Performance recap

- 2021: -36%

- 2022: -76% (Found Saul’s amazing board Jan 2022, started this style of investing in May 2022)

- 2023: +80%

- 2024: +104%

- 2025 through Feb: +17%

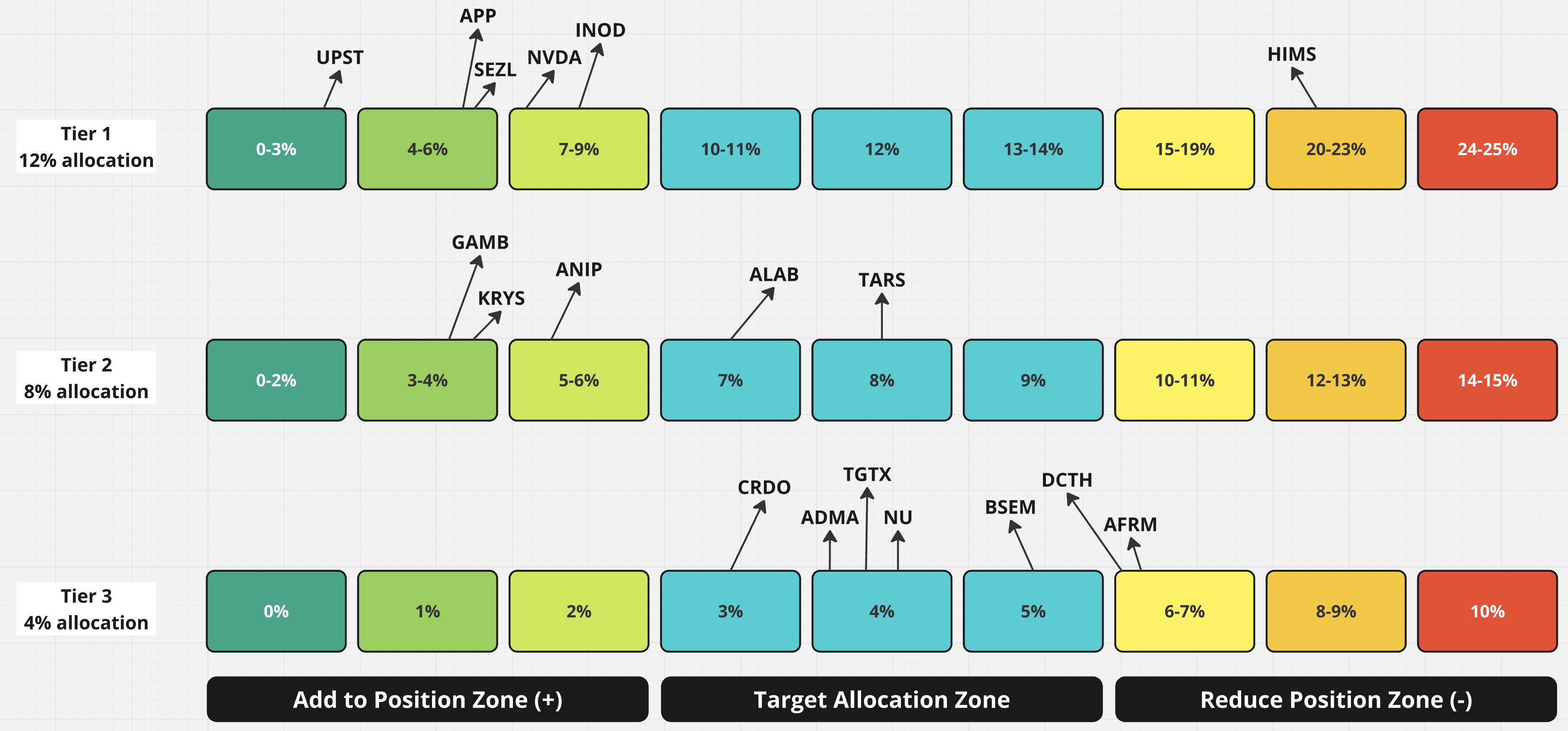

Current portfolio holdings:

- $HIMS 22%

- $TARS 8%

- $INOD 8%

- $ALAB 7%

- $NVDA 7%

- $SEZL 6%

- $APP 6%

- $AFRM 6%

- $DCTH 6%

- $BSEM 5%

- $ANIP 5%

- $KRYS 4%

- $TGTX 4%

- $TQQQ 4%

- $NU 4%

- $GAMB 4%

- $ADMA 4%

- $CRDO 3%

- $UPST 3%

Portfolio is currently 116% long.

