Says “may” reduce rate of rate increases in December.

Steve

Says “may” reduce rate of rate increases in December.

Steve

In the same speech, Powell made it clear that they will have to maintain higher rates for a long time.

Updated Nov. 30, 2022

…

“The labor market … shows only tentative signs of rebalancing, and wage growth remains well above levels that would be consistent with 2% inflation,” Mr. Powell said. “Despite some promising developments, we have a long way to go in restoring price stability.”…

Mr. Powell repeated his earlier view that officials were likely to raise rates to a somewhat higher level early next year than they had anticipated in projections released after their September meeting, when most officials saw their benchmark rate rising to between 4.5% and 5%.

“There is no doubt that we have made substantial progress,” he said. “We have more ground to cover.”… [end quote]

Here is Chair Powell’s speech.

November 30, 2022

by Chair Jerome H. Powell

…

For purposes of this discussion, I will focus my comments on core PCE inflation, which omits the food and energy inflation components, which have been lower recently but are quite volatile. Our inflation goal is for total inflation, of course, as food and energy prices matter a great deal for household budgets. But core inflation often gives a more accurate indicator of where overall inflation is headed. Twelve-month core PCE inflation stands at 5.0 percent in our October estimate, approximately where it stood last December when policy tightening was in its early stages. Over 2022, core inflation rose a few tenths above 5 percent and fell a few tenths below, but it mainly moved sideways. So when will inflation come down?..

For now, let’s put aside the forecasts and look instead to the macroeconomic conditions we think we need to see to bring inflation down to 2 percent over time.

For starters, we need to raise interest rates to a level that is sufficiently restrictive to return inflation to 2 percent. …

Finally, we come to core services other than housing. This spending category covers a wide range of services from health care and education to haircuts and hospitality. This is the largest of our three categories, constituting more than half of the core PCE index. Thus, this may be the most important category for understanding the future evolution of core inflation. Because wages make up the largest cost in delivering these services, the labor market holds the key to understanding inflation in this category.

In the labor market, demand for workers far exceeds the supply of available workers, and nominal wages have been growing at a pace well above what would be consistent with 2 percent inflation over time.3 Thus, another condition we are looking for is the restoration of balance between supply and demand in the labor market…

