## Portfolio Management

The number of stocks in my portfolio waxes and wanes according to a number of things, but probably never is less than 8, or more than say 15. Okay, so what makes the difference?

If I have stocks that I have strong convictions about I will tend to add additional funds to them instead of looking for new stocks, and I end up with a more concentrated portfolio.

If I have less conviction, or if some positions have become too large, I will try out a lot of smaller positions in order to decide which ones I should add to and make into ongoing positions.

Consider, for instance, if something were to happen and I were to have to exit my largest position now. That would be a big part of my total portfolio. I wouldn’t put that much into any one or two new stocks, nor would I add that much to existing positions. I’d probably have to reallocate the money to five or six smaller (3% to 4%) positions, and maybe one or two “put it on the radar” (1% to 2%) positions.

When the market tanks irrationally, I tend to reduce or eliminate the stalwart stable stocks that haven’t declined much and thus won’t have much of a bounce, and reinvest the money in the great, fast growing stocks, which have declined a bunch with little or no reason except that the market is falling. This also tends to concentrate my portfolio. I might buy some of a new stock that has fallen in one of these panics, but it’s difficult emotionally to put money in an unfamiliar stock when there’s panic all around.

When I think my main stocks have gone up irrationally, are over-extended, and the positions have gotten too large, I tend to trim them and put some of the funds back in the stable stalwarts and some in new “try-out” stocks. This increases my number of stocks. (This is similar to B.)

I really like it better when I have fewer, but high conviction stocks. I’m more comfortable, and I can probably make much higher percentage gain for my portfolio with 8 positions than with 24. Fewer are easier to follow, and the chances of finding 8 that will average 50% gain is MUCH better than the chances of finding 24 that will average 50% gain, and HUGELY better than your chances of finding 100 that will average even 40% gain.

When do I sell?

I tend to sell a piece if my position has gotten too big for me to be comfortable with. However, I have let rare positions get very big if I was in love with the company.

I tend to sell a little piece if I feel the price has shot up wildly. On the other hand, a stock might go up steadily, but if my position isn’t too big, the rise isn’t too fast, if their metrics are improving nicely, I may add multiple times along the way instead of selling. In other words I don’t sell just because something is going up.

I tend to sell a piece if I feel the story has changed.

There really are some times when it makes sense to sell a stock. Saying that “it would be better if I held” because at some time in the future the price may go back up up is not valid (it’s silly, even). Just think of a stock that you sold at $200. It dropped to $50. It gradually came back and now, 5 years later, it’s at $220. Would you say it would have been better to have held because it’s now up 10% in 5 years!!! That really is silly. You could have thrown the money at a dartboard of MF recommendations and beat that result by 500%. And could have done lots better than that by intelligent picking.

There’s a big opportunity cost to leaving your money in a stock which keeps going down, and then stays down, as well as whatever paper loss you have.

If I need cash for an attractive opportunity, I:

(1) sell a little of stable, slower-moving companies that I have confidence in, but which haven’t fallen hardly at all and which aren’t going to run away from me when the growth stocks start back up.

(2) sell a little of high flying stocks with growth that doesn’t warrant their high valuation, and which therefore seem vulnerable.

(3) sell my little experimental positions in stocks which may turn out well in the future, but where I have surer places to put my money.

Since I’m almost always nearly 100% invested unless I’ve recently sold out of a big position, I often don’t have the money to take a full position all at once. If it’s something I absolutely fall in love with, I’ll jump into it right away with whatever money I have available, and will likely trim some other large positions to fill out a full position. If I’m not sure, I’ll take a small position to put it on my radar. I then may start adding more as money becomes available, often building to a “full” position, which for me is an average-sized position, not an oversize position. Or as I get more familiar with the stock that I’ve taken a starter position in, I may say to myself, “This is stupid, it’s not my kind of stock”, and sell out of my starter position. That does happen.

I usually keep enough for a couple of years worth of living expenses in cash that I don’t consider part of my investing account, or part of my portfolio. I keep it firmly in cash.

