ESPR ER changed to 8/12 bmo

They have an 8/5 BTIG biotech (private?) event now.

Why the delay? Just bc of btig conf, or need more time for something?

What are you allowed to say at a conf a week before an ER anyway?

Dreamer

ESPR ER changed to 8/12 bmo

They have an 8/5 BTIG biotech (private?) event now.

Why the delay? Just bc of btig conf, or need more time for something?

What are you allowed to say at a conf a week before an ER anyway?

Dreamer

There is a company trading under NAMS that is doing similar things as ESPR.

Feels more like a hyped SPAC at moment, although their product may be legit.

Issue is these studies take time, side effects can derail success, and then you still have period of time before your “label” improves and/or insurance payers get on board, etc…

Esperion drugs were approved in 2020.

It was only March 2024 that they had improved label. Many payers got on board in June w more expected in Sept.

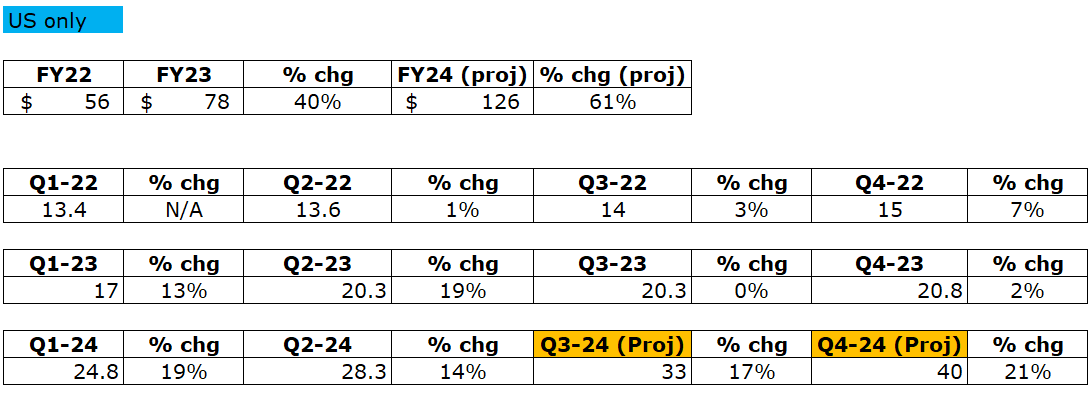

Meanwhile, Esperion on pace for $130m in US sales (my projections) this year, which is 70% y/y growth.

NAMS has no sales yet.

Best i can tell, they are looking at 2026 before any label updates. So Esperion has about a 2yr headstart.

NAMS trials are all in combo w a statin.

Esperion approved for primary care without statin.

Anyway - wanted to point out a threat. They are supposed to announce data from one of studies on Monday. May or may not lead to FUD against ESPR.

Upcoming ESPR catalysts:

Their non-US partner DSE reports, maybe next week?

They have a BTIG conf next week.

ESPR has q2 ER on 8/12.

The longer a buyout or US partnership drags out, the lower I think the upside is, unless they come out w additional indications that bemoedoic acid helps with.

So I would like to see them do something by EOY.

Would be fun to daydream about $20, $30, $40 prices, but a more realistic scenario is $7-8-9 for a stock stuck under $3. Still great, if done this year vs in 2-3 years.

Dreamer

Not time to buy, yet. Earning next week, unfortunately. That could move the needle. But the chart says $1.90 and we are $2.13 and coming off the opening lows.

We MAY be at a point where bad economic news is now bad market news.

The bad employment numbers don’t mean just a rate cut or two to spike the punchbowl, but more of an ooops, and no August meeting so on hold 'til September and a bunch of weekly jobs data before then.

I dumped most of my ANET yesterday at $356 after months and months of being too cheap to pay LT cap gains. Now sitting at $315, also rebounding from opening lows. I guess that is at 10% haircut. Maybe I can buy it back and reset the cost. It was up 550% since 2017 (average, I had a small amount of 10-bagger in there).

KC

everyone acts like rate cuts = good.

Maybe a boost after the first one, and then honeymoon ends as the other cuts rapidly file in after (because they are needed - which means economy not doing well). See; 2000, 2008, etc etc

Don’t bother pointing to 2020…nothing about pandemic and massive stimmy funds are normal part of recession cycle.

my 2 cents.

Also agree on Esperion…earnings out, and whether good results or not, expect stock could go limit up or down.

