This is a name I sold some puts last year, that expired, but failed to buy the stock in spite of coming close few times. Any case, the stock is declining for some time and after earnings, it is down 5% today. Interestingly, post earning $70 put premium have declined, that is, from $1.8 it moved to $1.4. I think the primary reason is the company guidance for 2025, which is $3.67 to $3.78, which is slightly higher than this year 2% ~ 5%. If the stock declines further, I am looking at doing some covered call.

That is plain ugly. It’s living under the 200 day and could go much further down. If it breaks $82 to $83 than the next stop is around $70.

From your lips to God’s ears. ![]()

1 Like

Thanks, I needed that. ![]()

Just to keep tracking I have sold couple of $70~$80 Jan 26 call spreads for $7.75; If the stock stays above $80, I get 30% annualized yield. I am fully prepared to take the shares and add more if the price declines.

1 Like

- The company is a steady grower; Their target is 3~5%, FX has impact

- The company now pays $2 per year dividend

- The debt remained more or less flat for the last 5 years

- Most of FCF after paying dividend is used to buyback shares, not much over the last 10 years it is 7m ~ 10m;

2025 Guidance

- Company generally guides conservative

- Flat Sales growth

- Gross margin to be up slightly

- GAAP EPS up low to mid single digit

- Some analysts think $CL might cut ad to leverage the EPS; $CL in CAGNY presentation talked about, how they have invested increasing $$$'s in the last 7 years; The 2018 starting point is for a reason, i.e., that’s when $CL had organic growth reset! So they have made investments in the last 7 years to support the brand.

The entry price matters lot on these names; I expect some weakness in 2H and If the stock declines, around $70 will be a medium term buy; For now, I have couple of $70 to $80 call spreads, just to keep an eye;

Translation: they have pricing power. Their markets are clearly mature. Sales expected to grow with population, 2% per year. Organic growth is mostly price increases. They have done international for growth for decades. Otherwise growth requires inventing a new category. Stealing market share from the competition is difficult.

Today the company announced 1Q, where it beat the estimates. The company updated the full year guidance, and expecting slightly lower sales, and EPS towards the lower end. The stock is holding very well, while it is up from the time of my original post, the call spread has actually widened a bit, ![]() , thanks to volatility.

, thanks to volatility.

In any case, I am not doing anything, just sitting tight and watching.

