https://www.nytimes.com/2023/06/21/business/economy/powell-inflation-federal-reserve.html

Fed Chair Sees ‘Long Way to Go’ on Inflation Fight

Jerome H. Powell, the chair of the Federal Reserve, is set to tell House lawmakers that most central bank officials expect rates to rise further.

By Jeanna Smialek, The New York Times, June 21, 2023, Updated 10:31 a.m. ET

Jerome H. Powell, the chair of the Federal Reserve, told House lawmakers that the United States remains a “long way” away from low and stable inflation even 15 months into the central bank’s campaign to cool the economy and wrestle down rapid price increases.

Mr. Powell is testifying before the House Financial Services Committee. He told lawmakers that the labor market remains very tight and that inflation — while it has come down notably from its peak last summer — is still too fast. In light of that, the Fed could raise interest rates even higher than their current level of just above 5 percent…

“Given how far we’ve come, it may make sense to move rates higher, but to do so at a more moderate pace,” Mr. Powell said in response to a lawmaker’s question, explaining that it was like moving from a highway to more local roads. “As you get closer to your destination, as you try to find that destination, you slow down even further.”… [end quote]

The futures market is very sure that the Fed will raise the fed funds rate in July by 0.25% to 5.25 - 5.50%. A small fraction think the Fed will raise a second time later in 2023. By December 2023, about 1/3 of market participants think the Fed will start to cut. By January 2024, about 2/3 of participants think the Fed will start to cut. By December 2024, almost no market participants think that the fed funds rate will be 5% or above. The market consensus (median) at the end of 2024 is 3.50 - 4.00%.

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

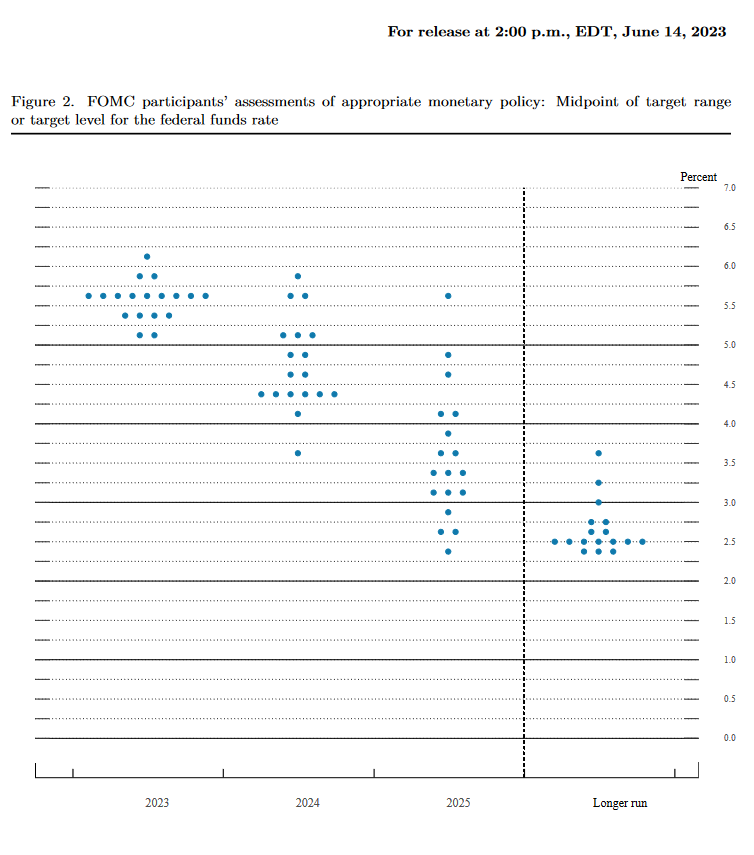

The Fed’s “dot plot” from their Summary of Economic Projections shows a higher median for 2024 but declining to this level in 2025.

The same report shows PCE and core PCE inflation declining to their target of 2% in 2025.

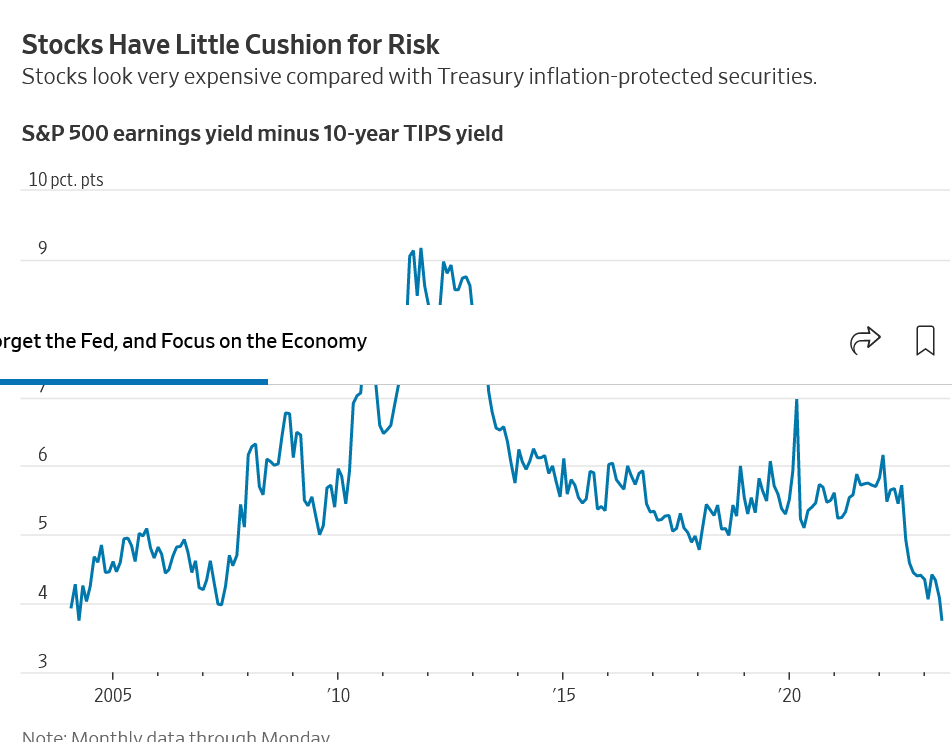

The stock market has a pattern of ignoring Powell’s clear signaling and rising until he speaks clearly again and smacks them down.

For long-term investors, what really matters is the economy.

https://www.wsj.com/articles/forget-the-fed-and-focus-on-the-economy-b56eb562?mod=markets_lead_pos3

Forget the Fed, and Focus on the Economy

What matters for long-run returns is getting the direction right, and the Fed’s fine-tuning misses the point

By James Mackintosh, The Wall Street Journal, June 21, 2023

By James Mackintosh, The Wall Street Journal, June 21, 2023

…

Rather than preparing for still-higher interest rates, markets are well along in pricing an economy with lower but fairly sticky inflation, higher-for-longer rates and continued growth. Stocks are up, Treasury yields are broadly stable at what used to count as a high level, and risk premiums on junk bonds are falling fast. These all point in the same direction, and it’s a bullish one.

Many of the same economic concerns that earlier this year led economists to predict recession are still in place… [end quote]

Conclusion: There is a lot of risk built into the stock market now. It’s very expensive. Many investors appear sure that the economy has turned around in a positive direction. But the Fed is determined to hold rates high for at least the next year. They NEVER intend to resume the zero fed funds rate that pushed so many assets to bubble levels.

Wendy