Changes this month

- New Positions: GAMB UPST

- Bumped ALAB TARS HIMS APP

My methodology current scores:

A visual representation of my current portfolio by Tiers:

Another view plotting my quality against valuation:

Why I own what I own:

- HIMS - 22%

- HIMS had really good earnings and incredible guide up. Just unfortunate that this stock trades like a meme stock.

- But the GLP1 story is still intact. They have adjusted for semi-glutide shortage ending and even without GLP1 their organic growth is north of 40%. They are going to get into menopause related medication and treatments soon, that’s a big business. And their legacy business of hair loss and ED is still growing very well. If tele-health is the future, I see no reason why HIMS can’t be the face of it.

- All this to say, if growth stays intact for another 2-3 years, the improving profitability margins are going to make this business look very very cheap.

- ALAB - 7%

- ALAB had really good earnings. Just what I wanted to see. Not worried about the price action as the numbers should win out at the end. I added to my position during this pullback.

- If they execute, 100% revenue growth over the next 12 months should be achievable. And why would you not own a business that is growing at potentially 100% with 40%+ margins. Doesn’t happen very often in the stock market. So I am planning to ride the wave till I see material growth deterioration.

- NVDA - 7%

- NVDA had ok earnings. Beat on both top and bottom line but the raises are shrinking every quarter. They still are pointing to 60% growth and knowing how they raise, it might end up around 80% ntm sales growth. So I see no reason to lighten this position yet.

- I think this whole tornado of DeepSeek information has created a buying opportunity in Nvidia. It still has the best in class chips product with newer models hitting the market. I still feel Nvidia can create a iPhone like cycle for a few years where all the hyper scalers are forced to upgrade hardware to keep up with the fight for first place in this AI race

- TARS - 8%

- TARS reported really good results but didn’t make any more inroads towards profitability. That is a concern so I will keep my position sizing right here and only increase if I see them getting fcf+.

- Their primary product XDEMVY kills mites in your eye lashes. Only FDA approved product and is just beginning to do commercial launch.

- Since it’s early commercialization stage, I expect them to grow rapidly in the next 12 to 24 months. They are close to getting to FCF+ and I feel the current high multiples will hold if they can get there soon.

- DCTH - 6%

- Delcath Systems. is an interventional oncology company focused on the treatment of primary and metastatic cancers of the liver.

- They have two products in this space and are at an early stages of commercialization.

- Analysts expect them to deliver 110%+ NTM revenue and the FCF numbers should turn position in the next 12 months. So if they deliver, I see a lot of potential in this name in the next 12 to 24 months.

- BSEM - 5%

- As expected, LCD got pushed back to mid-april now, which means q1 results will have full medicare coverage.

- They have the better product and the clinical trials should show that. And the nasdaq listing should help which should be out over the next couple of months

- AFRM - 6%

- AFRM had great earnings results. And took a big step towards higher profitability. So I am happy with the report and will continue to add if there is significant pullback.

- Affirm is trying to capture a big piece of the growing “buy now pay later” market. It’s a steady eddy in my portfolio and I still feel it is undervalued. I will keep this a mid size on my account for now and let it do it’s thing.

- INOD - 8%

- INOD reported great results but the stock is extremely volatile. I expect to see a bumpy ride up for this one over the next 3 months before next earnings.

- This is a play on AI and LLM adoption curve. Initially introduced by wpr101 and then later I saw it in Purst04’s portfolio. Ran the numbers and it did quite well on my methodology quality score. The stock has been consolidating since last quarter’s blowout earnings. The fact they are profitable and probably has room to optimize, got me excited and I am in with a starter position.

- SEZL - 6%

- SEZL absolutely crushed earnings. I expect this to pick up steam once growth stocks turn up.

- The numbers they are putting up are quite impressive. Do intend to add to this one if there is a significant pullback. They are in the same space as Affirm, buy now pay later space. I have a starter position based on just high revenue growth and the fact they are already FCF+

- APP - 6%

- APP had good earnings but got caught in 2 coordinated short attacks. I added to my position. I feel the same way as many here on the board. These short reports throw everything and hope one of them sticks. I have really not seen anything from the business end that warrants this kind of sell off. I still think they have room to run. Although highly profitable, they are still growing at a rapid rate.

