In selecting the next ticker to enter there may be competing tickers with comparable financials residing in different sectors. When traditional hypergrowth data does not favor one over the other, the investor might check the current market trends of the sectors and select the sector seemingly favored by the market I took a look this week at the following sectors: Robotics/AI, Pharma/Bio, Fin Tech, Cloud and Clean Energy and used BOTX, FINX, ARKG,PBW and SKYY as indicators.

On a two-year chart, Cloud ran ahead of QQQ and FINX ran quite consistent with QQQ, the other three dramatically underperformed QQQ.

I recognize this is outside Saul’s knowledge base, but would any others here consider sector performance in ticker selection? If so what indexes or ETF’s do you use as indicators?

So, knee jerk answer, or off the cuff as you might say…

The main reason that funds were OT in Sauldom is that they force you into diversification, and in most of these cases it would be appropriate to say di-worseification.

A fund is kinda forced to throw a wide net so you get the get the good and the bad in that one basket. Let’s say you wanted UPST in a fund, but you would probably also get Fanny and Freddy if you were looking at financial lenders. I would never want to own the latter two, so I wouldn’t want to own the fund.

Now, to you point, maybe a fund is “in vogue” at the moment and everyone is buying ALL AI ALL THE TIME. The problem there is that you have no idea when that mania is going to crash. Now you are more timing the market than anything else. There is no way you can research all the companies in a fund, and there is no way you can influence what they own…(well, I have no way to influence that).. Then, you have to deal with all the costs of funds and some of the newest hottest ones will take well over 2-3% of your money. (Especially if they are actively managed.)

For all those reasons they are not Sauldom investments. They break just about every rule that Saul wrote up.

There are probably other boards to talk about things like the best funds at any given time. But, I would humbly suggest to everyone that this is not the board for that discussion.

My post did not suggest investing in a fund. My post only questioned if anyone here had used sector well defined cyclical performance as a tie breaker in choosing between two tickers with similar “Saul” metrics, whose homes were in different sectors.

Hi Gray - now that you have clarified the point about the sector instruments - not as investments but as benchmarks, then - in a sense I do think about hot sectors (AI, Cybersecurity and Fintech) and cooling sectors (AdTech) but I don’t typically use sector ETFs to do it, I usually notice it and look at it through the performance bundle of a number of individual companies that I might follow. Since I hold a less concentrated portfolio with multiple players from the same sector that feels as easy to do as anything. I also do think that some sectors ETFs or indexes are not valuable in terms of representatives of the underlying sector. Pharma is a classic where strength is more driven by individual company portfolios, trial results, product launches and M&A than anything else.

Ant

I think the broader question here is how to find good growth companies, and that’s probably on topic. My suggestion: what about renaming this thread to the broader “how to find growth companies?” Saul has said he never uses screeners or the like to find companies, and I never have either. Generally we have relied on recommendations from trusted sources. But some folks around here (like @wpr101 and @ryshab) have found some very interesting companies through screeners and maybe even by utilizing AI, and perhaps considering sector dynamics, and who knows what else. Maybe they would be willing to share and discuss what they look for.

Note: Back in 2018 Saul wrote “How I pick a company to invest in,” but the world and the landscape of available companies have changed a lot since then. It’s pinned on the board’s sidebar and worth a read, but it’s probably time to update on the world as it is today.

Bear

PS - Also, remember that just asking a question isn’t likely to get as much engagement as proposing something specific. Do you have an example of a couple companies where your tiebreak method might be applied right now?

Thanks @PaulWBryant for the shoutout.

My criteria for finding growth stocks are a few different steps:

Phase 1: Awareness of a potential ticker

I scout through portfolios and suggestions brought on this board and see if any ticker is in my comfort zone for investing.

I use X or twitter to gather some new tickers I haven’t heard of, or some old tickers that is gaining mentions or traction from trusted accounts I follow

And I use a screener to find a whole bunch of businesses that show up. Usually 90% is noise. 10% I will research and maybe once a quarter I will get a couple of names that really shows promise to enter my portfolio.

Here are some of the key ingredients I use for screening.

I usually play in tech and healthcare. Sometimes communications and financials. But that’s about it. All other sectors usually screen out because of my criteria or when I do numbers analysis. All cyclicals I avoid, with rare exceptions.

I try to find businesses below 1 Billion market cap. That way there is enough room to grow. If I can’t I will try for 1-5 Bil. next. Above that I rarely get it, though there are exceptions.

