After the good discussion about Aehr and how it is being impacted by the EV makers slowing down, do we apply same reasoning to Tesla?

If people are seeing the opportunity costs with Aehr, then should we see that same opportunity cost in our EV stocks? Some people on the board own Tesla, so will that be sold? (It is getting hit before market right now.) I don’t think any posters here own Rivan, but I have same sized small position in that as Tesla.

Just wondering about how people might link industries/investments in a situation like this?

“Just to point out how bad this quarter was. AEHR only had 2.2 Million in Bookings and 3.0 Million in Backlog. That has never happened since they IPO’d. This was an exceptionally terrible quarter.”

Let’s see. Two million dollars in quarterly bookings! How does that compare with Tesla??? Are they in any way comparable??? What a laugh. (I’m not in Tesla, by the way).

Saul

Yes, due to ”The Innovators Dilemma”, EV maker that are not Tesla are cutting back production. All other automakers can no longer afford to take the steep looses when trying to sell their EVs. This is obviously terrible for AEHR. However, this is not terrible for Tesla!

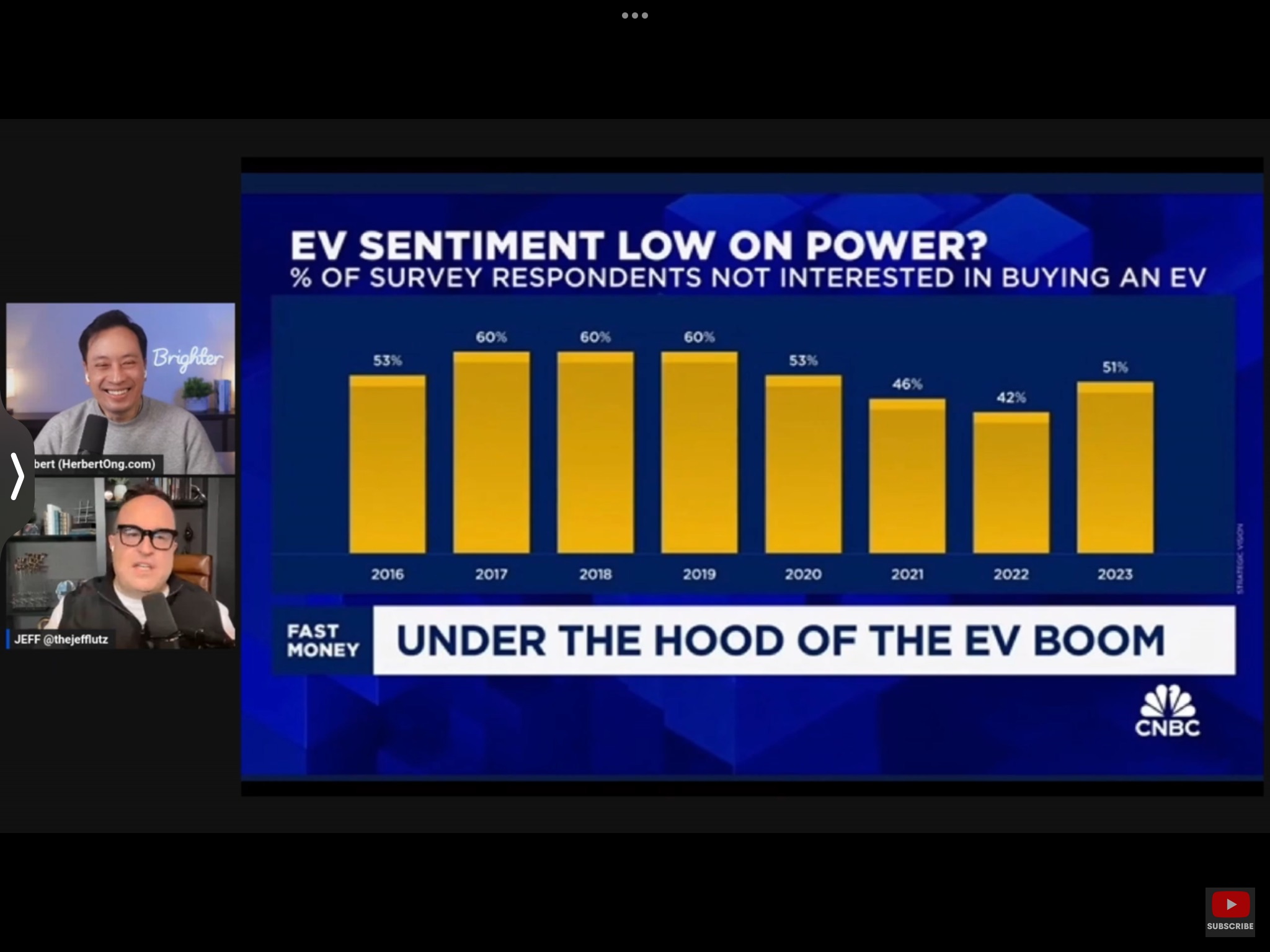

Remember, Tesla does not advertise. Despite what mainstream media being paid to report by all other automakers, customer adoption rate of EVs is massively under servered. Look again at the graph above. The headline might lead you to believe EV adoption is poor. However, what the above is actually stating is that, of those living in North America, 49% a intend to buy an EV as their next car!

Tesla is not only taking share from other EV purchasing decisions. Tesla has now overtaken VW in total sales of all types of vehicle sold in the US!

I sold my tiny Rivian position in November. Kept Tesla because it’s a different animal altogether. They lead, they don’t follow.

And so did Rivian (on the front motor). And all the motor manufacturers that supply electric motors. SiC is very experience.

We talked about this on other threads. Most are not necessarily cutting production, but are not expanding as it was planned. Some had cars piling up on dealers’ patios, but so did Tesla (Tesla cut the M3 price so much that the effective price was less than $30K).

This is the car industry. I think EV sales, which is still a luxury product, is very strong if you take into consideration the high interest rates (always a killer for car manufacturers) and cheap-ish gas. These are cyclical and always will be.

You know, I have been in and out of TSLA largely because my 401k does not allow direct exposure so I have to use a 1.5X derivatives-based 1-stock ETF. (Oh, the irony, people cannot be allowed to own stocks but can be allowed to own any ETFs).