- TGTX - 4%

- TG Therapeutics, Inc., focuses on the acquisition, development, and commercialization of novel treatments for B-cell mediated diseases. Successful launch of their flagship drug BRIUMVI, for patients with relapsing forms of multiple sclerosis. Robust pipeline in place - new indications for BRIUMVI and allogeneic off-the-shelf CD19 CAR-T for autoimmune diseases. Hyper-growth still intact with high margins and very healthy free cash flow.

- NU - 4%

- I thought NU’s earnings were descent given the headwinds around exchange rates. Lots have been covered about this great business in this forum. So I am not going to get into details.

- Leader in LATAM Banking. Very well run business. Market provided an opportunity to get in and I took advantage of the situation. I expect a steady eddy out of this one.

- CRDO -3%

- Another business in the AI/LLM optimization play. Similar offerings to ALAB but their recent quarter results were stellar. Scored very high in my methodology and with the DeepSeek new opportunity, I got in. Hoping to see great execution from this business going forward.

- ANIP - 5%

- ANIP reported fantastic results. Their guide up was also very impressive. Thsi puts them back on 405 growth curve. I will add to my position if given the opportunity.

- I have owned this pharmaceutical business with success in Q4 2023. Then growth slowed and I exited luckily in time. Now growth is back with a potential of 40% revenue growth in the next 12 months. Also, the stock price has been coiling for over 9 months. Very AFRM like chart. So if they execute I expect a nice pop for a few quarters. They are currently at 10% FCF margin with room for improvement

- TQQQ - 4%

- I am trying to see if I can make TQQQ as part of my long term portfolio. I have read enough papers to know this is a high risk strategy but it works. You just have to have an appetite for 70-90% drawdowns. I am not going to make this more than 10% of my portfolio but this is a grand experiment. For now, of the 17 positions I own, it is already sitting at number 12 as per performance. If it hangs out in the top half of my holdings in terms of performance, I will gladly keep it.

- KRYS - 4%

- KRYS reported good revenue growth but made significant progress towards more profitability. So I am happy with the results.

- New entry for me. Scored extremely well as per methodology. They are a player in the genetic and rare diseases category. The company’s pipeline is impressive and their commercialization has seen good success.I expect Krystal Biotech to diversify into many drugs and have a long run. Obviously, execution will be key.

- It’s not cheap but it’s highly profitable and is growing rapidly. So I am in with a starter position.

- ADMA - 4%

- ADMA Biologics is uniquely positioned to capture a large portion of the IG market

- The big issue is LTM revenue growth is 63% and ntm prediction by analysts is 14%. Huge disconnect.

- Well the CEO came out during the JP Morgan conference and pretty much told us that they are taking the same conservative approach to guidance as last year. And last year they beat analyst expectations by 30%.

- Another important point is ADMA has hit a 40% FCF two quarters ago. If that is their high number and they can trend more towards a 30/40% FCF, then the market will give a higher multiple to the business.

- GAMB (new position) 4%

- Gambling showed up on my methodology with a high score and even with this impressive run, they look cheap to me. So I started a starter position on this one. More than the growth what impressed me was their profitability. I am still learning about this business and will share more over the next reports.

- UPST (new position) 3%

- I have owned UPST in the past. All the way from 80 to 400 to 60! Not fun memories. But I took a second look as this business showed up with good score on my methodology. And I feel UPST has turned the corner or at least that’s what I am betting on. Growth is clearly back and it has started to catch the analysts on the wrong foot. That’s always what I want to see in my businesses. So hoping for an extended run this time around.

Wrapping Up

February was a split month. The first half of the month saw rapid rise in growth stocks and the second half turned out to be brutal. I was up almost 40% at one point but ended the month around 17%. Given indexes are pretty flat, will take these results any day. But I am very highly exposed to the markets now. Any major pullback from here and that would have a significant impact. But I believe I own the best businesses possible and once the markets turn up, these businesses should do just fine. Earnings season so far has been quite favorable and hence I haven’t sold any position yet. Hoping growth stocks catch a bid in March. Let’s see how things unfold.

Always a privilege to post on this board. Thank you for reading. Cheers!