Thank you, @fish13 ! Now I can delete the draft I’ve been working on.

World-class management, indeed!

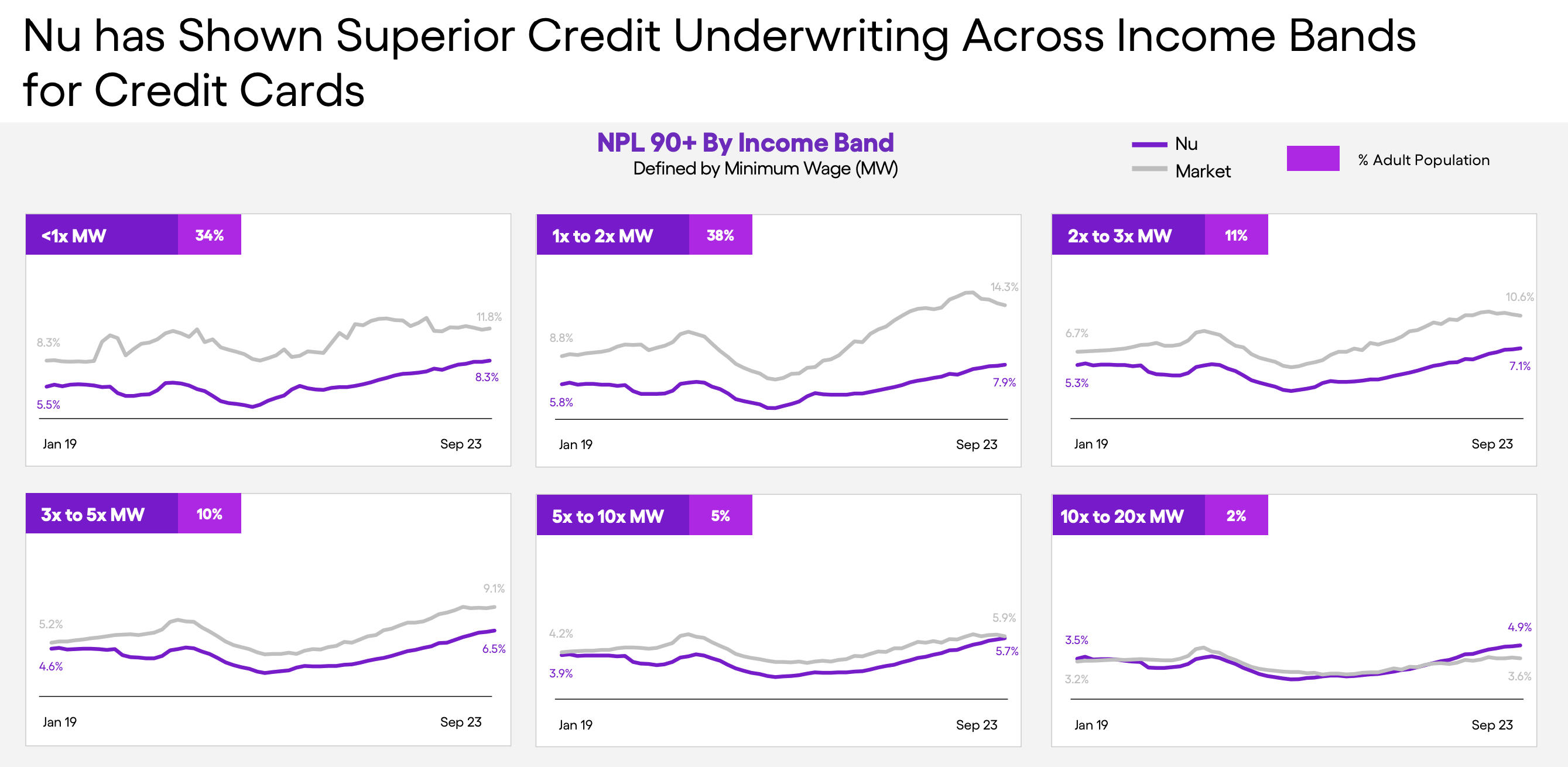

For those who may never have watched an interview with CEO David Vélez, this Goldman Sachs interview from a month ago (20 min) spends some time at the beginning talking about the macro in Brazil and making your exact point on how they have managed to succeed despite it all.

The stories in the WaPo article are heartbreaking, but my first thought was that I have met many versions of each of those women here in the US, and the systemic problems here (as there) are why both governments are trying to deal with it.

It was also notable to me that, of the three examples in the article, all were women, two of them were teachers, one was a single mom who got in trouble when the father of the child stopped paying, one was fully employed and her employer ran out of money and stopped paying her, and one got ripped off by a friend who went on a spree with her card.

Before those events, all were making payments, despite the high rate (which the article says is more like 190%), and it was the missed payments that spikes the rate to over 400%.

Most borrowers here don’t pay such high rates. It’s when they miss a payment that they get charged the astronomical APRs. By law, a lender cannot charge those rates for more than 30 days before offering borrowers the opportunity to parcel out payments. But the average rate in such cases is still more than 190 percent, according to the Central Bank.

Yes, all those rates are still incredibly high, but the macro is also way out of whack. Brazil obviously needs a Consumer Finance Protection Bureau, like we have; a program to forgive educational debt, as our government is trying to do; and more social support for single moms.

Bottom line, I don’t see that $NU is contributing to the problem. $NU was helping Ms. Chaves to get her education until her employer hit the bad macro and stopped paying her. And, again, I’ve met women in every one of those circumstances right here in the US in every state I’ve lived in (which is 8).

It’s totally possible I’m wrong. But if David Vélez turns out to be an unethical CEO who is gouging his customers–or even turning a blind eye, it will be my most catastrophic failure of judgment of a person ever.

That doesn’t mean failure of the company is impossible. He’s said that in interviews. I forget which one, but he responded to the question of the biggest mistake he saw CEO’s making, he said something like, “Thinking they have arrived.”

JabbokRiver

Long $NU 20.36%