I know this is a controversial stock for this board. For those that don’t know, Robinhood is the stock trading app that’s popular with Millennials and Generation-Z. Many like to associate it with the Reddit Wall Street Best cohort. They have 22.5 million accounts which I think is impressive when one considers that Fidelity only has 26 million retail accounts.

Yes, Robinhood is massively unprofitable, and many question if the crypto portion of their business is sustainable, which is where they make most of their money. On the other hand, they have brought trading to a whole new generation, made it affordable, and have helped change the game when it comes to retail investing. I don’t own the stock, but they just posted their first ER as a public company it’s now on my watch list. I like the trajectory of this business and think it’s possible they can scale significantly to over 100 million accounts globally, similar to the success that Netflix has had.

Here is the press release if you’re interested:

https://s28.q4cdn.com/948876185/files/doc_financials/2021/q2…

There are some impressive numbers here:

- Total revenue increased 131% to $565 million in the second quarter

- Transaction-based revenue increased 141% to $451 million

- Cumulative funded accounts increase 130% to 22.5 million

Also impressive

- Net loss was $502 million (ouch, they state that part of this is from a one-time $1 billion charge for stock-based compensation related to the IPO.)

But what I found even more interesting was the Robinhood earnings breakdown that Jason Calacanis did on his latest podcast. Jason is a well-known angel investor and Robinhood is one of his investments. What I thought was great about this was hearing how a successful angel thinks about investing. I think this is a great listen, even if you’re not a believer in Robinhood but want to get insight into how professional venture investors think.

https://podcasts.apple.com/us/podcast/this-week-in-startups/…

10 Likes

Hello all. This is my first post here. I appreciate the constructive, analytical discussions this board fosters. I have learned a great deal from all of you.

GolfCaddy4PLynch, thank you for your write up (and so many other write ups). I agree with you those numbers look good. Robinhood has been an innovative company. It is the reason why commission-free trading is so common these days (regardless of whether that is actually a good thing). It has also helped make trading popular among a new generation.

There is, however, one number that worries me–the average account size of a Robinhood user. Estimates are that the average account holds only approximately $4,500 (https://www.barrons.com/articles/robinhood-ipo-stock-value-5…). What concerns me about Robinhood is that they are seeing massive revenue growth predominantly from immature investors who might move to other platforms as they become more sophisticated (read: more valuable) investors. All that said, I am speculating about the potential churn.

7 Likes

Hi StocksandStouts,

The median age of a Robinhood user is 31.

The median amount of money in a 401K for 25- to 34-year-olds is $10,402.

Given Robinhood doesn’t support 401Ks (correct me if I am wrong about it) and this is just a cash trading account for the average Joe, I think it’s fantastic that people have saved even that much at the age. And those balances will grow over time, at least for the cohort that saves and invests well. Which will be a significant portion of them. The all-digital approach means they have much lower per-user operating costs than a full-service operator like Fidelity.

BTW: The full chart for 401K balances by age is here.

https://www.businessinsider.com/personal-finance/average-401…

I don’t think churn is the issue, competition is. Coinbase, the Square Cash App, SoFi, and a multitude of other financial apps are all competing for the same user. In my opinion, Robinhood has a fantastic brand name that is synonymous with free stock trading and is who I would consider the leader in the youth trading space. As long as they keep innovating, like they have been, offering new services like pre-IPO investment access I believe they will thrive.

Globally the retail investment space is a huge market and there is room for them to easily grow to 50 or 100 million accounts in a few years, maybe faster. Keep in mind people will have multiple accounts, I have a Robinhood account with almost 4K in it, ironically.

Thanks,

GC4P

1 Like

I won’t touch Robin Hood stock for three main reasons:

-

Payment for order flow is controversial and it’s subject to potential regulatory risk.

-

Robin Hood damaged its reputatoin during the GameStop squeeze. It lost some customers and will likely reduce future potential customers. Even if it still manage to grow its revenue, if the growt rate is slower than expected during IPO, there’ll be headwind for stock price.

-

Robin Hood is on the side of Market Makers not retailers. As a result, there are to opposing forces : market makers vs retailers fighting for the up and down of the stock price. The stock will be volatile for the medium term and is likely not going anywhere. I predict Robin Hood stock will be just a twin version of GameStop stock.

"Robinhood has severely damaged its brand. More than half (56%) of Robinhood account holders are considering leaving the platform as a result of the fiasco. Forty percent of Robinhood investors say they aren’t considering it, and 4% say they’ve already left the platform as a result of its stock limiting. It looks like Robinhood is learning the lesson Warren Buffett preached for years: “It takes 20 years to build a reputation and five minutes to ruin it.” - Fortune.com

6 Likes

- Regarding the payment for order flow, from Robinhood earnings call:

Q: What’s next for Robinhood, if PFOF is or payment for order flow is regulated, what can you do?