I was on vacation this week, so didn’t post much on their partner DSE earnings, but they were up 100%+ y/y for what it’s worth. Will get around to it.

Next up is some BTIG conf on 8/5 and then ER is on 8/12 (Monday).

Then some online are mentioning form 13F’s or whatever funds file should show up the 13th or 14th and you can gauge whether fund/institutions are adding or subtracting to their ESPR shares and whatever confidence that provides you.

Still would like to see $29m or thereabouts for US sales on the 8/12 ER.

Most important will be color on the current Q and the roadmap of what other payers remain to get on board with better cost coverage of the drug, which would further spike sales.

I am hoping they take a partnership or a buyout offer soon, assuming they have offers coming in to choose from. Long-term going it alone might be more prosperous in the long run, but don’t think I have the patience for that. Would be ideal to reap an ESPR windfall to leverage if/as markets crash further when it becomes evident a recession truly is at hand, as there will be bargains to buy.

Dreamer

Is this a legit take?

Dreamer

Ms. Foody and Mr. Looker

Pursuant to the terms of their employment agreements, in the event that employment is terminated by the Company without “cause” (as defined in the employment agreement), subject to execution and non-revocation of a separation agreement that includes a customary release of claims in favor of the Company, the named executive officer is entitled to receive (i) an amount equal to 12 months of then-current annual base salary, payable in 12 monthly installments, and (ii) if the named executive officer is participating in our group health plan immediately prior to termination, a monthly cash payment until the earlier of 12 months following termination or the end of the COBRA health continuation period in an amount equal to the amount that we would have made to provide health insurance to the named executive officer had the named executive officer remained employed with us. In the event that employment is terminated by the Company without “cause” (as defined in the employment agreement) or the named executive officer resigns employment for “good reason” (as defined in the employment agreement), in either case within a 12 month period following a sale event, subject to the named executive officer’s execution and non-revocation of a separation agreement that includes a customary release of claims in favor of the Company, the named executive officer is entitled to receive (i) an amount equal to their then-current annual base salary (or such base salary in effect immediately prior to the sale event, if higher), plus their target bonus, payable in a lump sum within 60 days after the date of termination, and (ii) if the named executive officer is participating in our group health plan immediately prior to their termination, a cash payment equal to the amount that we would have made to provide health insurance to the named executive officer had the named executive officer remained employed with us for 12 months following termination.

interesting take here on modeling buyout numbers/value.

Otsuka has Japan.

DSE has Europe, some southeast asia, and south america.

both owe milestone payments and royalties, although DSE royalties of $500m (approx) were bought out by Omers as part of deal to eliminate debt. But Esperion gets the royalty stream back after that.

So it is basically saying: if companies were already going to have to pay $X for these territories and royalties/milestones based on sales expectations, the US business is practically valued at $0 for any buyout under $2b.

Current mkt cap is $400m, but with exec stock awards (still not fully issued?) perhaps we should just call it $500m mkt cap now for easy math at $2/share.

So you shouldn’t be happy with a buyout under $10/share? That would be great. Curious what others think though. When I first got into the stock, I penciled in on my trusty napkin “$12”. But the longer the price stays buried at $2, it seems like you “settle” for $6-8 mentally.

Dreamer

I guess that was 5 days ago. I did add some at 0102 on 8/8 my local time, 1202 on 8/7 for most of youse guys. $1.9588. Now 4.01% of IRA.

FWIW, Esperion filed Form 8 stating the Chief Medical Officer is “transitioning”, her employment ending on or before September 16. Didn’t seem to cause even a ripple. She did get a one year extension to her exercise period for vested options. Why would one bail out from a 5 to 9x gain on additional stock compensation? ![]()

KC

Her employment contract was online. I think I posted it a couple posts before yours. Anyway, it reads like the cause was “sale event” as a likely reason for the exit. Also not clear that she walks away from any addl stock comp, as we don’t know if any awards were “accelerated” on the way out. May find out more after ER on Monday, whether on the conf call or via the updated SEC docs that follow.

She fulfilled her purpose of getting the drug thru phase 3 trials, CLEAR/MACE studies, expanded label, etc etc… Idea is that any acquirer or incoming partner is likely a big pharma with CMO in place so time to say “thanks Joanne!” and let her start looking for a new gig now and she gets the 12 month extension on her vested options (again - don’t know if more were accelerated to her as part of this) and she was making about $1.4m I believe and basically got that as a Thank You in severance, on top of continued health care, etc…

If this isn’t tied to an eventual acquisition, then it makes no sense and/or is bad news. I lean toward the former for now.

