Buffett continues to move the goalposts. The amount of cash he is holding is unacceptable unless there are near term plans to use it.

At the 2017 annual meeting, Buffett said, “But like I say, at a point, the burden of proof really shifts to us, big-time. And there’s no way I can come back here three years from now and tell you that we hold 150 billion or so in cash or more, and we think we’re doing something brilliant by doing it.”

After adjusting for inflation, $150 billion in May 2020 would be worth $183.4 billion today. Time for you to sell?

Exactly. Buffett said it’s not brilliant for them to hold so much cash so why are they doing it? Also, he had an opportunity to deploy massive sums during the pandemic and chose not to, similar to the financial crisis when he mostly did convertibles.

The deals were not nearly as good for Berkshire during the pandemic compared to during the GFC. In the GFC, getting $5B from Berkshire (in return for interest and warrants) was also a big show of confidence meant to keep your business afloat until government did what they needed to to stabilize the economy (mostly commercial lending and mortgages). But during the pandemic, government almost immediately released trillions of dollars into the economy. Essentially for free! So there wasn’t much profit to be had for Berkshire in that instance of economic dislocation.

Obviously, if it is unacceptable to you, you can sell your Berkshire shares. Right now I suspect that Buffett is waiting for a really good deal to show up. Maybe when the depths of the CRE crisis hits in 2026/27, if Berkshire is convinced that offices will still remain a thing, then there may be some very sweet deals to be had?

They are earning decent returns on that.

This was discussed ad nauseam. Berkshire and WEB mindset is to protect capital first and foremost. I think they are doing an excellent job of it. As an investor you have an option of whether to invest in Berkshire or not.

I still hope, he may end up investing/ creating long-term position but they are not going to do a deal for the sake of doing it.

We are holding 18% cash equivalents on assets of $1T in a highly priced market & we are making over 5% on our T bills. For good reason, I trust the G.O.A.T. Owner Patience has been rewarded quite handsomely over the last 60 years. I think Warren senses some real opportunity may arise over the next 1-3 years. Nice to know he will be disciplined and we will swing hard when the time is right.

This is not true. Warren took smart calculated risks when he was younger. Walking into Geico’s office on a Saturday is a good example.

He has been progressively becoming risk averse as the size has grown. At the bottom of the pandemic, Warren was selling.

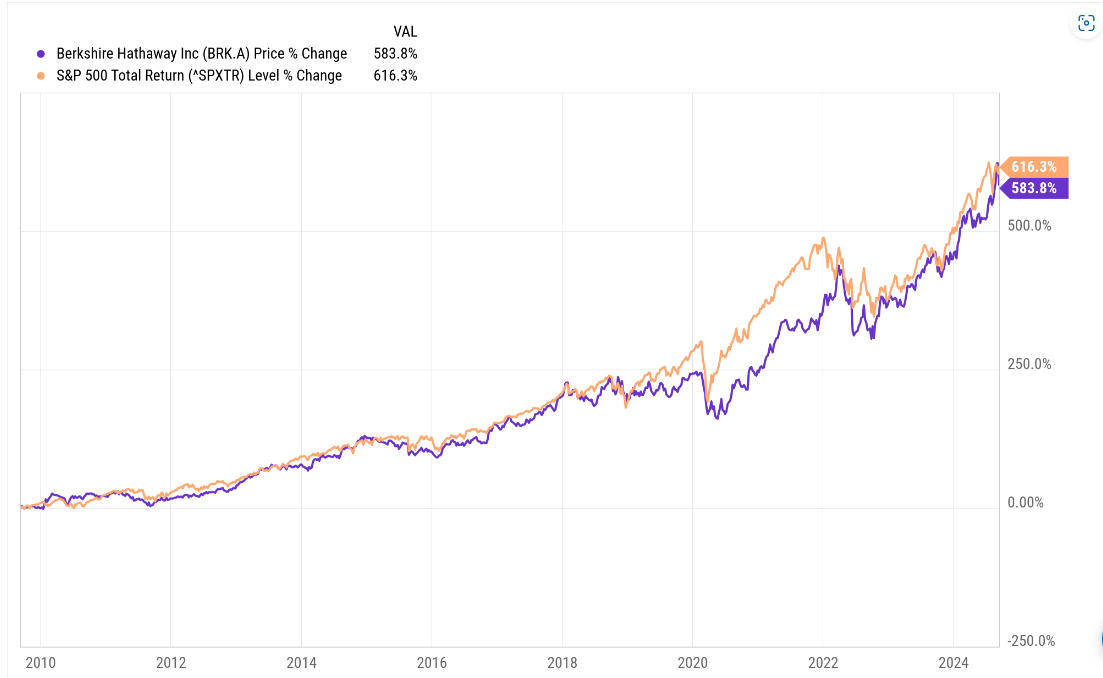

This shows up in the results in BRK’s underperformance over last 15 years.

As an investor it is wise to slowly sell BRK and DCF into S&P index. There is no way Greg will be able will be able to do better than Warren and Warren is underperforming.

Sorry, but it is true.

Barron’s yesterday : “Berkshire has topped the S&P 500 over the past one, five, 10, and 20 years.”

Divi in May 2024: As an investor it is wise to slowly sell BRK and DCF into S&P index.

Ah, but not over 15 years - Divi’s preferred measure ![]()

25 years - when I first bought BRK - is quite satisfactory!

No, I win, having sold some BRK at the top and sold a good part of my puts 2 days ago - - - and several ones on the Berkshire forum over at shrewdm.com won who did the same, Jim and others.

That’s the beauty of BRK: Predictability!

P. S. : Does S&P wins over 1, 5, 10, 15 and 20 years?

Welcome to the club. Looks like you, Ajit and I are in same company. Sell sell sell.

There is no way Abel is going to outperform S&P over next 15 years when Warren couldn’t with a much smaller market cap.

“in the Club”?

With me having sold 5% of my “forever” Berkshire shares?

Btw, regarding your “sell sell sell”. Famously James Cramer said exactly those 3 words (“Regarding Berkshire Hathaway there is only one thing to do: Sell sell sell”) on the very day of it’s low in Jan or Feb 2000.

There never was a more precisely wrong timed call, as from that very day on the Internet stocks did crash and Berkshire did rise again to infinity and beyond.

As Cramer for me always was a contra indicator after hearing him saying that I bought my first Berkshire shares on that day, a day Cramer and me will never forget.