We’ve discussed the Social Security thing quite a bit here over the years. I think, by restating the basic facts, perhaps a better understanding of it can be had by all of us. For this post, I will use the maximum social security amounts, and will ignore inflation indexing (I think the analysis makes no difference either way, because all the numbers, including deferred numbers are indexed using the same inflation number). And it all boils down to two types of annuities.

The literal choice that people have to make beginning at age 62 is to choose to receive one of the following two options:

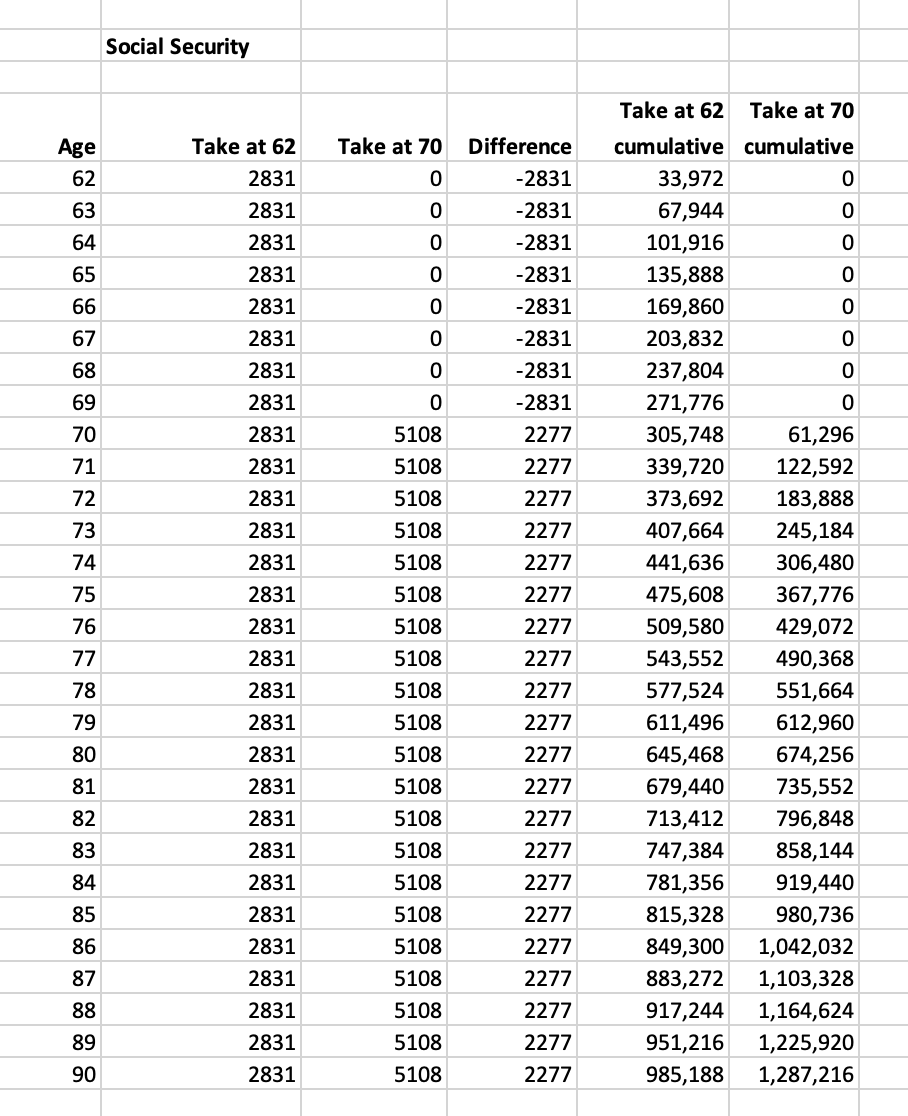

- An 8-year immediate annuity of $2,831 per month beginning at age 62.

OR - A lifetime annuity of $2,277 beginning at age 70 and ending at death.

Much of the conversation has been around “being able to spend more at age 62” by taking social security early. And with just a first order look at the numbers, that sounds like it makers sense. But does it really? I don’t think so. You need to also look at the risk-adjusted numbers. Let’s say that someone needs a minimum of $5000 a month to live in retirement (obviously everyone has some minimum number that they can use). So, if social security after age 70 can provide as much as you need to support yourself, or even provide a substantial part of it, then you can spend ALL (or most) of your saved money between age 62 and 70. First you need to cover the $2,831 that you won’t be receiving from social security, but everything else can be spent on additional “fun”.

Yes, if you die at age 80, you will have received less from social security in total by taking at age 70 instead of at age 62. However, if you took at age 62, you would have had to save a lot more to cover all the expenses after age 70. And, yes, you die with more savings, but that’s not the stated goal. The stated goal is to be able to spend more between age 62 and age 70 when you are still strong and vibrant. Even if you end up receiving less from social security, by taking at age 70, you still end up living better in retirement!

(I have to go to gym now because they close in a hour, but I may edit this some more later.)

Back from the gym. Here’s the chart I meant to add.

Priest scene part 2 (1080p HD)")