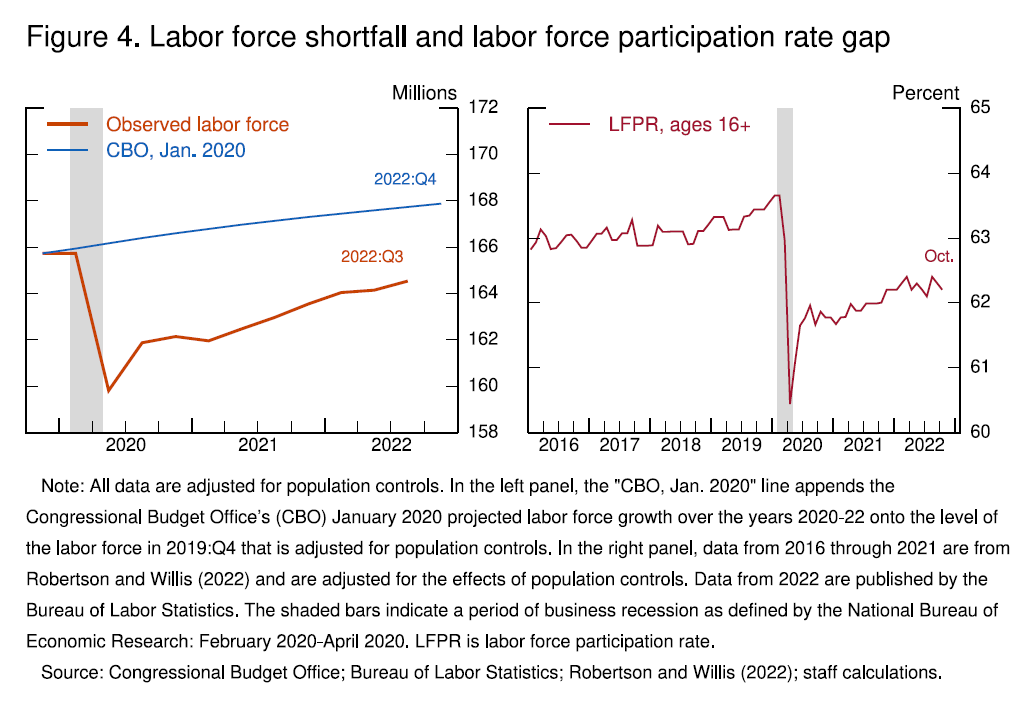

Comparing the current labor force with the Congressional Budget Office’s pre-pandemic forecast of labor force growth reveals a current labor force shortfall of roughly 3-1/2 million people (figure 4, left panel).4 This shortfall reflects both lower-than-expected population growth and a lower labor force participation rate (figure 4, right panel). [Lots of retirees, fewer immigrants.]

These excess retirements might now account for more than 2 million of the 3‑1/2 million shortfall in the labor force…The combination of a plunge in net immigration and a surge in deaths during the pandemic probably accounts for about 1-1/2 million missing workers.

Policies to support labor supply are not the domain of the Fed: Our tools work principally on demand…

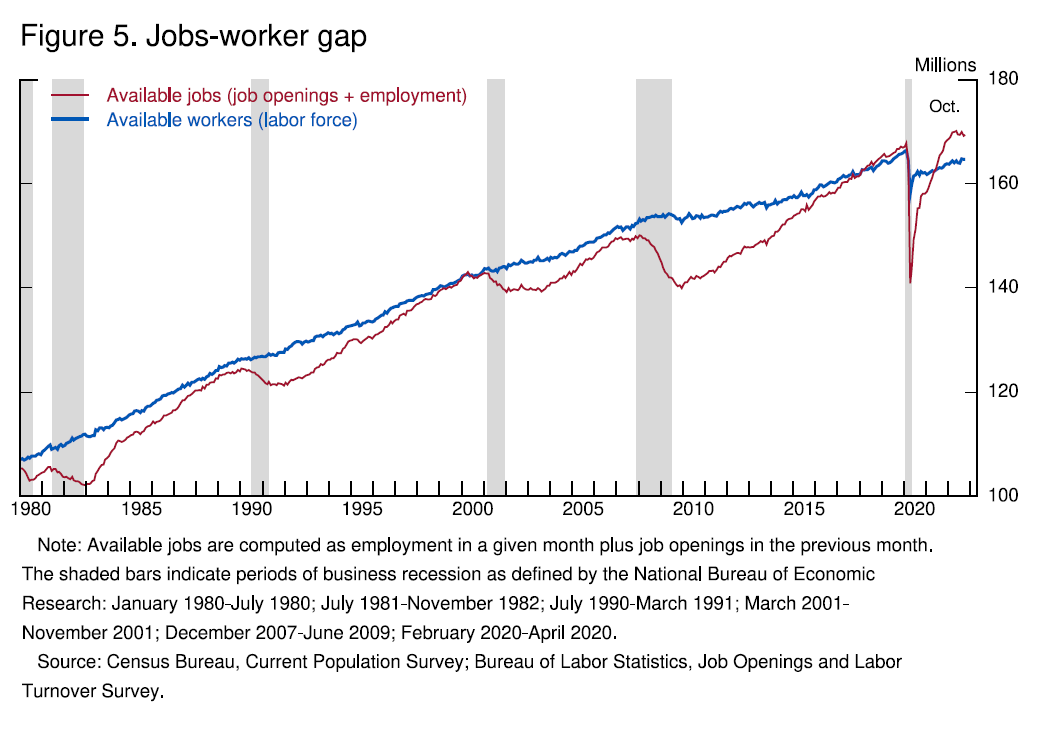

Currently, the unemployment rate is at 3.7 percent, near 50-year lows, and job openings exceed available workers by about 4 million — that is about 1.7 job openings for every person looking for work (figure 5). So far, we have seen only tentative signs of moderation of labor demand…

Given our progress in tightening policy, the timing of that moderation [in the pace of increasing the fed funds rate] is far less significant than the questions of how much further we will need to raise rates to control inflation, and the length of time it will be necessary to hold policy at a restrictive level. It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy. We will stay the course until the job is done. [end quote]

The Fed is in the position of having the responsibility for controlling inflation which was caused by factors outside its control (fiscal policy, pandemic, war, retirements, immigration) using a single tool (the fed funds rate) which doesn’t directly impact any of the causes.

