My portfolio is up 32% as of writing on 3/26/2022 from when I started tracking my results in January of 2020. Meanwhile my benchmark, WCLD, is up 6% since January of 2020, and the S&P 500 is up 23% since January 2020. For the period from January 1st, 2023 through 3/26/2023, my portfolio is down 1%, meanwhile WCLD is up 11%, and the S&P 500 is up 4%.

- 2020 Performance: 225% (not a typo)

- 2021 Performance: 30%

- 2022 Performance: -69% (unfortunately, also not a typo)

- 2023 Performance: -1%

Cumulative Performance 1/1/2020 - 3/26/2023: 32%

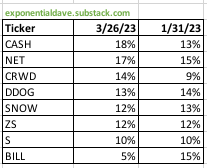

Current Positions 3/26/2023 vs 1/31/2023 (before earnings season):

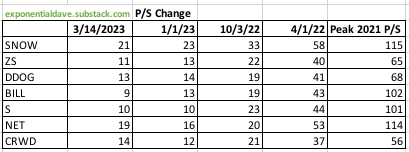

Valuation by P/S:

Earnings Season

Regarding the most recent earnings season, on the whole I would say that Bill, Snowflake, SentinelOne, and Datadog did not live up to my expectations, which admittedly are high because of the incredible results these companies have historically put up for many years in a row. This is not to say any of these companies performed poorly from an objective standpoint. As you will see in the individualized company reports below, all of them are still growing revenues despite a challenging macro environment, albeit slower revenue growth than we are used to. And all of them are either already profitable or continuing to trend toward profitability.

On the other hand, Crowdstrike, Cloudflare, and Zscaler all met or exceeded my expectations.

At the end of the day, BILL is the only stock I ended up trimming noticeably, but I would also like to trim Snowflake, S1, and Datadog when I find other places to put the money. (might soon be looking into Enphase, MNDY, TTD, GLBE).

SentinelOne

At first glance I liked SentinelOne’s latest earnings report, but after closer inspection at SentinelOne’s historical performance as well as the performance of their closest competition, I actually came away wanting to own less of SentinelOne.

Revenues grew 10% QoQ and 92% YoY to reach $126m. For any other company, this would be quite good. But for SentinelOne to only grow 10% QoQ, well this is a big disappointment because the average of their QoQ growth in 2021 was 22%, and in 2020 it was 18%.

They’re growing basically just as fast as Crowdstrike, but without any of Crowdstrike’s free cash flows and off a way smaller revenue base! Crowdstrike’s revenues were $678m in its most recent quarter versus SentinelOne’s $126m.

People are pointing to ARR growth as a better metric, and if you go by ARR, you see that S1 is doing a good deal better than CRWD, with S1 ARR at 13% QoQ and CRWD at 10%. Although they are right about it being a better metric and about it being more in S1’s favor, S1’s ARR growth used to be roughly double CRWD’s. Now they are only a few percent away. Those few percents are meaningful, but the gap between the two is much narrower now. The case for owning S1 is much less compelling - it’s easier to argue now to just own Crowdstrike.

When macro improves (whenever that might be), perhaps SentinelOne could reaccelerate to its former glory days. I never bet on re-accelerations though, because the math of large numbers makes it much harder. (the famously known cliche known as the law of large numbers)

Additionally, revenue guidance for the full fiscal year is for 54% growth, up from the 52% number they gave last quarter. It’s worth pointing out now, they did 10% QoQ growth this past quarter and 12% the quarter before that. 10% growth annualizes to 46% growth for the year, quite a bit shy of the 54% they think they’ll get. That means the c-suite thinks that revenue growth will accelerate from here. In other words, the SentinelOne c-suite is betting their word on revenue growth acceleration in a tough macro environment.

On the one hand, SentinelOne’s management has historically been quite good at underpromising and overdelivering. On the other hand, betting your reputation on revenue growth accelerating is a risky bet! And it’s not like SentinelOne has any obvious tricks up its sleeve to get revenue growth back up that it isn’t already doing. For example, my first thought was maybe they could just ramp up sales and marketing, but SentinelOne has kept the pedal to the metal on sales and marketing costs. And even with soaring S&M costs, SentinelOne’s revenue growth has only faltered.

Let’s look at their other KPI’s to get a more full picture of how S1 is doing:

- Revenue beat over guidance: 1%, their lowest beat ever by a long shot

- NG GM: 75%, their highest ever by several percent

- NG Op Loss Margin: -35%, a huge improvement from last year’s -66%

- NG Op Expenses: $186m, much higher than last year’s $112m

- NG net loss: -$37m, an improvement from -$44 in the prior year.

What I see here is a business that used to have absolute best of the best revenue growth, and now their quarterly revenue growth is not any better than my other stocks. And their profitability metrics, while improving, are still a long ways off from being what anyone could consider to be good.

Zscaler

Zscaler dropped what appeared like a pretty great report on the surface, but the market dinged it 10% afterwards, leaving many of us wondering what the problem was.

If I had to guess why, it’s the billings numbers, which have continued to fall each quarter. Normally I’d say revenue growth (which was great) is more important than billings, but Zscaler is the rare case where management has repeatedly told us in conference calls that billings is the best way to look at the business.

Billings fell to 34% YoY from 58% YoY in the comparable quarter last year. It’s basically been a linear shot down from 74% as recently as 6 quarters ago. Management’s explanation for this from the earnings call is here:

“Billings were impacted by new customers being more deliberate about their large purchasing decisions at the start of the calendar year”

But on the positive side, most all their other KPI’s looked great:

- Revenue growth of 9% QoQ (business as usual) which is a guidance beat of 6% (also business as usual)

- Increased annual guide to 43% (from 40%)

- A revenue guide for next quarter of 3% QoQ growth (not as high as the comparable quarter last year’s guide of 6%).

