Last week, Fed Chair Jerome Powell spoke at the economic symposium sponsored by the Federal Reserve Bank of Kansas City in Jackson Hole, Wyoming.

Speech, August 23, 2024

Review and Outlook by Chair Jerome H. Powell

…

Today, I will begin by addressing the current economic situation and the path ahead for monetary policy. I will then turn to a discussion of economic events since the pandemic arrived, exploring why inflation rose to levels not seen in a generation, and why it has fallen so much while unemployment has remained low.

Near-Term Outlook for Policy

Let’s begin with the current situation and the near-term outlook for policy…

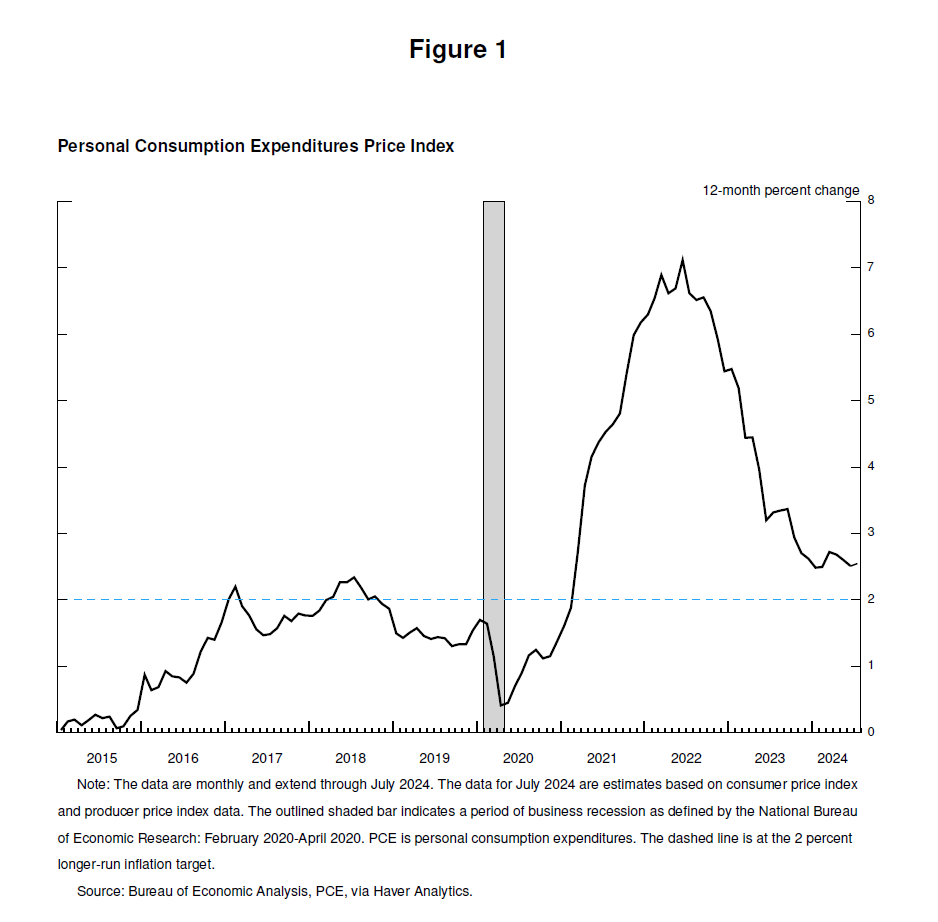

Our restrictive monetary policy helped restore balance between aggregate supply and demand, easing inflationary pressures and ensuring that inflation expectations remained well anchored. Inflation is now much closer to our objective, with prices having risen 2.5 percent over the past 12 months (figure 1).2 After a pause earlier this year, progress toward our 2 percent objective has resumed. My confidence has grown that inflation is on a sustainable path back to 2 percent…

