Performance recap

- 2021: -36%

- 2022: -76% (Found Saul’s amazing board Jan 2022, started this style May 2022)

- 2023: +80%

- 2024: +104%

- 2025 through March: -6%

Current portfolio holdings:

- HIMS 16%

- TARS 10%

- TQQQ 9%

- INOD 8%

- NVDA 7%

- SEZL 7%

- ALAB 7%

- AFRM 7%

- UPST 6%

- DCTH 6%

- GAMB 6%

- ANIP 5%

- APP 5%

- KRYS 5%

- ADMA 5%

- CRDO 5%

- RDDT 4%

- MYO 4%

- BSEM 4%

- BYRN 4%

Portfolio is currently 130% long and has 20 positions.

Changes this month

- New Positions: RDDT BYRN, MYO

- Have been on my watchlist for a while and with this huge discount on these names, I got starter positions going.

- Sold: NU, TGTX

- NU - I don’t understand this business very well. Banks are not my cup of tea. It looks really cheap but I have a hard time evaluating it. Add to that the LATAM space and I am totally out of water. So I moved the proceeds to the new positions I opened this month

- TGTX - My valuation model says it’s overvalued now. So I trimmed and then sold out completely. I still like the business but will wait for a better entry. I also needed the cash to flip to MYO, which I bought today.

- Bumped: CRDO, INOD, HIMS, UPST, GAMB, SEZL, AFRM

- With the markets providing an opportunity, all bumps are in accordance to trying to get these names to my allocation levels.

My methodology current scores: (all green bars I own)

A visual representation of my current portfolio by Tiers:

Here are a few updated one pagers for my businesses.

Sorry I did not have time to create one for each of the businesses I own. One note on valuation - I have boiled it down to a formula now. Let’s see how this works. But for valuation I take the ntm fcf and use half of my methodology score as multiple. That’s my very basic valuation model. Ideally, I like to see the number for next 12 months north of 100%, that way if I am wrong I still might be able to get out unscratched. Also, if it is able to get 100% returns in the next 3 years instead of 1, that would be very satisfactory. So basically, these are the guardrails/padding built in for losing less capital.

Why I own what I own:

- HIMS - 16%

- HIMS gave away all it’s early year gains and then some over March. It’s back to levels, I consider very attractive.

- Markets are saying they don’t believe in what HIMS is guiding for. So this is going to come down to the next earnings release - May 12. If they even re-iterate their guidance, I think the stock starts it’s upward trajectory but if they raise guidance again, we are back to meme stock territory. Nothing to do but wait an watch for the time being.

