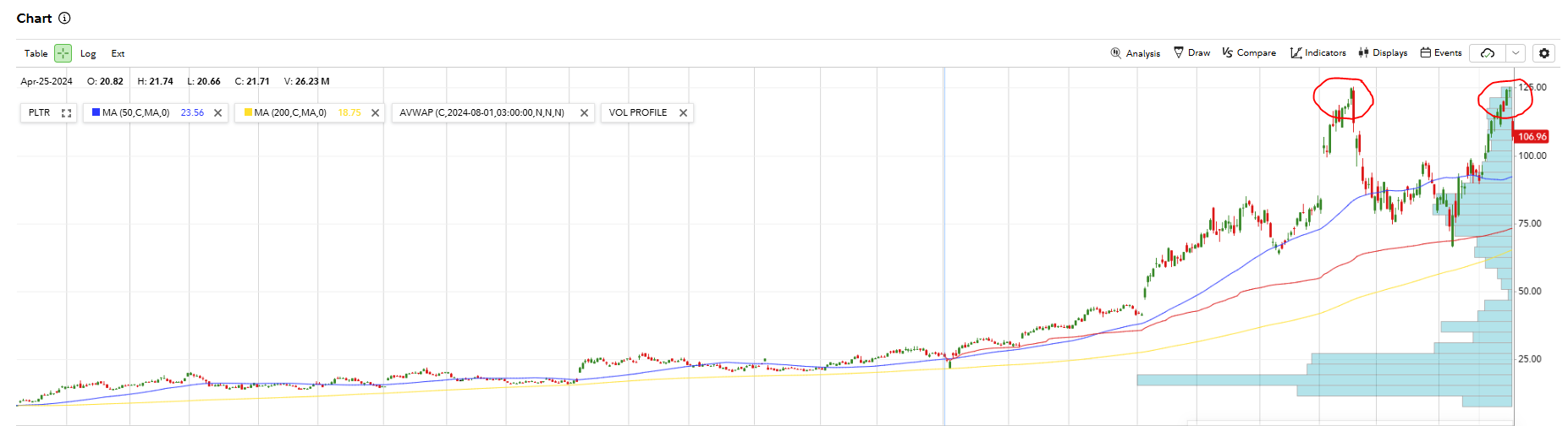

Current market cap is $155 B, that is 30 x revenue for 2027, that is another 3 year away. However, earlier the stock was hot and shorting it is burning money. Now the stock seems to be have broken and breached the 50 day moving average. The stock has potential to “fill the gap” or visit $50.

I have modeled 25% growth over next 7 years and termina 30% net profit, that will result in $3.8 B net income and modeling 5% dilution (currently it is 6.8%), you are getting $1.2 EPS, that is on year 2031. I am not arguing it will not trade with high multiples, but lot is baked into the price.

I am thinking of either a call spread, or put spread with some defined risk and at least 3x payout expiring Feb 7th, 3rd is earnings.

I have factored those things. There are lot of hype around 20m project wins… They are not going to get Lockheed Martin kind of $100’s of billions contracts.

In any case, my spread have defined risks and generally these bets are for $1 K or $2K. That is like .2% of my trading account.

Mr. Market will give PLTR high valuations expecting that price will grow into valuations. There are $Trillions sitting on the sidelines and will go to high growth companies as fed cuts.

The danger is that you may be right in your thesis but still lose on the trade. I am in a similar situation with RKLB.

I guess you haven’t really read my post I am going to place either call spread or put spread, both defines risk and it is going to be around .2% of my trading capital.

Separately, in a silicon valley 3 or 5 young kids working in a garage coming up with a product that can achieve 10x functionality improvement or 10 x cost reduction is feasible. For a company that is serving enterprise customers for 20 years, is not going to achieve that kind of velocity. There is one $NVDA. Folks imagining that $PLTR revenue is going to go 10x in 2 to 3 years and valuing company like that are going to be disappointed. Today the company is valued over 55x of revenue not earnings. What kind of growth is embedded in that?

Again, The stock had a huge run and it is breaking and I am going to place a defined risk, short-duration, just post earnings spread trade.

Never is the time to go short. Shorting has a terrible risk profile, limited upside, unlimited downside. Options are a better, safer alternative. In addition to spreads, covered calls can work as well or better which is what I’m doing.

The first thing to determine is whether Palantir is a company with a future. If not, sell.

If the stock keeps falling one can get cash from selling calls that expire worthless effectively reducing the stock’s cost basis. The option’s delta says that you cannot get enough cash to match the stock’s fall but it sure mitigates the volatility. The strike price needs to be high enough not to sell at too much of a loss. That is the limiting factor

The Captain

PS: So far two call trades have reduced my PLTR cost basis by 10.8%. If the latest calls are assigned I make net 9.3% in under two months.

I think $NVDA and AI Capex is going to go through digestion phase, whether it is this quarter or next or one after that… we don’t know, but at some point $NVDA revenue growth, earnings growth is going to normalize and suddenly folks are going to be unhappy with that.

My position is 20% covered call Feb-7, 30% on Feb-21, 30% Mar, 20% May. All positions are with $100 Strike. I am perfectly fine if they get called away, and it gives me some flexibility in planning. AI is a great long-term story, but the ROI story has some questions need to be answered.

Also, I expect the application layer is going to make more money in the end.

Yahoo Finance is showing a PE for Palantire of 418.7. Stock price is going up much faster than earnings. Very speculative.

Nvidia PE is shown as 46 but when adjusted for earnings growth closer to 30. That is reasonable for a growth stock. The risk is whether earnings growth will continue given the recent developments with Deepsearch. We shall see. I think shorting from here is more risky.

Not earnings, but revenue… They are projecting $3.75 2025 revenue. In the after hours the market cap moved up $44 B!!!

I know the results will beat expectation and stock could move up is a possibility, but this was beyond my expectation! I will give it couple of weeks to see where the stock settles and then need to decide whether to hedge and accept the loss and move on.

Decreasing Returns

Traditional businesses like manufacturing and services that have high capital needs

Increasing Returns

Software like businesses where the first copy is very expensive but copies are dirt cheap

The profit to revenue ratio is very different. With Decreasing Returns the ratio tends to be linear while with Increasing Returns it’s exponential because the cost of copies is minimal. This is the reason why traditional valuation methods don’t work well with Increasing Returns type businesses.

You can apply traditional valuation methods, just require some minor adjustments. For Ex: I assume they will grow their earnings, 35%, then 30%, then 25% and then 20% as terminal growth (these are pretty high numbers) for a period of 7 years and then at the 7th year revenue assume you can get 30% margin (again it is high even for SW firms) and apply 20~25 PE on that number, now you can assume some dilution 3% to 5%, look at the past dilution as a guide, once you have the share price at 7 years then you can apply what kind of returns you need and discount it back, you can get current share price.

Also, much simpler metrics like x of revenue, can be applied. Adjust x for growth, and margins. Currently $PLTR in certain metric is off the charts. There is a strong retail community, which keeps buying every dip. So the valuation will be higher for some time. I am not expecting the company to have a couple of bad quarters of revenue at least for another year or two, so until that happens the valuation may stay higher.

So, you cannot stay short of this name longer. You just trade based on technicals. Be quick to take profit or loss.