But I have definitely noticed that in Fall 2023 there seemed to be a hit campaign in the media against Tesla.

Can you please share your reasons for your change of mind regarding Tesla vs end of Dec report?

(Mine is simply the opportunity cost relative to other options, but it is all short term and all about a restricted 401k so there is no point in listing my reasoning here as it is of zero benefit to others.)

I don’t think this is the right comparison and lesson to learn here. We are looking to invest in great companies. TSLA is a great company as its products are being used by lot of customers. Even though AEHR is in similar industry of testing SiC for EV’s, its not a great company and I don’t think it ever will be. The main reason here is the AEHR has huge customer concentration and this is not the type of company we want to bet big on in a concentrated portfolio.

I usually overlook short term quarterly noise as a long as I am invested in great companies, but AEHR is just not it.

We all want to know what Saul is thinking when he buys/sells, so we can learn how he thinks about things and maybe improve our own thinking. Since he hasn’t responded (yet), this gives us an interesting opportunity to think for ourselves.

I have learned some things about Saul’s thinking over the years, but I don’t always see it right away. And there’s a lot I haven’t adopted – for example, though I’m not in TSLA (don’t think I’ve ever been), if did own some, the fact that it’s down 12% ytd in just a couple weeks would have me considering adding to it. That said, Remitly is down 7% and I’m not adding to it. The reason with Remitly is that though the opportunity seems great and it seems to have way more upside than downside, my conviction isn’t super high. Maybe that’s how it was with Saul and Tesla? And maybe that’s a lesson I can learn: if your low conviction position is losing, cut it loose. I haven’t been as quick to do that as Saul historically…I usually wait until it’s more clear…and a lot of times the stock is much lower.

Or maybe Saul simply saw a better place for the Tesla money. If I had to guess, maybe he added to Nvidia. If he has 2 positions he feels similar conviction about and one is going down and the other is going up, he many times starts to favor the one that is going up. Kinda makes sense, huh? I’m not like this…maybe I should be. Seriously, if a low conviction holding of mine goes up, I usually trim at least a little, thinking, “whew!” I like gains and I like the fact that I can take a little of a low conviction position off the table. But maybe I was right! And so it’s silly to trim. Maybe… This is another potential lesson.

Or maybe Saul just got tired of looking at TSLA, I don’t know. But I’ve learned 2 potential lessons without him explaining anything, so thanks, Saul!