- Record NG net profits of $57.6m, and improved GAAP net loss substantially from -$100m in the comparable quarter last year to -$57m.

- Improved free cash flow to $63m or 16% of revenues, up from $29m or 12% of revenues.

And one more note on billings, revenue growth never follows billings perfectly, in the sense that billings growth was at one point 74% YoY but revenue growth never got up that high. Similarly, we can expect that revenue growth will not necessarily dip down to 34% YoY (where billings is now). Although it certainly will happen at some point in the future, because no one stays in hyper growth forever.

Snowflake

Snowflake’s revenue growth guide for 2023 was 40%, much lower than last year’s 67% guide. And importantly, it was a decent step down from the 47% growth they had promised one quarter earlier for fiscal 2024. It’s never a good look for a company to downward revise their own guidance. This was an odd misstep for a seasoned management team who we expect better from.

Product revenue growth was 6% QoQ, 3% over their guidance. This translates to 54% YoY, a large step down from last quarter’s 67% YoY growth (and the preceding quarter’s 83%). The revenue growth guide for next quarter is 3% QoQ, which is the same they guided for this past quarter.

Million dollar customer growth was a bright spot, growing 15% QoQ to 330. While it isn’t their highest ever QoQ growth rate, it is certainly pretty great. And they also continued to add global 2k customers, gathering another 6% QoQ.

Net retention continues its slide from a staggering 178% five quarters ago to 158% now. Keep in mind though, 158% is still outrageously high. No other software company close to its scale has a 158% net retention rate.

RPO grew 23% QoQ which sounds great. But comparatively, last year’s RPO grew 44% QoQ, as did the year before’s.

NG net income was a record $49m. But GAAP net loss continued to grow to -$207m, substantially worse than last year’s -$132m. In this environment, markets are allegedly caring much more about GAAP profits, but frankly it feels more like markets care more about rising interest rates than growth stocks becoming profitable.

Lastly for profitability metrics, NG adjusted free cash flows was a record $215m, which is fantastic.

On the whole, revenue growth has dropped a lot and guidance for the full year was lowered, so it’s hard to say that this was a good report. The continued strength in non-GAAP profitability metrics helps the report avoid being in disaster territory.

DataDog

DDOG got bit after its earnings where it reported incredibly weak annual guidance of 25% YoY. To put things in perspective, it guided last year’s growth to 49% and sharply bumped up its guidance to 58%, 49%, and 61% at each succeeding quarter. I feel confident to say that DDOG’s management team intends to bump guidance up a lot next quarter, but it’s hard to see DDOG’s actual revenue growth for 2023 ending up much higher than 40% in this environment. Q4 is historically a good quarter for them, and it was their weakest quarter since June 2020 (covid).

QoQ growth in the reported quarter was 7%, much lower than the 11%-15% ish range they used to consistently hit. And guidance for next quarter’s revenue growth is naturally not very great either, coming in basically flat. It’s important to recall though that we have been monitoring management for a long time now. They’ve issued quarterly guidance 14 times and beaten it by at least 3% (often much more) every single time.

Million dollar customer growth was 47% YoY, which sounds nice, but it’s much lower than the prior year’s 114%. $100k customer growth continued its deceleration to 38% YoY, which has fallen steadily now for 5 quarters in a row.

Profitability metrics remain solid, with free cash flows at $96m and NG net income at $90m. GAAP net loss was a manageable -$29m, although that is worse than last year’s $7m GAAP net income.

My summary is that the report was pretty bad because guidance was SO bad relative to the prior year’s. Hopefully this proves to just be conservatism, as DDOG’s management has always significantly underpromised and overdelivered in the past (the way it should be).

Cloudflare

Cloudflare finally broke out of its revenue growth range of 47%-54% YoY, a range which it had stayed in for as far back as my YoY data goes (Q3 2019). That’s 13 quarters, which is incredible. Anyhow, revenue growth for this most recent quarter was 42% YoY, which is not as good as usual but not hugely worse either.

QoQ growth was 8%, which was a guidance beat of 8% (they had guided flat).

Guidance for the coming year is 38%, which isn’t much worse than usual. For comparison, last year’s projection was for 42%, and the prior year’s was for 38%.

Profitability metrics are good, with NG net income at a record $21m and GAAP net loss narrowing to -$46m from -$77m the prior year in the comparable quarter. Free cash flows were $33.7m, much better than Cloudflare has done as far back as my data goes.

Objectively, this report was not bad, and certainly one of the better reports of companies I follow. Revenue growth was not as consistent as usual, but in reality it was just 5% lower than usual on a YoY basis. And importantly, their annual guide is business as usual.

Bill

On the whole I don’t like Bill’s most recent report. After their last report, this is what I wrote on Twitter and the board here:

It’s understandable why BILL stock is getting beaten after hours:

- Bad revenue guidance of -5% contraction for next quarter. They haven’t guided this poorly since 2020

- Looks like half their revenue growth is becoming dependent on float revenue growing, which only increases when interest rates increase

- Divvy growth, while still high at 78% YoY, seems to only plummet with each passing quarter. Three quarters ago it was at 155% YoY

The quarter wasn’t all bad though:

- QoQ revenue growth was 13%

- NG net profit soared to a record $49.4m, much higher than last quarter’s record of $17m.

- FCF smashed records, hitting $47m in a single quarter

All in all, I see BILL as having headwinds when interest rates eventually flatten or start heading back down. Bill seems more likely than my other holdings to fall short of expectations in the medium term , so I ultimately decided to trim my Bill holdings substantially, from about a 14% concentration to 5%.