Dreamer

ER conf call in 30 min

Not a lot new in PR though

US sales $28.3m, so just shy of my goal, but “ok” given June accelerated as expected.

Earnings (Loss) Per Share. Basic and diluted net losses per share was $0.33 for the second quarter ended June 30, 2024, and $0.01 for the six months ended June 30, 2024, compared to basic and diluted net losses per share of $0.46 and $1.19, for the comparable periods in 2023, respectively.

Cash and Cash Equivalents. As of June 30, 2024, cash and cash equivalents totaled $189.3 million compared to $82.2 million as of December 31, 2023.

The Company ended the quarter with approximately 194.6 million shares of common stock outstanding

updated US sales numbers

I downgraded my 2h-24 proj just slightly, as a nod to them falling just short of my $29m Q2 goal. Would rather underpromise/overperform from here. This makes a 60% y/y growth, but reality is the Q/Q growth (projected) in 2H-24 indicates a pace closer an annualized 100% y/y growth momentum into 2025.

Let’s see how it actually plays out and/or if they wind up partnering or getting acquired by a Big Pharma (BP) for US business before EOY.

They still need the occasional milestone payment, of which they still have $300m from DSE in play and $600m from Otsuka still in play, likely paid out in 2025 and 2026/27, to stay profitable in short-term. But reality is they are outsourcing their tablet manufacturing expense to DSE and that should be done before end of 2025, which reduces COGS greatly. So they are pretty close to profitable on just US sales alone in a couple Q’s. Add in the milestones and peanut-butter-spread them over course of a FY and they are pretty much profitable now in 2025 and beyond.

Dreamer

Dreamer

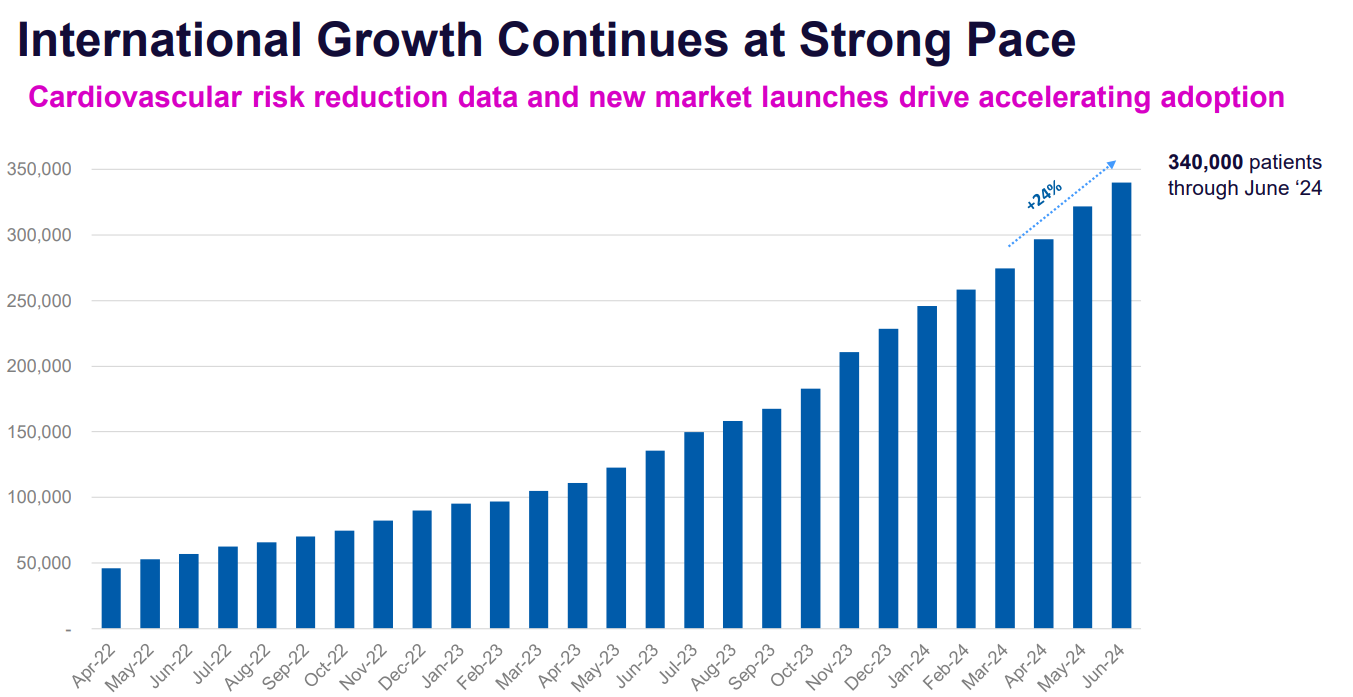

this slide slightly updated from prev Q

and new updated Aug corp preso/slides here:

https://www.esperion.com/static-files/32e7bdfa-9f1b-4d96-b486-949e11361625

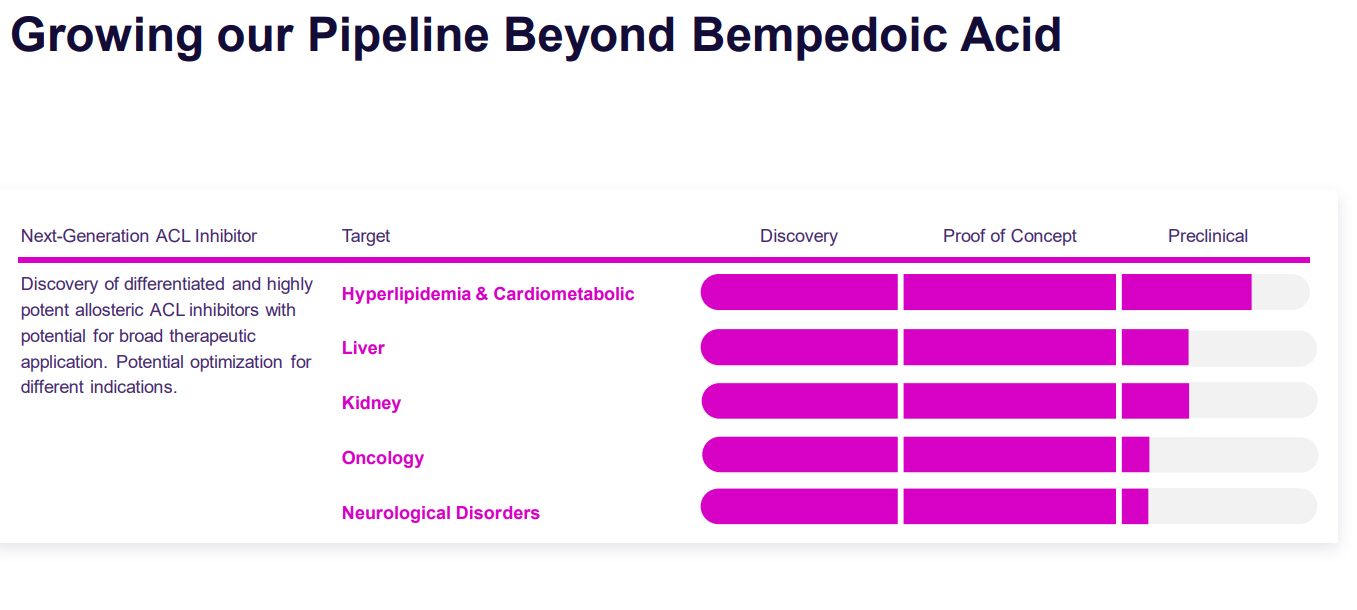

and this is sort of interesting, but also a head-scratcher with departure of their CMO (Foody):

It could be that a CMO specializing more in these other indications makes sense and/or simply that Foody departure truly signifies a likely incoming partnership/buyout and her duties become redundant w incoming CMO.

Dreamer

this is the type of stock to try a man’s soul though…not for the faint of heart!

10Q is out. Not much new to report that I see.

I guess one comment is that based on warrants and options and stuff (not my area of expertise!) the current shares may be 194m but I think you should just pencil in 240m all said and done.

So if you think they should sell for $2b price tag, then just know $2 is equivalent to $480m mkt cap…so let’s just round up to $500m for easy math.

$500m mkt cap = $2 stock price, fully fully fully diluted.

Think they will sell for $2b total? Then selling price should be $8/share.

Over in stock mssg board hell, they are postulating $1.50 is back in play due to gaps or whatever TA wizardry they like to employ.