I look for TTM growth rate north of 40%-30%

Look for 20% gross margins for screening but will rarely enter businesses that is below 50% actual gross margins

FCF margins I look for -50% and above. Ideally want -20% or lower, so that they are at the cusp of turning FCF+

I look for average revenue revisions up over LTM at 20% or more. This is a critical screen. I need to see analysts are wrong and playing catch up. Otherwise, mostly everything is baked into current price already.

I also sometimes screen for last quarter 3% or more revenue raise for current year. This is to ensure the business has continued momentum in surprising the market.

Phase 2: Check my core criteria set to see if numbers check out

Valuation potential to double in next 1-3 years

(My NTM FCF expectation * Methodology Score)

Quarterly Earnings trend ideally Beat & Raise or Beat

Quality to Value ratio above 200

Value (EV/GP/NTM Growth) ratio below 0.2

Then I look at a chart of Gross Margins, Revenue, FCF. I want to see all of that as a stair step up. I don’t want to see lumpiness in revenue growth, or margins all over the place or fcf very unpredictable. A stair step tells with earnings beat is a rare combination. They are pretty reliable as these businesses have done this over and over again. Very rarely will these businesses be undervalued but if they are, they are usually undervalued when they are very small. Like market cap below 1B.

Phase 3: Now I look at the business and see what they do, their products, management team, earnings calls. Check X to see if there is any deepdive. How well known these businesses are among retail.

After this, I would take a Tier 3, which is 5% position in the business. I also force rank them against my current 12 businesses. If they can’t make the top half in terms of potential, I usually will mark them for close watch but won’t take a position. The goal here is to continuously own the very best performing businesses in the market. This is probably why I have 30+ businesses churn through my portfolio. And this is also why if a business makes it over 6 months in my portfolio, they usually have good returns.

Sorry for all the jumbled up thoughts shared without much editing. Hopefully all this makes sense. Happy to expand on any particular area if there are questions. Thanks.

With my approach I do not look too much at sector performance per se, but I am looking for companies which may be benefiting from an industry tailwind. Using the current trend of AI will serve as a good example. Semiconductor stocks are over performing and valuations for them have increased. However, there is a clear catalyst for the increased valuation with massive data center growth. It is then a subjective judgement call if the sector’s valuation corresponds to the increased prospects for the industry as a whole. From my viewpoint this is a bit of a guessing game on what a sector should be valued at.

One more key point in my strategy is to have some diversification amongst sectors. Even though I believe AI is a huge trend, I do not want to own only semiconductor stocks because they end up trading in tandem. That all-in approach makes it a much stronger directional bet with increased stress when that industry crashes at some point. Like many on this board during the SaaS era, I completely missed the risk of being invested so heavily in one business model. I thought because the companies themselves were selling to a diverse set of verticals that SaaS investments were inherently diversified.

It is an encouraging sign for my portfolio when the stocks trade on different news events that are uncorrelated. For example, with some of my top holdings, HIMS is trading on GLP news, AppLovin on AppStore changes, Reddit on social media and AdTech news, and Astera Labs is trading on enthusiasm for the semiconductor sector and tariff fears. This is ideal from my perspective that the companies are not trading in tandem. Diversifying like this will help reduce both risk and variance in the portfolio. Of course sometimes growth stocks in general all go down together like earlier this year. Some would consider it un-diversified to only own growth names, however this is a risk I am willing to take with my eyes open.

I have a couple videos on my channel that go a bit more in depth on Selecting a growth stock and Stock Screeners. I’m also looking to detail my process of evaluating a new stock once I have a promising symbol from a screener or from other investors.

@flyingelephant1 for dilution, I use last 12 months “weighted average common shares outstanding - basic”. The main reason I use this part of the criteria is because I invest in a lot of unprofitable companies that are on the verge of becoming profitable. Many of these businesses prefers to raise capital from the equity markets by diluting shareholders vs. taking out debt. Hence, this levels the playing field especially for healthcare or early software businesses.

And for your second question, for EV I use current EV and my projected EV based on valuation formula (as shared above). And Gross Profit I use current LTM number. But will give a relative bump to the number if I see continued improvement on gross profit over last 4 quarters.

Do you take out conversion of preferred shares from the dilution value you use? Because a conversion is not the company raising money and/or operating expense of the company. Its a share that already exists and is converted into new shares. For example 75% of CRMD dilution in Q1 was conversion of preferred shares into common shares. I personally remove conversions from my dilution calculus because that’s not a decision the company is making and their is a set number of those shares. But I also have to account for those shares when doing valuation metrics because those share already exist.