We all tend to get worried or elated over moves of our stocks with no news attached. This is usually random noise. For a trivial example, say your stock dropped from $58.70 to $58.30 from Thursday to Friday. Did anything happen that caused it to be worth 40 cents less on Friday? Of course not. The message in all this is to keep your eye on the company, and how it’s doing, and not as much on the stock price.

## Adjusted (Non-GAAP) vs. GAAP Earnings

I use adjusted results because they tell you what the real company is doing. I pay no attention to GAAP earnings and only look at non-GAAP or adjusted earnings. I know this bothers some people, but it’s what I do. I feel that GAAP earnings ridiculously distort the picture. (Consider company X that has a big tax benefit this quarter and reports huge GAAP earnings, and then next year they pay normal taxes and looking at GAAP it appears as if their earnings have tanked, just for a trivial example. Or company Y that has outstanding warrants. If their stock price goes down, GAAP rules makes their apparent GAAP earnings go up due to repricing of warrants. Just nonsense. I especially remove stock-based compensation as an expense).

I ignore the stock-based compensation because it is already accounted for in diluted shares. More shares reduces earnings per share. Taking it also as a non-cash expense double counts it, which is why almost every company that I know of subtracts out the stock based compensation non-cash expense insisted on by GAAP when they figure adjusted earnings or “real earnings.”

I don’t like excessive stock compensation either, but you have to remember that at most small technology companies, that is most of executive compensation, as the companies don’t have much money. It also allies the insider’s interests with ours if they have options that are only valuable if the price goes up.

In the earnings press releases, management almost always gives a reconciliation between adjusted and GAAP figures. You can see exactly what they leave in and take out so you aren’t taking it on blind trust. If I have confidence in management, I just use the adjusted earnings they give. This perhaps sounds overly trusting, but what I’m aiming for is seeing how the company has been functioning over time, and management is trying to evaluate the same thing. If I don’t have confidence in management, I shouldn’t be in the company in the first place.

It’s important that you realize just how insane some GAAP rules are. Let’s consider company ABC, which makes engines, and has some outstanding warrants. What would happen if some terrible news came out during the next quarter? For example, if a big new engine had a bunch of defects, or a new competing product showed up which was taking lots of their customers. Their revenue would drop like a rock, and their stock price would crash (for good reason!).

GAAP rules for repricing the warrants would mean that because the stock price plummeted, the company would show huge (imaginary) INCREASES in GAAP earnings for the quarter!!! And this is from a system that is supposed to be giving the public a clearer idea about what is really happening at the company!

(For those who wonder what their rational is, it’s: stock price down, means potential obligation from warrants is reduced, and thus more GAAP “profit”)

By the way, analyst earning estimates are almost always adjusted earnings too, as far as I can tell. Also the companies’ disclaimers almost always specify that management uses adjusted earnings for their own internal evaluations of how the company is doing. They always give GAAP results as a formality, and then usually base their entire discussion of results on adjusted results.

For those who think that GAAP are the only valid earnings, and that Non-GAAP are just “cheating,” these were the latest PSIX results, at the time I wrote this back in 2015:

GAAP earnings: 68 cents

Adjusted earnings: 39 cents

WHOA! Adjusted just about half of GAAP? It’s supposed to be the other way around! How can that be? Because, as usual, GAAP has a lot of nonsense in it: GAAP was up because the stock price was down so they had to reevaluate the “liability” of the warrants downward due to the lower stock price. This gave more GAAP “earnings”. (Note that if the stock price had been up, repricing of the warrants for more liability would give lower earnings. If you think that makes sense, well…)

In addition, GAAP income included a non-cash gain resulting from a decrease in the estimated fair value of the “contingent consideration liability” recorded in connection with an acquisition. This also gave more GAAP earnings.

Now if you think GAAP gives a better idea of how the actual business did in the quarter, be my guest. As I said, it’s nonsense to me.

## What is my Buying Policy?

What is my buying policy? I actually don’t have a fixed buying policy. That means you can rule out cost-averaging over a predetermined time. I never do that.