{kind=link}

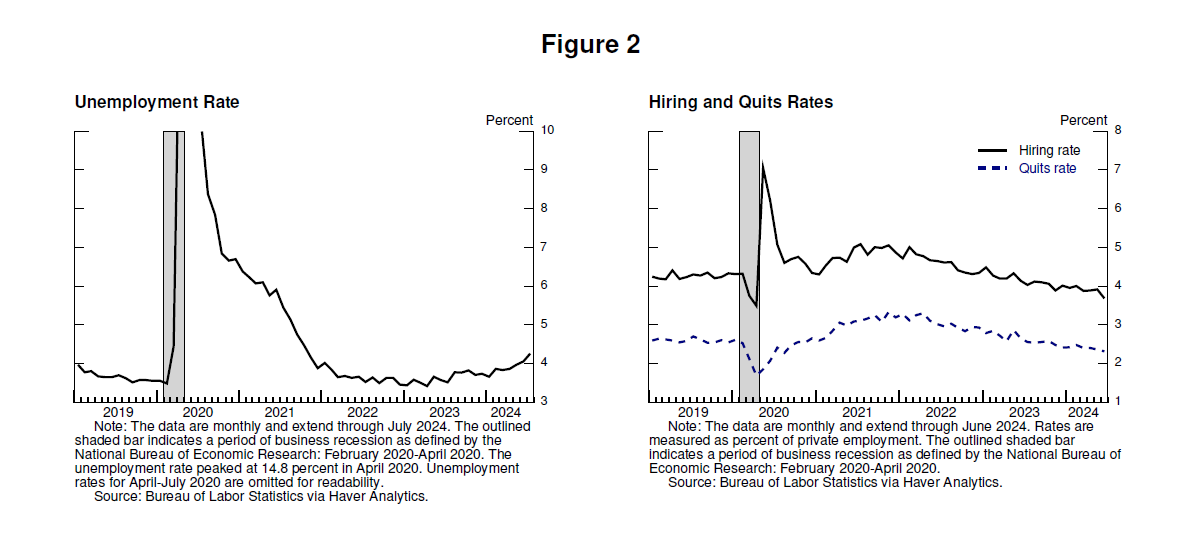

Today, the labor market has cooled considerably from its formerly overheated state. The unemployment rate began to rise over a year ago and is now at 4.3 percent—still low by historical standards, but almost a full percentage point above its level in early 2023 (figure 2). Most of that increase has come over the past six months. So far, rising unemployment has not been the result of elevated layoffs, as is typically the case in an economic downturn. Rather, the increase mainly reflects a substantial increase in the supply of workers and a slowdown from the previously frantic pace of hiring. Even so, the cooling in labor market conditions is unmistakable…

{kind=link}

The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks… [end quote]

The entire speech is soothing since it repeats what market analysts and the options markets have been saying for months.

CME options traders give 100% probability of the Fed cutting the fed funds rate at their September meeting in 2 weeks, with 2/3 betting on a 25 bps cut and 1/3 on a 50 bps cut.

The entire Treasury yield curve continues to fall. The slope is now positive from 5 to 20 years. Junk bond yields are falling faster than Treasury yields and the spreads are falling. This may indicate that investors recognize that falling interest rates will take some of the pressure off zombie companies that may need to refinance low-interest loans at higher rates.

SPX and NASDAQ indexes have stabilized. VIX is low. The Fear & Greed Index is in Greed. USD is near the bottom of its channel. Gold appears to have stabilized after its strong recent run-up. Oil and natgas have also stabilized. CAPE is increasing to a new bubble high.

The trade is neutral since SPX is not increasing faster than UST (the price of the 10 year Treasury).

The Atlanta Fed’s GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2024 was 2.5 percent on August 30, up from 2.0 percent on August 26. This is a good, sustainable growth rate and far from recession.

The overall picture is an end-of-summer pause.

It’s clear that the Fed is moving from a tightening cycle to a loosening cycle. In previous cycles, the Fed’s phase shift was due to incipient recession so the loosening was followed by a stock market drop.

That may not be the case this time. If the soft landing scenario continues as the Atlanta Fed predicts both the stock and bond markets could see continuing strength.

The METAR for next week is sunny.

Wendy