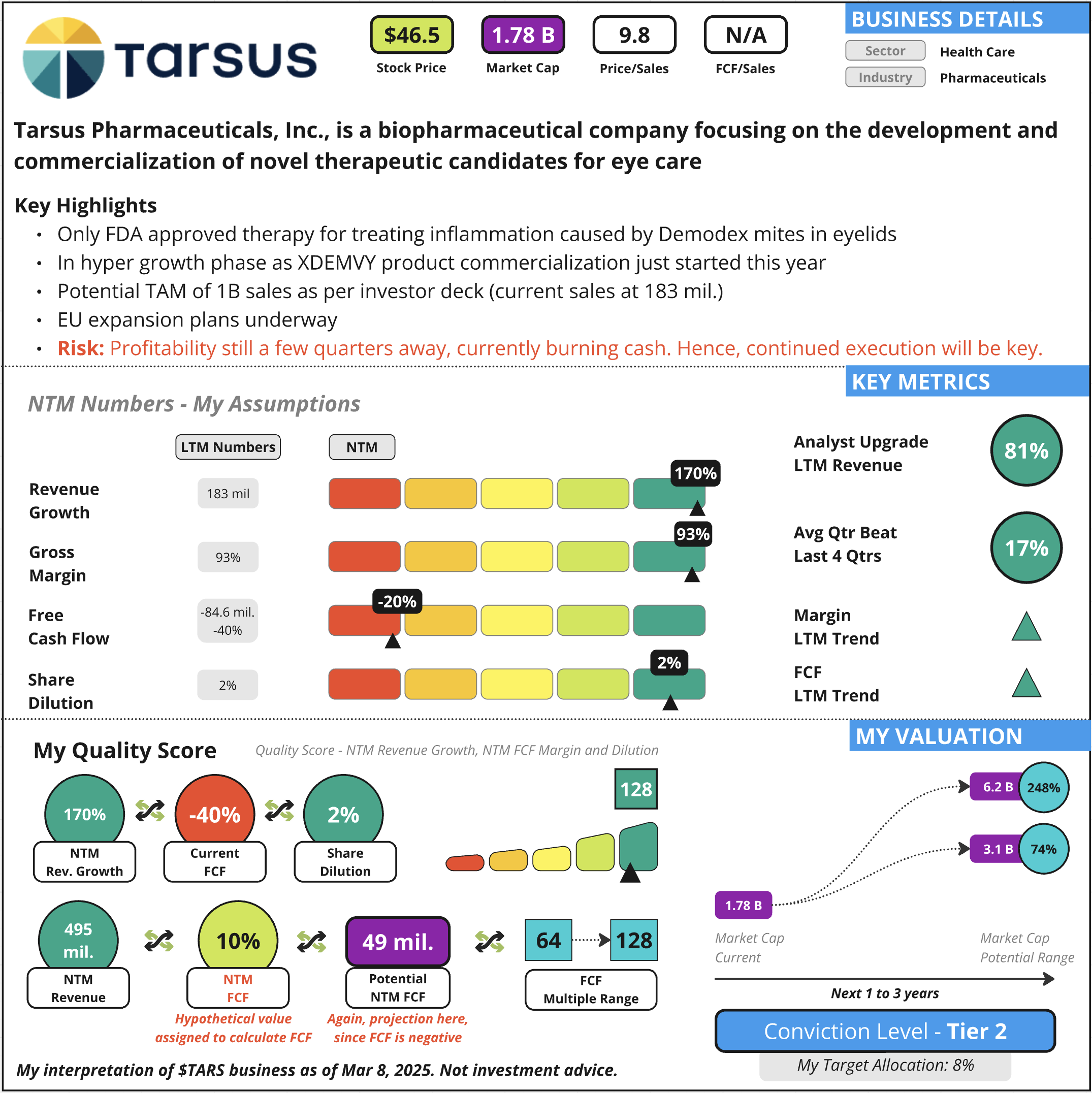

- TARS - 10%

- TARS have been trending up since it reported nice quarterly results at the end of Feb. In this downtrending choppy market, it had a 15%+ month. So I believe once this market turns, TARS has the potential to be a leader. Let’s see how April unfolds.

- TQQQ 9%

- I just wanted to address this once. TQQQ is a leverage play for me. It’s a tool to increase alpha when markets pull back. I have a well established strategy and I just simple execute it when markets go on extended drawdowns. I usually liquidate TQQQ once Nasdaq hits all time high. But this time around I might start to make it part of core position. I will just report numbers going forward but won’t add commentary as this is out of bounds for this board.

- INOD - 8%

- I think Innodata’s customer concentration risk is very real. The quicker they show signs of revenue distribution across the big players in the AI space, the more upside it will have.

- So far the execution has been pretty flawless and among the other data/AI plays, this one is relatively cheaper. Also has been holding up better than the other AI names, so I am hopeful that this bounces harder once the tide turns.

- NVDA - 7%

- NVDA is almost back to the price it was four earnings ago. So obviously, the numbers look much more attractive. It’s definitely slowing down but the fears of NVDA being cyclical and the best earnings are in for this cycle - is overblown imo.

- NVDA still has the best in class chips with newer models hitting the market. I still feel Nvidia can create a iPhone like cycle for a few years where all the hyper scalers are forced to upgrade hardware to keep up with the fight for first place in this AI race.