You can also rule out: “I am tempted to just wait a bit longer until the right opportunity arrives.” If I like a stock enough to take a position, I will always take at least a starter position, and figure on adding later. I never wait for the “right opportunity” to take a starting position. I do add to a stock when it goes down for no reason on an opportunistic basis, but you can’t take that as a rule, for some of my most profitable stocks ever I kept adding on the way up, instead of on the way down. (If I start buying at $25, adding at $28 or $31 might seem expensive, but when it gets to $75 or $120 the difference between $25 and $28 will seem negligible. Also if it’s at $25 and I wait for $22, to buy at a “cheaper price,” I’ll really kick myself when it’s at $120 and I never got in because of waiting for a cheaper price.)

As you can see, there’s no clear rule, but I was able to rule out two approaches (buying thirds at predetermined times and waiting for a cheaper price to add).

Remember you’re not locked in. Not infrequently I decide my initial purchase was a mistake, I don’t really have faith in this stock, and I sell out at a small profit or loss.

On the other hand, if I’m really excited about a stock I’ll take a substantial position right from the start. I’m more likely to do that with a MF recommendation or a company being actively discussed on our board than with a little stock I found myself. But I occasionally change my mind on those too.

Never miss getting into a stock because you are waiting to buy it cheaper. The decision is whether you want to invest in it or not. Once you decide, take a starter position, at least. Don’t wait around for a slightly better price.

Price anchoring is a BIG mistake. Treat a company as if you had just encountered it, and then decide, based on its current metrics and story, whether you want to buy it now. Where the stock price was in the past is irrelevant. You can’t go back and buy it at that cheaper price where it was two months ago.

When the whole market is falling, putting more money into your high confidence stocks usually works out very well in the end. On the other hand, when one stock is falling off a cliff in a rising market, it usually means that something is very wrong. Putting more and more money into it on the way down is usually very dangerous, and a way to lose a lot of money.

If the stock is going up, it generally means the hypothesis upon which you bought the stock is working out the way you hoped. The business is doing well, revenue, earnings, cash flow, and all the rest are going up. I’m glad to add to an idea that is working out. If it’s going up wildly on just hype I won’t add.

There are others who like to “average down,” which sounds good, but it often means adding to an idea that isn’t working out (watering the weeds, making excuses for bad news). Oh, sure, if my original purchase was at $73, and a week later it’s at $71 because the market is down a little, I might add a little. That’s just random noise. But if they come out with really bad news or a bad report and the price is dropping like a rock, I’m not one to say, “Oh, they’ll get it figured out. I’ll buy at this cheaper value. It’s a bargain.”

I saw the following question on a MF board and thought it typified what I wouldn’t do. Here’s the question: “With the disappointing XYZ results, is XYZ a buying opportunity?”

I didn’t know anything about XYZ, nor did I read their results, but the general idea of buying more of a company because it had bad results and the price fell, and thinking you are getting a bargain seems foolish to me.

There are exceptions: If a stock, after reporting excellent earnings, falls off a cliff because it didn’t meet estimates, or some such nonsense, but I know what the news was, I have read the conference call, and I know there is nothing wrong, at least that I could see, I don’t hesitate to add. (Maybe some hedge fund got a margin call on another stock and had to raise cash in a hurry and so had to liquidate my stock at whatever price they could get. Who knows? Irrational things happen.)

You can’t buy all the great stocks! (unless you run a big index fund yourself). Some stocks you pass on will go up. It’s guaranteed! Personally I don’t even think about them. I just care about how the ones I bought are doing. (THIS IS A KEY POINT, READ IT CAREFULLY!)

Where do I get my stock ideas? Many of my stocks were MF picks (mostly RB, actually), although I had invested in several of them before they were picked by MF. As I indicated above, I really prefer to invest in MF picks because the discussion boards and continuing coverage is incredibly important to me.

People on our board have introduced me to a large number of stocks with their posts. I’ve also more rarely gotten ideas from news articles and from random posts on other MF boards.

I’ve gotten some stocks from random Seeking Alpha articles. Note that most investing newsletters have no discussion boards and no real ongoing support, such as you find on MF.

## What is my Selling Policy?

I tend to sell a piece if my position has gotten too big for me to be comfortable with. Usually, that means more than 12% to 15% of my portfolio. However, sometimes I have let rare positions get to 20% if I was madly in love with the company.