1 Like

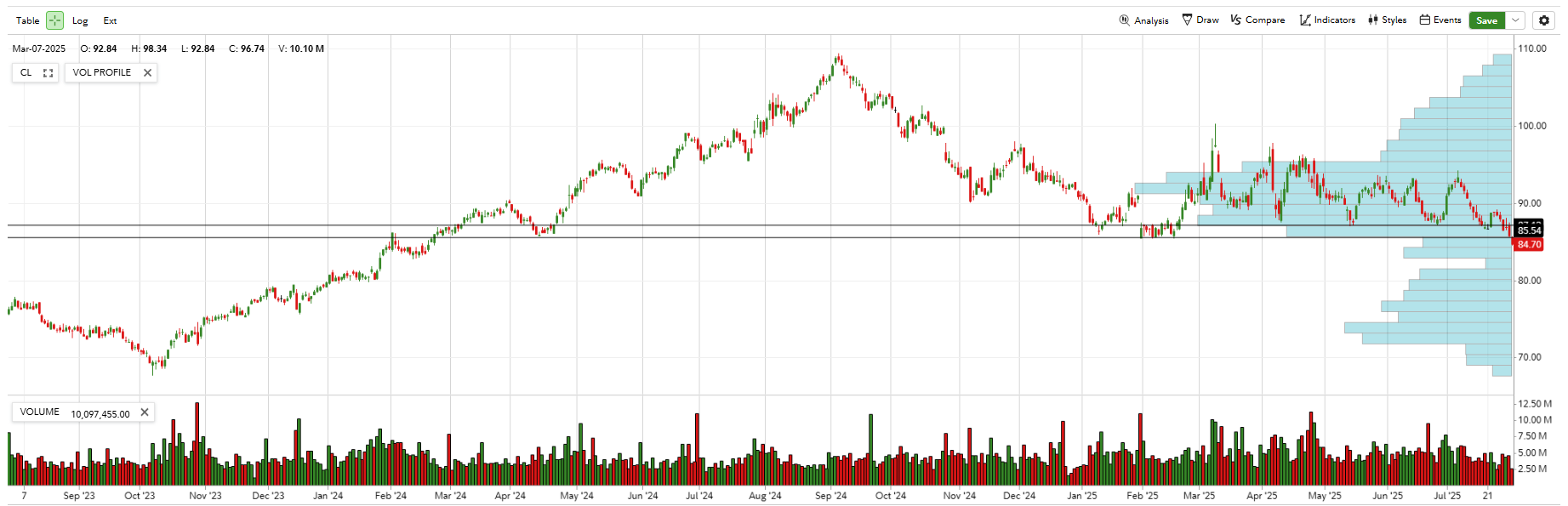

The stock is slightly below both support levels. Tomorrow is the earnings. If it is not recovering, then it has a long way to go down.

I don’t think anyone considers Colgate a growth stock. Most of its markets are mature. Exports are its best growth opportunity (and has been for years, maybe decades). May be subject to trade issues and tariffs. Strictly a cyclical. Able to raise prices? Able to compete with generics? Might benefit from a stronger economy due to tax cuts but inflation and consumers trimming spending have to be a worry.

This is an area where being able to create a new consumer category can be a winner. (Soft soap is the most recent example. Ragu spaghetti sauce in a jar.) Do they have any successes in that area? Otherwise its raise prices or dog eat dog for market share.

The stock price is declining steadily. Here are next 3 supports and especially $79.x is relatively strong support. I am watching closely, and it is time to do a deep dive to get comfortable, as the stock is marching towards $70 ![]()

PS: Just like $C had a steady climb, $CL is steadily declining. Playing these trends are more profitable for investors. I have not really bought a put or put spread, still learning about how to trade these trends… someday ![]()

![]()

Are short sellers doing well? Will the down trend continue?

Tariff impact doubtful. Will international business be impacted? Minimal impact on imported raw materials expected.

Will falling interest rates help? Low end consumers cutting back switching to generics might explain slowing profits. What is lag time for impact of lower interest rates?

In name like this typically short interest is very low, like 1.5%.

$CL has pricing power and can generally navigate interest rate and raw material price hike, or even slightly higher Ad spend, people switching to lower product during recession etc.

The biggest challenge is waiting for the stock to bottom and buying at right price, and then wait for the cycle to turn.

Patience, grasshopper patience.

Colgate-Palmolive has always struck me as a defensive play with steady cash flow, but limited explosive growth. Their global footprint and strong brands give stability, especially in downturns, yet the upside feels capped compared to higher-growth consumer staples. I tend to think of CL as more of a dividend and safety stock than a long-term compounding growth engine.

1 Like

Q3 results were out, looks like this quarter will mark the bottom in sales growth. In a name like this, the changes are from LSD (low single digit) to MSD (medium single digit) OSG (Organic Sales Growth) is a great growth.

The entry price is very important for a low growth stock, even if the brand is great. I am seeing there are many such companies in this segment with solid brand power, steady sales, decent dividend and regular share repurchases.

I am revisiting my original thesis on growth, and the valuation model.

Analysis, paralysis. I missed the opportunity to buy. Don’t be too piggish to get the best entry price.

Define “higher growth consumer staples.” Like Proctor & Gamble, Church & Dwight, Henkel in Germany, these are defensive stocks as long as they have strong brands (that can resist generic substitution).

Growth usually requires inventing a new category. The most recent one is liquid hand soap.

People say cosmetics is a better business. Fads like “aloe” go through the business causing reformulation and relabeling. Easier to raise prices to those who want to try the latest fad—which is heavily advertised.

Banning synthetic dyes and food colors might be the latest fad. How do you invest?

1 Like