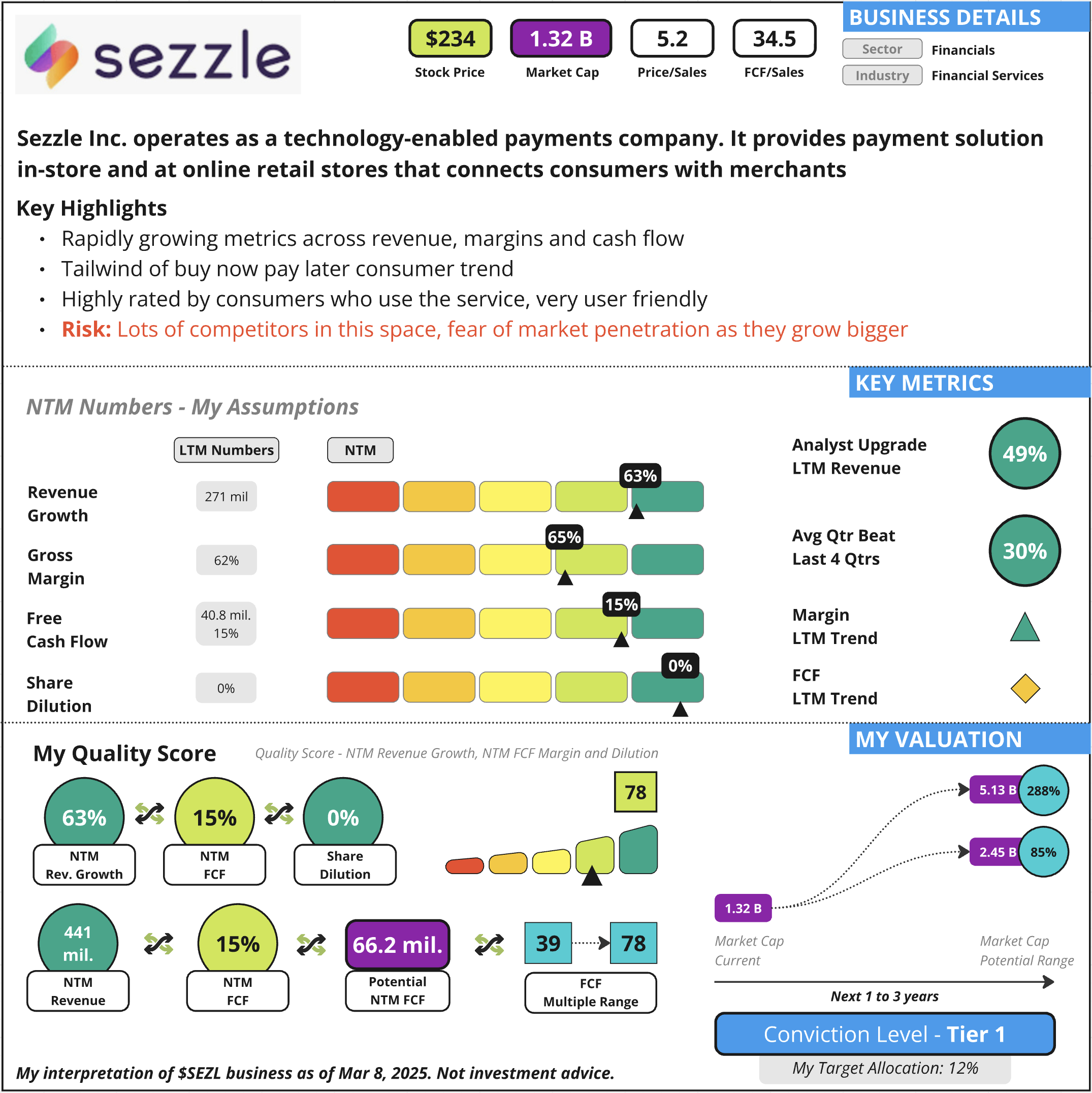

- SEZL - 7%

- SEZL absolutely crushed earnings. It announced a 6 to 1 split and a 50 million dollar buy back program. I think Sezzle is quite undervalued given the growth and cash flow it is about to generate in the next 12 months. If this market pull back does not affect the wallet of the customers too much, I expect Sezzle to do really well based on business momentum and execution.

- ALAB - 7%

- ALAB has lost 60% of it’s value since all time high yet trailing p/s is 24 and p/fcf is 94. I feel like this is what the investor sees and with the AI stocks getting killed, ALAB has become the poster child of excess valuation. Also, I know the weekly chart looks like a vertical rocket launch. So it was going to come back to earth for sure. But now with 100% ntm revenue growth potential and FCF at around 30%, this should start to see a floor and be a good investment for the long run. Execution so far has not at all been an issue.

- AFRM - 7%

- AFRM had great earnings results. And took a big step towards higher profitability. So I am happy with the report and will continue to add if there is significant pullback. If Affirm can solidify the FCF around this 30% mark, I think it should get a re-rating over the next few quarterly results.

- UPST 6%

- UPST had a great quarter and did a gap up to almost $90 a share. Due to march madness, it is down to half that value now. I feel Upstart has turned the corner and is starting to accelerate revenue growth. The guidance this quarter was extremely impressive as it raised yearly guide by 20%. That’s rare. So, I continue to build my position in this business.

- DCTH - 6%

- I was pleased with Delcath Systems results this quarter. The beat revenue expectations by 10% and reduced their FCF negative gap. This business should turn FCF+ in the next two quarters based on the trend so far. That would be a good tailwind for DCTH as this is still expected to grow over 100%+ in the next 12 months. Also, there was no additional dilution which has been a concern previously.