I’m long TSLA for the long haul and I very seldom trade it anymore. Now, on occasion, I buy an even lot and sell covered calls against it. The last time I did that was from November 1 to November 17. Now I’m waiting for the Earnings Call, January 24, to see what else I might do.

In my opinion Tesla is the best long term hold in the market but with a very distant horizon. Like Apple and Amazon, Tesla is a trend setter. Already legacy automakers are starting to copy Tesla, specially the Chinese automakers. In under ten years EVs will be commoditized and no longer be the core business for Tesla just like computers and books are no longer core for Apple and Amazon. Instead the so called ‘adjacent possible’ will become core. For me the biggest attraction is the AI powered humanoid robot which will enter service at Tesla factories very soon, most likely this year. Having these factories as sand boxes for the robots to play and learn free from the interference of customers, analysts, the press, and Tesla/Elon haters gives Tesla a leg up on other humanoid robot ventures that have to rely on external sand boxes.

I found Agility Robotics quite interesting. A number of Fortune 500 companies have expressed interest in their products. I can’t find the reference but I heard the CEO say it.

From an investing point of view, humanoid robots have not Crossed the Chasm which is the event that reduces investor’s risk as the technology is more than likely to survive and thrive. Tesla is a special case in the sense that one can get in early with relatively low risk because the stock has many other legs to stand on, something that most other robotic startups don’t have.

Okay, I’ll give in. I sold Tesla because I found something I liked better. I watched those two recommended interviews with the CEO of NU Holdings and took about a 5.5% position about a week ago, the first few days of the year, almost all at $8.24. He really inspires confidence. (It closed this week at $9.26, up 12.4%).

I sold all my Tesla and a tiny bit of CELH, and put a little of the cash into my permanent cash position, and used the rest to buy the NU and add a VERY little each to AXON, Monday, IOT, and ELF. Oh, and I took a 0.5% position in NVDA, which I may or may not hold on to. It may be a big mistake to not hold on to Tesla, but that’s what I did.

Best,

Saul

As you can tell, I’m quite undecided about Tesla and Nvidia. But feel much more confident about my top five: IOT, ELF, MNDY, CELH, and AXON. Fairly confident about NU too, but it will never be even a 10% position.

Nvidia has 90% market share of a trillion dollar buildout of datacenters and a very strong MOAT with it’s CUDA software. It looks likely that it will take at least a year or two for the competition to start making a dent. I’m curious - why you are on the fence?

Also, I’d love to hear why you dumped TTD. It’s a proven winner with a large TAM that is taking market share. 2024 could be a great year with the Olympics and General Election, and a possible rebound in the ad industry.

Hi Jeff, good question. The Trade Desk keeps saying that it’s taking market share and it certainly has a very congenial CEO. Okay, in spite of all that “taking market share” its growth rate keeps plummeting.

The last four quarters their average growth rate has been 24%. The four quarters before that they averaged 33%. Does that sound like they are taking market share? If so, you’d have to wonder whether that “market” might even be shrinking.

I know very little about the ad industry. Sure there’s an election year coming. But that’s a temporary, once in four years event, and everyone will know that.

Their trailing one year EPS is $1.22 and their stock price is $67, so their trailing PE is 55x earnings, and they grew at 25% last quarter.

So why should I be in this company when I see better opportunities?

Okay, let’s compare. Let’s look at Elf for instance. Elf’s revenue growth rate was 76% last quarter, compared to TTD’s 25%. They are growing three times as fast.

Elf’s growth rate in the year ago quarter was 33% so they are growing well more than twice as fast as they were growing a year ago! Now, to me, that’s “taking market share”. Compare it to TTD’s 25% growth rate, down from 31% a year ago.

Lest you think that ELF is just growing fast but not profitable, their trailing adjusted EPS is $2.82 !!! (and growing at 76% !!!) Their stock price is $157.60, so their trailing PE ratio (55.8x) is essentially the same as Trade Desk’s. But Elf is growing its revenue 3x as fast.

While 49% intend to buy an EV as their next car(as do I) I wonder how many are factoring in the logistics of installing a charging station? I probably wont buy an EV until I’m prepared to install charging station AND a solar+battery accompanied charging system. It feels like many Americans are entering the flat part of the S curve right now?

Installing a charging station at home is a $1000-$1500 one time investment that will pay for itself quickly. Why are you coupling your EV timing with the more expensive solar/storage decision?