I usually just use a number that my data provider gives me on a daily basis. It’s called “Share % change 1 Year”. For CorMedix, it was 23% and now recently after the offering it went up to 35%. But to your point, I do not do this manually looking at actual share count and sorting through different kinds of dilution. Your process is much more nuanced than what I use.

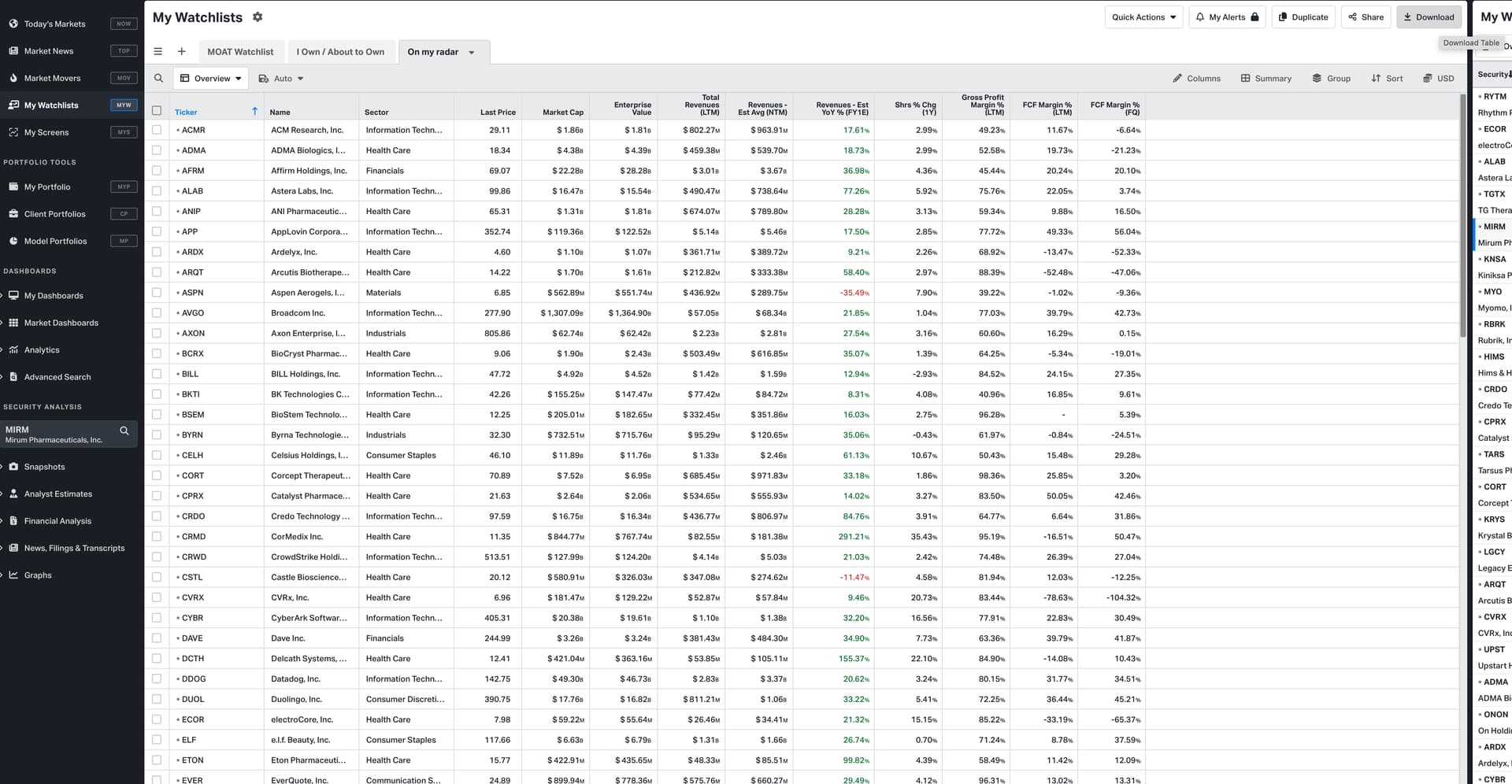

Here is a sample download from today for the data screen:

This is off-topic but how do you download that?

That looks like koyfin and koyfin doesn’t support downloads of financial or valuation metrics from my experience. Which slows me down in my metric calculations.

It’s in the “My Watchlists” section. Once you select the columns you want and save the view. On the top right, there is a download button, that downloads the data in a csv table format. Then I usually take the data to my excel data source tab. And everything flows from there.

Here you can see the download button on the top right.