frederick Weyerhaeuser, we’ve grown to become one of the largest sustainable forest products companies in the world.

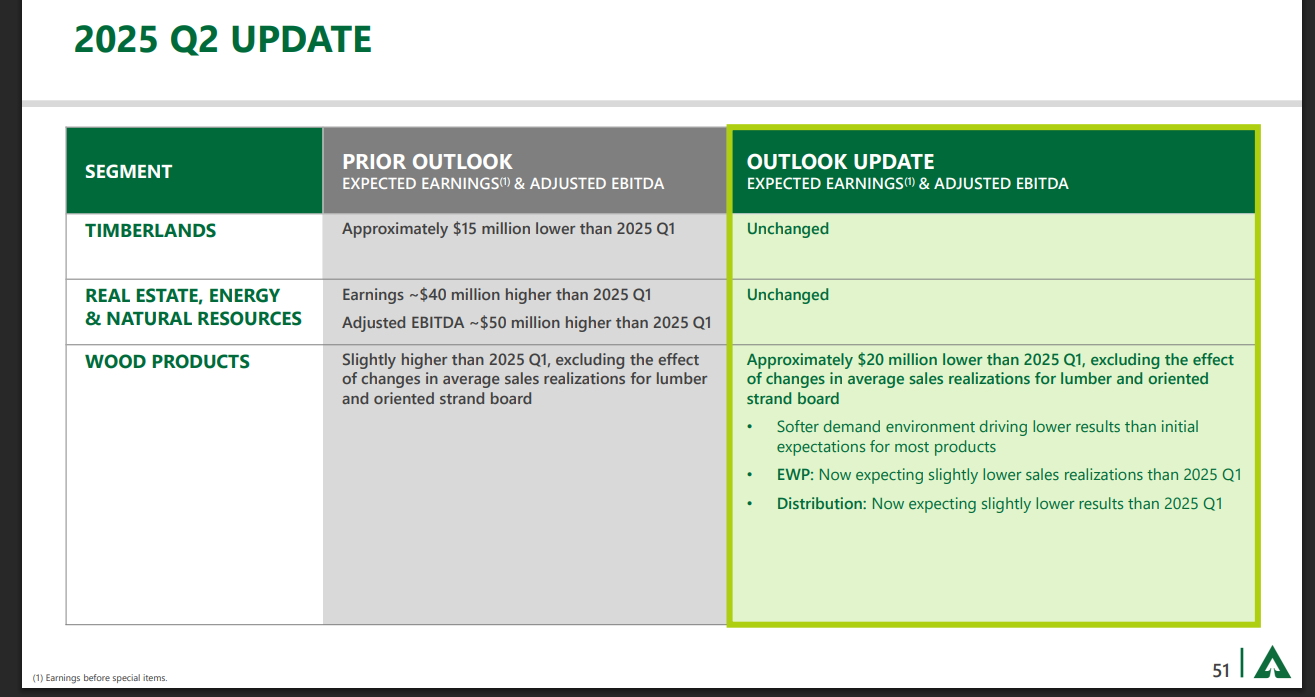

Today, $WY released June Investor presentation, in that they reset the expectation for the Q2 guidance.. based on these slides looks like $60~$75 M hit to the EBITDA. While I closed half of my puts I sold in April, still I have 50 contracts for Oct $22 puts. If possible I would like to roll it down to $20.

Primarily what happened is, most plantations have planted tensely, i.e., too many trees are planted too closely, with an expectation they will be thinned, i.e., they will cut trees that are short, that are crooked, i.e., not straight, and allow the healthy specimen to grow. Now, there was a demand for those thinned trees from paper and pulp industry.

However, in the last decade, steady closure of paper mills and the demand for pulp falling, the price for pulpwood dropped. Depending on the location, Your plantation location viz-a-viz to mills impact the price, the price fell 30% to 60%. As the price were falling, many plantation owners balked at thinning and basically allowed their plantation value to be destroyed, i.e., sub-optimal plants taking space from good stocks.

This is one of the main drivers behind,

The excess capacity build up is a common theme across the REIT industry.

In timber country they speak of chippers and pealers. Pealers become plywood, etc. Chippers mostly become paper pulp. Saw logs must be important but seem not to get lots of attention.

The decline in newspapers and magazines must mean slowing demand for that segment. In the early days of computers they said computers used lots of high grade papers. But with so many electronic displays requirements are probably not growing.

Building trades must be the growth market. And that might affect species planted and spacing.

In the last few days lumber future prices are crashing from $695 to $608, in mere 10 days. Still, $WY price moved up today! I am thinking of closing all my Oct $22 Put. Separately, Homebuilders are rallying… hmmm