I tend to sell a little piece if I feel the price has shot up wildly.

When I’m thinking of selling I seem to sell a little first while I’m evaluating, then decide for sure what to do. I might even decide to buy back the little piece I’ve sold if I reconsider.

One problem investors have is getting attached to their previous decisions and not willing to consider that they may have made a mistake. Not accepting that an investment could be a mistake is a dangerous error. I try to always reevaluate my investments and get out if I’ve made a mistake, or if information changes. Which is why I don’t hold stocks generally for 5 or 10 years.

I always buy with the idea of holding indefinitely, never with the idea of a short holding period, but in practice I guess my average holding period is six months to three years.

If a stock seems overly extended, I won’t sell out completely, but I’ll trim my position a little. Then if it goes up even further, I’ll trim a little more. If it drops back substantially, I might buy back some or all of what I’ve trimmed. I will never sell totally out of a position I’m very happy with just on the basis of valuation. I definitely don’t sell winners that have had a run-up as a policy. I only sell if I have a specific reason.

We all often worry when stocks we have sold go up. I try to ignore them and figure that once they are sold they don’t matter any more. Here’s a great quote from Huddaman: “I don’t really need to be right for the stocks I sell, I just need to right about the stocks I own.” Boy! Doesn’t that really say it all! It simply doesn’t matter what happens to a stock after you sell it. You can’t hold all the stocks in the market. Some stocks you don’t hold are going to go up. A lot! So what!!! The only thing that matters is what the stocks you are holding do!

Selling out at the bottom, when everyone is panicking, is not a good outcome. The time to have sold the wildly over-extended stocks, was when everything was booming. On the other hand, when the market is down, selling low-beta stocks that haven’t fallen much, and thus have less to rebound, can be a good source of cash to buy stuff that has fallen a lot.

There’s no such thing as “I was so far down I couldn’t sell”. The stock price has no memory of the price you bought it at. It’s at the price it’s at. That’s the reality of now. The question about any stock is “Where is it going from here? What decision should I make about it now, at its current price and its current prospects?” Not: “What price did I pay for it?” unless you are planning for tax losses or gains.

How to handle the emotions. I don’t even think about the price I bought the stock. I promise you, I don’t consider it at all probably 95% of the time (especially since most of my portfolio is in IRA’s). I think about a position that I’m considering selling simply as a part of my portfolio.

For example, a hypothetical thought process: My portfolio value is now at $xxx. AAA makes up 3.7% of my portfolio. It’s at a price of $yy. (That’s the price it’s at right now, and there is nothing I can do about it). Its fundamentals and its stock price are both deteriorating seriously, and there is nothing on the horizon that I can see that will magically turn that around anytime soon. Where can I put that 3.7% of my portfolio where it will have a better chance to grow?

As you see, there’s no consideration at all of the price I bought it at. In that thought process, the price I bought it at would be irrelevant.

You need to think of money as fungible, interchangeable. It’s only money. It’s not a share of AAA that you bought at $94, so you have to wait until it gets back to $94 before you sell it even if it takes five years. (Perhaps to make you feel better, so you won’t feel like you made a mistake when you bought it?) It’s just 3.7% of your portfolio, which as a whole is doing fine. Is there somewhere better you can put that money, that 3.7% of your assets, with a clearer path to a long-term good profit? That’s the question.

Do I wait for long-term capital gains? My results are for my entire portfolio, which includes various accounts, some taxable, some not.

Most positions I’d exit short-term would be losses or small gains. If a stock was really doing well I’d be more likely to add to it. If, for some reason, like a major change in the fortunes of a company, I had to get out of a position with a significant gain, I would do it in all my accounts, taxable or not.

Normally, to get to be a big gain it would mean I’ve held it for a year at least. It would be rare that I would be selling out of a stock with a significant short-term gain. So let’s say I do sell $120 worth of stock on which I have a $20 short-term profit. The key is that the tax is not on the whole $120, it’s just on the $20 profit. The difference in the short-term tax on that $20 profit and the long-term tax might be about $4.00. Should I risk the entire $120, keeping it in a stock I’m worried about, because I’m worried about $4 in taxes? When the stock could easily drop more than that $4 in a few days? When I could redeploy the money in something I prefer? I don’t think so.

