Nobody wants to run out of money. Whether or not you plan to leave anything to heirs, every investor needs to estimate their life expectancy to attempt to ensure that their assets will cover expenses.

Social Security provides actuarial tables but these are whole-population estimates that don’t take personal variables into account. According to Social Security, I have a remaining life expectancy of about 16 years, which means death at about age 85.

A Number That Should Guide Your Health Choices (It’s Not Your Age)

Life expectancy increasingly figures into calculations about whether screenings and treatments are appropriate. Here’s how to find out yours.

By Paula Span, The New York Times, July 23, 2023

…

Slowly, some medical associations and health advocacy groups have begun to shift their approaches, basing recommendations about tests and treatments on life expectancy rather than simply age…

A 75-year-old has an average life expectancy of 12 years. But when Dr. Eric Widera, a geriatrician at the University of California, San Francisco, analyzed census data from 2019, he found enormous variation.

The data shows that the least healthy 75-year-olds, those in the lowest 10 percent, were likely to die in about three years. Those in the top 10 percent would probably live for another 20 or so.

All these predictions are based on averages and can’t pinpoint life expectancy for individuals. But just as doctors constantly use risk calculators to decide, say, whether to prescribe drugs to prevent osteoporosis or heart disease, consumers can use online tools to get ballpark estimates… [end quote]

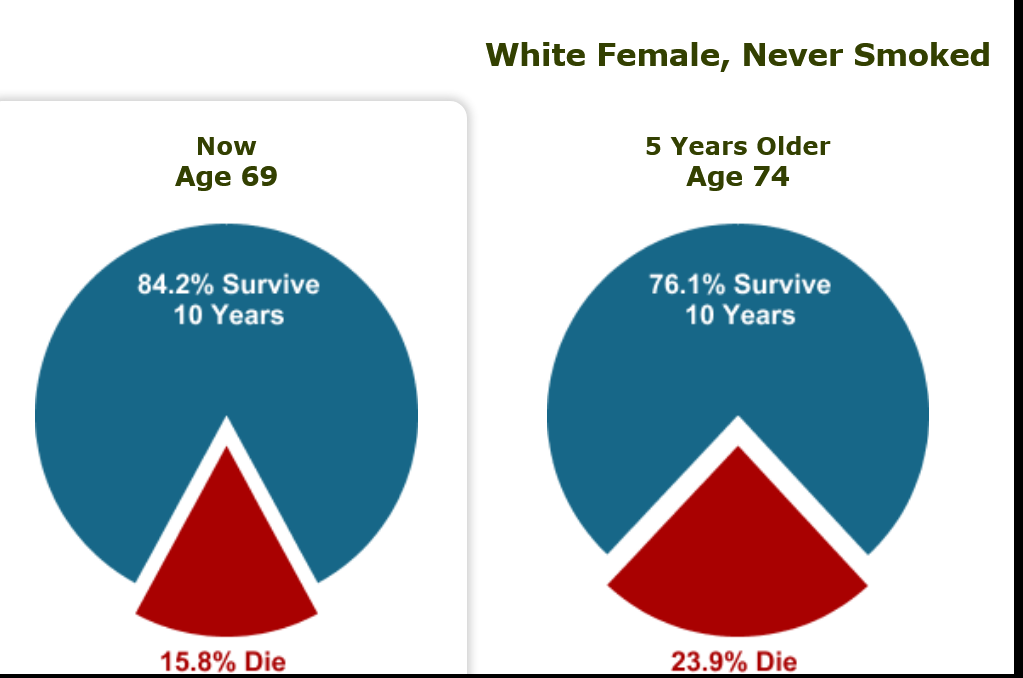

Here is the National Cancer Institute’s " Know Your Chances: Interactive Risk Charts." Risk charts present these basic facts by showing the chance of dying from a variety of cancer and other diseases over specific time frames. Because age, sex, race and smoking status are so important in determining your chances, the charts let you account for these factors. While there are other factors not accounted for here that make an important difference in your risk (e.g. family history of many diseases, obesity, excessive alcohol consumption, a variety of occupational exposures, etc.), the numbers from the charts will get you into the right ballpark.

This is what they return for me.

I have already had bilateral breast cancer, but it was caught at Stage 1 and treated (apparently successfully) in 2015.

The NCI’s statistics show that I have a 76% chance of living past age 84. I am normal weight, blood pressure under 120/75 and work out every day. The odds of living past age 84 are higher than I expected. (If cancer doesn’t return – my nonsmoking mother died of lung cancer at age 72. But her older sister lived to age 92.) Higher education and higher net worth are not considered in this model but they also correlate with longer life expectancy.

Many METARs are senior age so it might be worthwhile to look at this.

Wendy