I don’t know what market prices will do next.

But the omens are pretty good for buyers of Berkshire’s stock today.

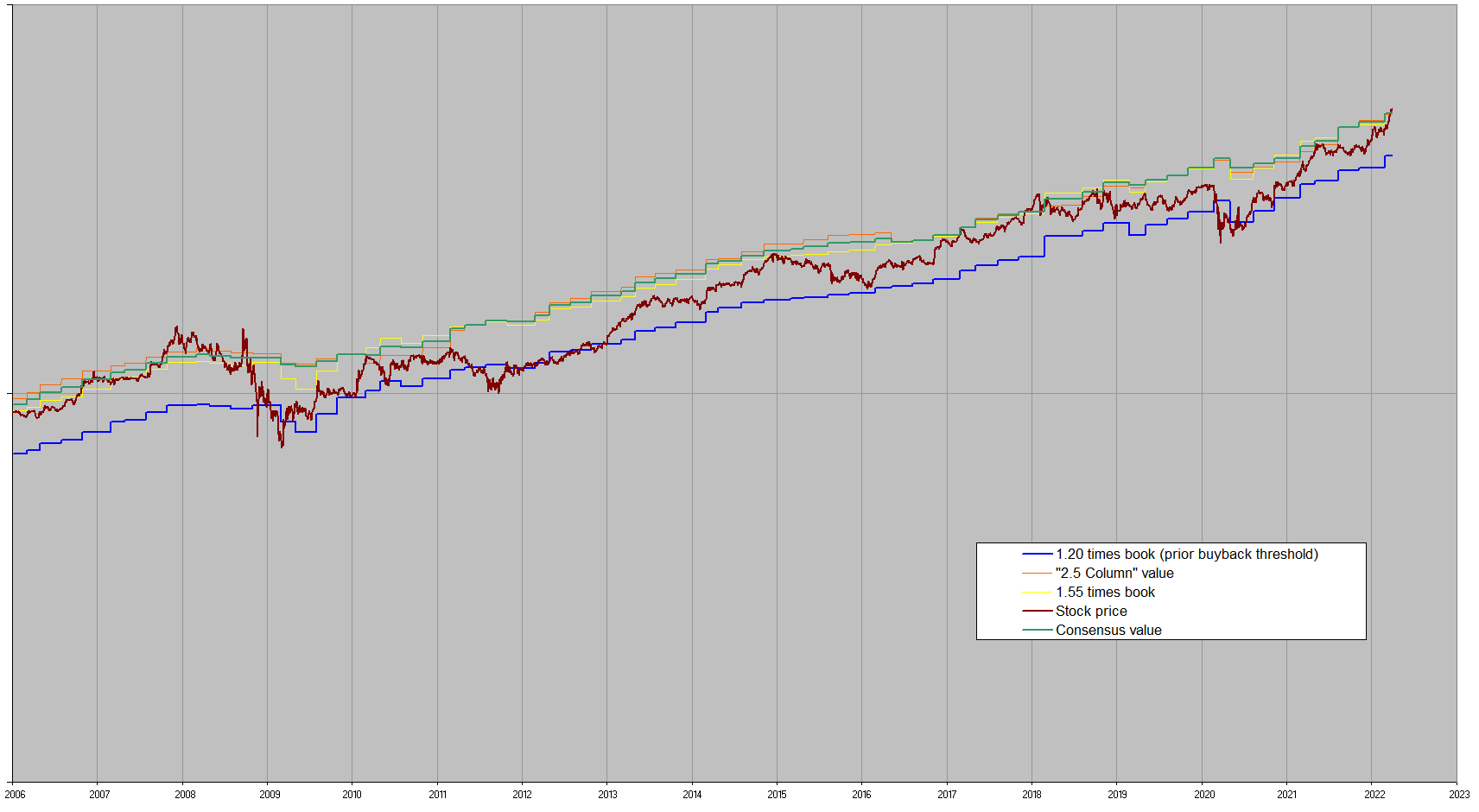

Berkshire’s valuation multiples have been much lower since the credit crunch.

Considering only the lower results since January 2008, starting from the price now of $265.80 per B ~= $398700 per share,

the average one year forward return was inflation plus 22.6%.

That’s using my own valuation metric, not price/book.

My calculations have included quite a large haircut on equities lately, so there is no obvious recent overhang of overvaluation built into the value estimate.

The same might not be true of book per share…a bit of retrenchment among the equities might have been in the cards.

I think I recall you saying that you prefer using price to peak book value per share as a valuation metric. Are you using the reported ~$230 per B for peak book/share? That would put the ratio at about 1.16x, correct?

“Do you know you per chance how much company book value declined for Berkshire is the great financial crisis from top to bottom?”

…

This post from Jim updated thru Q2 provides a great historical overview of Berkshire performance relative to several valuation factors. The performance thru the 2008/9 financial & more recent COVID crisis relative to these valuation measures is especially interesting considering our current “inflation-control” attempt and market reaction. Thanks Jim!

So looking at the chart even after the stock price had dropped 50% it was still trading at 1.2 x peak book? Or was that a written down 1.2x most recent book?

“Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria.”—Sir John Templeton

Wow, so much pessimism out there but so hard to be a contrarian here. Already added a good bit of BRK this summer, but leaning towards sitting on the sideline until Q1 2023 when maybe a Powell pause will lift all boats and spirits. Really hope we will see a lot of Q3 BRK (and AAPL) buybacks next month.

Don’t fight the Fed is right. And they are projecting multiple increases soon. One perhaps .75% in November. I’m remaining very cash heavy for this reason.

It’s likely the unknowns that are the issue, no? Will it be worse than the projected multiple increases? Can we expect more negative surprises like today’s? Even a positive surprise along the lines of “it’s still bad, just not as bad as we thought” could cause the market to rise.

{kind=link}