## Calculating Portfolio Returns

I retired in July 1996, so I’ve actually been taking out money to live on for the last 20 years, instead of adding money.

Here’s how to calculate your overall returns ignoring cash flow in or out. Say you start the year with $14,000. You want to equate that with 100% and calculate gains and losses from there. So you ask yourself “What number (factor) would I multiply $14,000 by to get 100?”

By simple arithmetic we have 14000 x F = 100

And thus F = 100/14000 = .0071428

Sure enough 14,000 x .0071428 = 100

Now say three weeks later you have $14,740 and you want to see how you are doing, you multiply that number by .0071428 and you get 105.3 (so you are up 5.3%). If you don’t add or subtract money, that factor will work for the whole year.

Now say you add $2300 of fresh money, but you don’t want that to screw up your estimate of how well you are doing.

You add the $2300 to the $14,740 and get $17,040 which is your new balance that you are investing with. That’s your new starting point. It doesn’t affect how you’ve done up to here. You haven’t suddenly done better because you added money. You can’t still multiply by .0071428 because you’d get 121.7 and it would look as if you were up 21.7%, when you are really only up 5.3%.

So you need to change your factor to make it smaller so it will still reflect just the 5.3% gain you’ve made so far. You figure: “What would I multiply my new balance ($17,040) by to get 105.3, to reflect my 5.3% gain so far this year?”

F x 17,040 = 105.3

F = 105.3/17,040 = .0061795

And that’s your new factor. If you multiply it by 17,040, sure enough you get 105.3. Now you continue to see how you will do for the rest of the year.

If a little later you are at $18,000, you multiply 18,000 by .0061795 and you get 111.2, so you know that your investing is now up 11.2% for the year.

Same, if you take money out. You don’t want it to look as if you lost money. You calculate a new factor so you start from the same percentage where you were.

On January 1st of the next year, you write down how you did for the year to keep a record, and start over at 100 for the next year.

## Dips and Downturns

When the market is in euphoric phase, companies can report poor or mediocre results, but the analysts and investors will find some positive slant to bid the stock up. This will last until it reverses, and then no news is good enough. Whatever it is, the analysts and investors will find some negative way of looking at it, and the stock will go down. So don’t panic at irrational sell-offs. If it’s one stock, then you have to make sure there’s not something wrong with that particular company. When it’s all your stocks and the pundits are all saying the big crash is coming, relax. It’s just something that they say now and then.

Sometimes you can feel shell-shocked from the pounding you get from the market. All your well-functioning, rapidly growing companies, who have had no bad news at all, have sold off sharply for no reason. If the market is down, it will recover. It always does. If anyone says “This time is different, it won’t recover,” you should greet what he says with suspicion. Just hope that the recovery is sooner rather than later.

Remember how scared everyone was at the end of 2008. One financial expert, when asked what positions he’d be in, said “Cash, and the fetal position!” That’s how scared people were. — Well, I was up 110.7% the next year, in 2009. The market has now been up for 11 years since 2008. If I had listened to the doom-and-gloomers at the end of 2008, I’d have been in cash and missed it all.

I wrote this one day in 2014: “Just two weeks ago, people were writing in on the board to ask whether they should sell out of everything and go into cash, long term growth newsletters were taking on “short” ETF’s to protect themselves from a falling market, and someone on this board was suggesting maybe it was the start of a Bear Market. By coincidence, they all occurred on the bottom day for the market. It’s worth keeping that in the back of your mind the next time the market takes a little breather and you get unreasonably scared. If you’re scared, almost everyone is likely to be scared, and we probably don’t have much further to fall.” That was in 2014 and the economy has been up every year since. Don’t believe the gloom and doomers. Eventually we’ll have a recession and they’ll say “I was right all along!” but they were WRONG all along, beause they missed most of this 11 year bull-market

My preparations for the next market drop. That’s easy. I don’t try to time the market and I stay fully invested. I try to pick good, really excellent companies, who will do reasonably well even if the economy turns bad. In other words, companies that have a lot of recurring revenue growth, high gross margins, and little or no debt..