So can it go lower? Sure.

Do I know what it will sell for, or that it will sell at all? Obviously I can’t know for certain.

The math that keeps me sane:

These guys (OMER) History

thought it was a good idea to give Esperion $300m just for the rights to the royalty stream of their partner DSE. They will get 1.7x their investment back or let’s just say $500m, and then royalties return to Esperion.

DSE just did about $50m in USD their latest Q. Royalties were 15% ($7.5k) but at some point they go higher (up to 25%?). So using 20% as a guide and assuming DSE continues ramping about 16% sequentially for a couple years:

I think they get about $60m in next (4) Qtrs in royalties

Then about $120m the next 4 Qtrs after that.

Then about $225m the next 4 Qtrs (now we are in mid-2027)

That brings them to about $400m and likely hitting the $500m cap in early 2028.

This is an investment company for a pension plan. Not some random dude on the internet like me. They put $300m at risk.

In addition, there are (undefined) sales milestones for both the DSE and Otsuka partners that supposedly still add up to around $900m. Esperion still get the DSE milestone payments along the way, even if not the royalties for a few years.

So if you buy Esperion, you have:

So what is all that worth? How about just the components?

So how is this not worth $1.2b min? $2b seems more than fair.

You take on risk, and want to make money from your investment, and not just break even, so while you should/could make $4-5b in revenues over next 5 years, you want to pay less than that, I get it.

So give me the $2b buyout or $8/share.

thanks,

Dreamer, graduate of Napkin Math University, class of '99.

An S8 filing dropped too.

Employee comp registration or something.

With cmo departure and now this…where smoke is fire?

Summary of the S-8:

Esperion Therapeutics, Inc. has registered additional shares of Common Stock under two plans:

These registrations were made through the SEC’s Form S-8. The information in previous registration statements (Registration No. 333-265247, Registration No. 333-273555, and Registration No. 333-243757) is incorporated by reference, except for “Item 8. Exhibits”.

The purpose of the 2022 Stock Option and Incentive Plan and the 2020 Employee Stock Purchase Plan (ESPP) is to provide benefits to employees and align their interests with those of the company. Here’s a bit more detail on each:

Stock Option and Incentive Plan: This plan allows employees to buy stock in their employer at a discounted price². The options vest gradually over a period of time known as the vesting period². This type of plan is often used as a form of alternative compensation, particularly in startups². It provides employees with the potential for a significant payday if the company’s stock price increases².

Employee Stock Purchase Plan (ESPP): This is a company-run program in which participating employees can purchase company stock directly, often at a discounted price. Employees contribute to the plan through payroll deductions, which build up between the offering date and the purchase date¹. At the purchase date, the company uses the employee’s accumulated funds to purchase stock in the company on behalf of the participating employees.

I am trying to understand why they have to do this. Most ESPP plans I have had work the about the same. Let’s assume the discount rate is 15%, then the plan sets a price and lets you buy shares 15% below the plan rate or the share price, which ever is lower at the time of issuance, usually every 6 months. If share price goes down, then the rate you buy is going to decrease and share needed will go up. So that may be the need to increase shares otherwise the ESPP plan have issue to function but wouldn’t the 2020 plan be defunct? Or maybe they have different employees on different plans.

Dunno.

I just read it as employee stock comp/options push as the stock price sinks and CMO is shown the door and payers mostly all on board, etc etc…

Seems like the time for a US partnership or sale is anywhere from tomorrow to next few weeks or next few months. No way of knowing if it happens for sure or not, but Q3 numbers “should” be pretty solid against another $20m Q3-24 compare. I think they will clock in around $33-35m and that is 65-75% y/y growth and at that point is it hard to deny this has become a growth stock, imo. Stock will hopefully rise accordingly, if it hasn’t already along the way.

So feels like mgmt/employees aligning themselves with potential buyout.

Or could be all random coincidence.

Dreamer

Here are my recent buys:

8/07 $1.96

8/12 $1.91

8/13 $1.86

8/13 $1.82

8/13 $1.89

Average price down to $2.06., down 12.7%. Now 4.4% of the IRA portfolio.

I might buy more for trading.

KC

typical for small cap bio stocks. You think you understand everything and then assume that prices will rise and the stock falls into the abyss. My biggest concern is the 262 mil convertible notes 2025. How will these be paid off? Dilution?

My average is $2.18 … Will likely sell with small profit EOY