The market is jumping up and down with glee at the slowing of the Fed’s increases. But they aren’t listening to Powell. Just as they didn’t before.

Slower does not mean lower. The Fed will continue to raise rates until inflation subsides. Because the rate hikes don’t directly affect the causes of inflation the Fed can only lower inflation by causing a recession that reduces the demand for labor. This will take a while, maybe a year or more.

The market doesn’t understand this. Speculators are speculating that the Fed will cave in and lower the fed funds rate at the slightest whiff of recession as they have done before.

But Powell is clear: he expects the recession, he predicts pain and he will continue until the job is done.

Wendy

Mr Market doesn’t seem to care about cautionary statements about the future. The “lower rate of rate increases” narrative has been floating the market for nearly two months.

Steve

“Everyone” knows that that is a BS statement. They will raise rates some more, probably 0.5 in Dec, and a few 0.25s in early 2023. Then they will stand pat … until they panic when a recession occurs. Once we are deep enough in recession, they will panic and start dropping rates much earlier than they expected. It would even be in late 2023 rather than in the second half of 2024.

That said, I now feel that there is a decent chance of avoiding a recession. Powells moderating statements only added to that feeling. The fact that the fed isn’t going to go hog wild and rapidly bring rates all the way up to the inflation rate … which almost always causes an overshoot … is comforting to many.

Take that in tandem with the IRA. While the IRA raises taxes it subsidizes industry and infrastructure on balance. Higher taxes yet would have allowed higher wage gains.

That will be much later in the cycle.

The IRA comes into effect.

Yes, that is what “everyone” expects, just as you said.

But…what if Powell and the Fed hold strong and actually do what they say they will do?

I agree with you that Powell’s moderating statements point to a gradual approach to a fed funds rate that will control inflation which is less likely to cause a recession.

But he also said that the higher rate will be needed for a long time. I don’t think the market believes that.

Wendy

It’s easy to see what the market believes at any given time. That’s because there is LITERALLY a market for fed fund futures. People putting down REAL money trading on the probabilities of what the fed funds rate will be. Some people doing that trading are doing so to hedge other instruments directly dependent on interest rates, and others are simply speculating.

If you look at the fed fund rate futures, you will see that the “terminal” rate is likely to be 4.75-5.00 after the 1-Feb-23 Fed meeting, Same for the 22-Mar-23 Fed meeting. Same for the 3-May-23 Fed meeting. Same for the 14-Jun-23 Fed meeting. Same for 26-Jul-23 Fed meeting. Same for 20-Sep-23 Fed meeting. THEN the likelihood after the 1-Nov-23 Fed meeting drops to 4.50-4.75, and same for 13-Dec-23 Fed meeting.

Here’s a probability chart (directly from the CME based on todays closing numbers).

@MarkR, thanks for sharing. Please post a link because I would like to follow this.

Wendy

@WendyBG - I’m not MarkR, nor do I play him on TV, but I found the link that you are looking for and can spare Mark the trouble. Click on the link, then on the left side of the graph tool choose, “Probabilities”. That gets you the exact chart that Mark posted.

Hope that helps!

'38Packard

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

@38Packard thank you! How do I get it to show a table that looks like the one @MarkR posted? I tried but failed.

Wendy

I had closed the tab and then had to search for it again (browser history didn’t help much because there were hundreds of links at that site until I found it).

Here is the link to that chart - FedWatch - CME Group

(need to click on “probabilities” inside the chart area to see it)

{kind=link}

{kind=link}