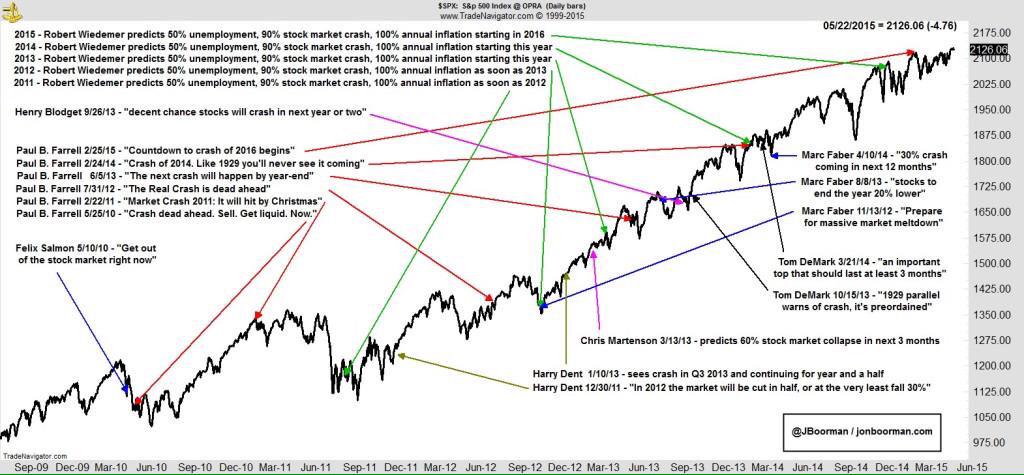

Why don’t I try to time the market? Because the experts can’t do it, so why should I think I can do it. There are people saying “Watch out for a market crash this year!” The only trouble is that they said that last year too, and in 2014, 2013, 2012, and 2011. And in 2010 they were warning about a “Double Dip Recession,” which didn’t happen either. Eventually they will be right, or partially right. Even a stopped clock is right twice a day.

Given all that, and that no one can forecast the market, here is my attempt to do so. Sure this has been a long Bull market. But this isn’t a euphoric market that charged out of the Great Recession. It has inched its way up slowly, climbing a wall of worry all the way. And it had, and could still have, a long way to go. Does this feel like a frothy market top? Do you hear any euphoria? Have you heard anyone calling for a massive market rise, anyone at all? Does everyone seem worried about one thing or another? And the market keeps inching up. The economy is growing, unemployment is falling, employment is rising, there’s no inflation, NO inflation, and no wage inflation. The market usually continues to rise for two years after the Fed starts raising rates, and they’ve just made one token little step. Give me a break! Relax and have fun investing. Sure, a correction will come along sometime, but we’ll all live through it. — I wrote that paragraph for the 2015 version of the KnowledgeBase and boy was I right. It still makes sense. Here is a wonderful compilation of all these guys who predict a stock market crash every year (often using the exact same words even, from year to year). It’s worth clicking through on it: https://pbs.twimg.com/media/CGVzK7_VIAAyCSH.jpg:large

{kind=link}

Right now (Jan 2020) we are in a growing economy, with low unemployment, low inflation, low interest rates, growing GDP, growing corporate earnings, and corporations are loaded with cash. This is a great environment for stocks, no matter what the bear market worriers say.

## On Insider Trading

I don’t give any guarantees, but insiders sell for all kinds of reasons, and undoubtedly have plenty of stock options that haven’t vested yet. I wouldn’t make any decisions based primarily on insider sales, without some confirmatory evidence. Just look up insider sales for Amazon, and you’ll see that there have been dozens of insider sales per month, all the way from when it was $5 (split adjusted) to its current $1900 per share. Why are the insiders selling some of their stock? Because it’s most of their portfolio, and they want to diversify, or buy a house, or send their kids to college, or buy a Tesla. You get the idea.

Heavy insider buying is something else again. It’s much rarer, and much more indicative.