The stock is up 80% ytd. That’s a good thing, yes, but it means a lot of the upside has probably been captured, unless you think it was just stupidly undervalued coming into the year. I actually do think it was undervalued, but now not so much.

Bear

PS – Hopefully this goes without saying, but for those with high confidence in NU, I’d love to hear their thoughts about all this. @SaulR80683 – you questioned why anyone would not own NU. Usually when a company is growing double digits sequentially each quarter and slows to 4%, that troubles you. What are your thoughts here?

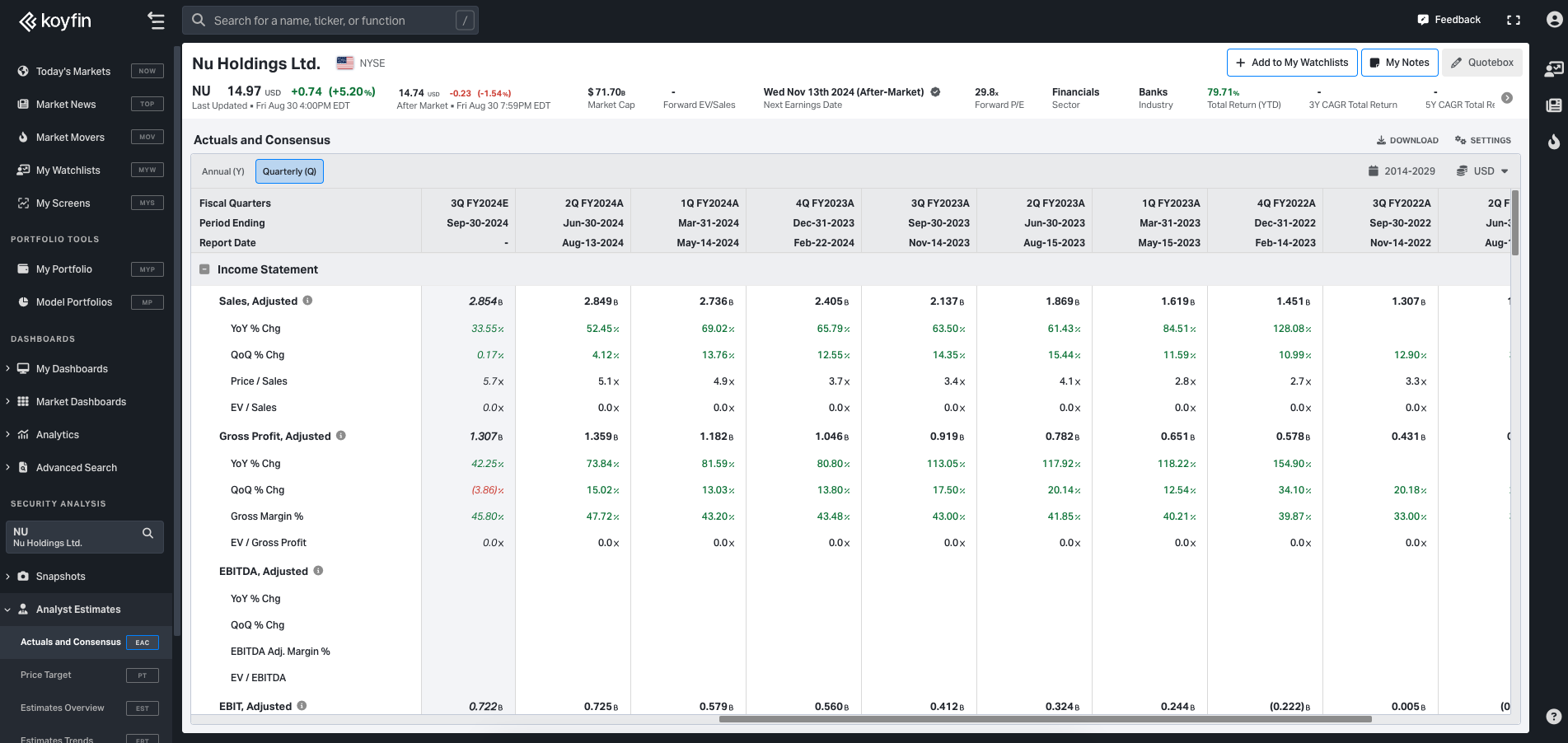

I’m trying to understand why the sources I check for numbers (Koyfin and FinChat) which are typically accurate show these revenue numbers for the last four quarters,

972M → 1207M → 1275M → 1463M

But then when I check official NU earnings releases I see way different revenue numbers, or going from 2738M → 2848M which is the 4% sequential increase. Is wrong data reaching these data providers somehow?

On the currency topic I’m guessing the bull counter point is something I learned recently from the Fort Knox interview. The CEO said “almost everything has gone wrong in macro” from GDP contraction to a presidential impeachment, an attempted coup, and high interest rates. Looks like the interest rate in Brazil is around 10% currently.

The other potential upside for the company also mentioned in the Fort Know interview it that even though they have 50% of the Brazilian population using NU, their market share in these categories is the following,

15% in credit cards

5% in personal loans

2% in insurance

1% in investments

They are also looking to setup a marketplace for non-financial transactions. I was curious if any board members know how this aspect of their business is coming along?

Here’s the Fort Knox interview referenced so it lives in this thread too,

There is a lot to like about Finchat but I am surprised they do not have Non-Gaap EPS as one of their KPI’s. I requested it but it doesn’t sound promising.

Currencies don’t worry me too much. Nu has overcome those issue before. Additionally, the dollar is likely to weaken as the Fed lowers interest rates.

While it’s true revenue growth has slowed recently, I think the revenue grew roughly as the users grow. BUT unbanked users are getting used to the ideas of the other Nu services, and many are starting to take on loans, which should be quite good for Nu.

Because the price went up a lot, IMO, is not a reason to sell a stock. If the business results support the price, and I think they do, then the price now might be a better value.

Best,

bulwnl

Thanks Saul! That video is a game changer for understanding why NU is a big idea. I’d previously been thinking of it as just as a well run Brazilian online bank, but when you understand how poor the competition was from legacy banks and how well NU is doing on metrics like customer satisfaction, the idea makes a lot more sense for why the company could grow significantly.

Sequential revenue growth slowed big time.

One counter point to this is that adj EPS is up 33% qoq, and beat analyst estimates by two cents which is the largest beat vs the estimate they’ve had in the past year.

I’m tending to weight EPS and profitability more than I used to since moving away from a SaaS dominated portfolio. Here’s a graph for reference,