A: payment for order flow is regulated already. It’s been primarily focused on disclosures. And we do provide all the required disclosures and we do our best to explain how we make money and what payment for order flow is, it’s often misunderstood, component of our business and so appreciate the question.

- “It lost some customers because of GameStop scandal”

But they added 4.5 millon new customers in Q2. That’s 20% QoQ.

And what’s interesting about Robinhood:

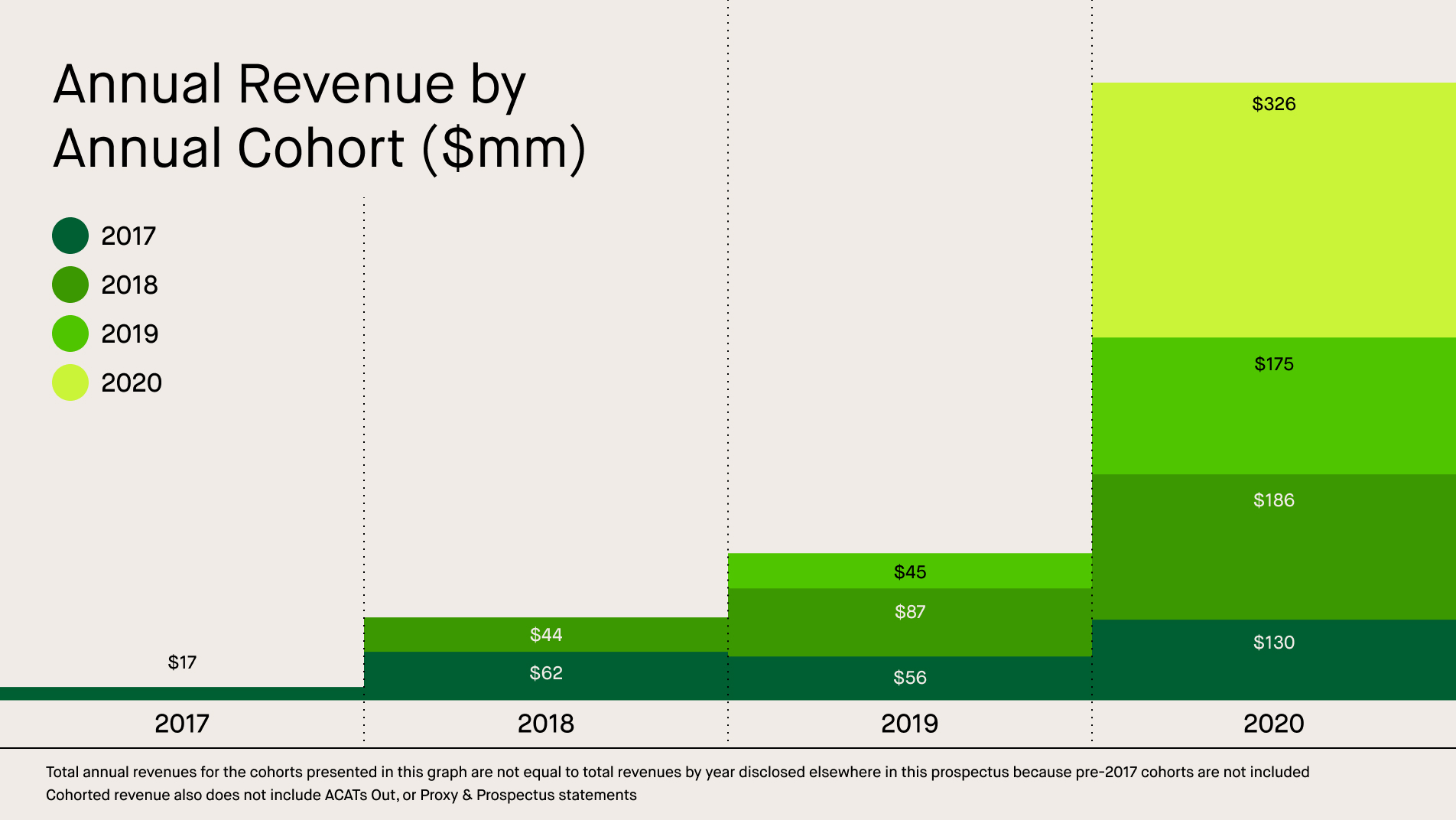

The revenue growth from 2017 and 2018 cohorts corresponds to 200% DBNER. For 209 cohort it corresponds to 388% DBNER.

And here is a chart with Cumulative Net Deposits by Annual Cohort:

https://www.sec.gov/Archives/edgar/data/1783879/000162828021…

As wee see, it does grow as well.

3 Likes

This is what I was warning about. It’s not about now. It’s about the uncertainty of the future.

Banning PFOF is on the table. It’s a possibility. It probably won’t happen because so many brokers use it but it’s a worry hanging overhead.

https://www.cnbc.com/2021/08/30/robinhood-tanks-after-sec-ch…

{kind=link}

{kind=link}