- GAMB - 6%

- Gambling showed up on my methodology with a high score and even with this impressive run, they look cheap to me. So I started a starter position on this one. More than the growth what impressed me was their profitability. What I like about this business is growth is accelerating and analysts have started to raise guidance. Still a p/s under 4 so lots of room to run if it executes.

- ANIP - 5%

- ANIP reported fantastic results and the stock didn’t disappoint. In a downtrending market, ANIP did 10%+ performance in March. Their guide up was also very impressive. This puts them back on 40% growth curve. I will add to my position if given the opportunity.

- APP - 5%

- APP had good earnings but got caught in 2 coordinated short attacks. I added to my position. I feel the same way as many here on the board. These short reports throw everything and hope one of them sticks. I have really not seen anything from the business end that warrants this kind of sell off. I still think they have room to run. Although highly profitable, they are still growing at a rapid rate.

- KRYS - 5%

- KRYS reported good revenue growth but made significant progress towards more profitability. So I am happy with the results. They are a player in the genetic and rare diseases category. The company’s pipeline is impressive and their commercialization has seen good success.

- ADMA - 5%

- ADMA Biologics is uniquely positioned to capture a large portion of the IG market. The big issue is LTM revenue growth is 63% and ntm prediction by analysts is 15%. Huge disconnect.

- Well the CEO came out during the JP Morgan conference and pretty much told us that they are taking the same conservative approach to guidance as last year. And last year they beat analyst expectations by 30%. I will be closely following their next quarterly results for guidance. They need to beat and raise by 10% or analysts will start to sound right about this business.

- Another important point is ADMA has hit a 40% FCF two quarters ago. If that is their high number and they can trend more towards a 30/40% FCF, then the market will give a higher multiple to the business.

- CRDO -5%

- Another business in the AI/LLM optimization play. Similar offerings to ALAB but their recent quarter results were stellar. Scored very high in my methodology and with the DeepSeek new opportunity, I got in. Hoping to see great execution from this business going forward.

- The huge concentration in one client is a risk. Since they are growing at such a fast pace, I am giving them a little rope. I will be closely following their US client base - would like to see them make some headwind in the next quarter.

- RDDT - 4% (new position)

- Like a lot of members of this board, I have been following Reddit for a while now. It has fantastic numbers and it finally gave a good entry. I was surprised by the steepness of it’s fall, similar to ALAB. But it’s a great business at a discount now. The growth is almost 50%+ with 30%+ analyst expectation raise and closing in on 20% FCF. These are elite numbers, so I took a starter position.

- MYO - 4% (new position)

- Myomo is a medical robotics company that produces myoelectric orthotics for people with neuromuscular disorders. They got Medicare coverage and just started to hit the S curve launch in US. Lots of room to grow in US alone and International expansion is next. Their TAM may be limited but the company is executing very well and have a good growth trajectory for the next 24 months. Their dilution numbers should come down dramatically now that they are profitable and growing revenue at a fast clip.

- What really got me to pull the trigger on this was their guide up this quarter. They guided to 20% ntm revenue growth. That is a rare feet for a business - usually these kind of raises ends up being a multi quarter momentum play. So I am in with a starter position.

- BSEM - 4%

- Very poor price action from BioStem. Gave back all its gains and now is in red territory for me. I am just waiting for it’s earnings release tomorrow. If I don’t get more clarity or pipeline, LCD and Nasdaq listing, I am probably going to sell out. Doesn’t matter how good the numbers look, the question marks seem to be piling up on this business.

- BYRN - 4% (new position)

- Byrna sells less lethal weapons and is a small fish in the AXON space. The numbers are promising and in this downtrend the stock has been beaten up a lot. It scored an impressive 82 per my methodology.

- Hard to find businesses that are quite profitable and growing north of 50%+ with less than a 5 p/s handle. So I am in with a starter position

Wrapping Up

Boy! am I glad March is over. That was brutal. Portfolio lost about 23% and moved from +17% to -6% for the year. I am not happy with the amount of leverage I have currently. I would like to get it down between 15% and 20% throughout this market drawdown. I am hoping by mid-april markets get a hang of what these tariffs might look like and once the uncertainty is removed, growth stocks should bounce hard. Most of them are around critical levels of historical support and are very extended to the downside. The only reason my portfolio is not down another 10 or 15% is because throughout this downturn biotech related stocks have really held up. And since I own quite a few names, that allowed for some cushion on the downside. I am getting more comfortable with holding 15 to 20 businesses. The tiering system allows for exposure control and has helped in risk management as well. Though I really would like to get down to 10 stocks like most of the members on this board. Still a work in progress.

It’s a privilege to post on this board. Thanks for reading. Cheers!