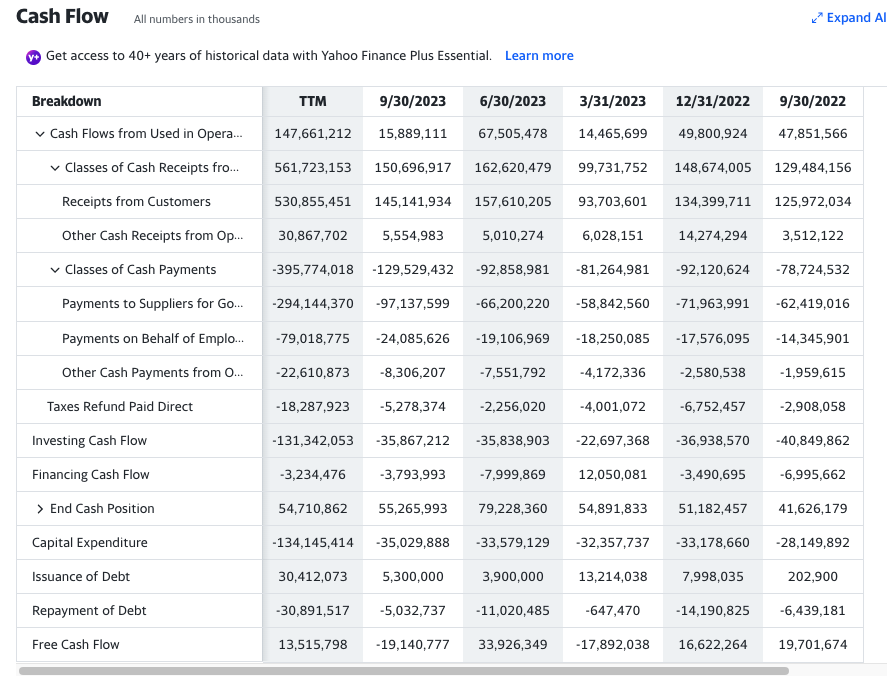

In the third quarter BYD reported record high sales revenues, net profits, and margins, a seemingly stellar performance. Yet according to Yahoo Finance, BYD free cash flow declined by a startling $53B, from a positive $34B in Q2 to a negative -$19B in Q3.

One additional thing I like about Tesla is that they report “deliveries”, not “sales”. Nobody delivers a $40k+ product until they have the money (or the backed loan, etc) in their account.

This is particularly odd since BYD announced record margins during a quarter when they were lowering prices to compete with Tesla. Tesla’s margins declined during this price war while BYD’s rose. Did BYD substantially reduce COGs? That would be quite a reduction.

But that doesn’t explain the big drop in free cash flows. Could BYD be dumping cars on dealers and counting them as sales as has been alleged in the past? I am slowly becoming a conspiracy theorist. Probably should get an X account.

Apparently BYD did last quarter. Again from Yahoo Finance, BYD showed a $12B decline in cash received from customers compared to Q2, while showing $23B in revenue growth for the same period.

Here are BYD FCF for the last five quarters. italics show negative FCF.

Q2 2023 was the anomaly. Otherwise the BYD business model is showing declining cash flows despite large increases in sales revenue.

Again, I’m just an amateur at finance and generally don’t have a clue, but this has the look of a company that is being significantly propped up by government subsidies. Is that what happened in Q2 2023?

According to this cash flow statement, “Payments to suppliers” is up by 35B from last year Q3, and “Payments on behalf of Employees” is up by 10B. And “Other cash payments” is up by 6B. Those appear to be the main large drains on cash flow when comparing 22Q3 to 23Q3.

This is part of what makes China investable to me. I have no clue what any of those items are or why they are so variable quarter to quarter.

That makes some sense given the rise in production. All things being equal, one would think that increase in payments should have been offset by the bigger increase in revenues year to year, 45B, with respect to cash flow.

It doesn’t make sense that payments to suppliers is up MORE THAN 50% while “receipts from customers” is up about 15%. This is 22Q3 versus 23Q3 numbers.

If I understand you correctly, it might make sense if “receipts from customers” means actual cash received by BYD and so for some reason an unusually high percentage of Q3 sales were on credit to BYD.

But that goes to the heart of my confusion. Revenues, profits, and margins hit record highs yet free cash flow plummeted for no obvious reason. I am hoping the bright folks here might have an idea of how this might have happened.

Is it plausible that BYD dumped a bunch cars on dealers, counted them as sold, but will only receive actual cash for the cars if/when the dealers sell them?

You would think a company that had negative cash flow in the previous quarter, is in the middle of a cutthroat EV price war in China, and has an aggressive ambition to sell product in Europe would have better use of cash than buying back stock.

A puzzling scenario, but they’ve got about $9 billion in cash on hand. Dropping $28 million of that into a stock buyback is trivial - it’s like 0.003 of their cash. Something so small won’t have any impact on their ability to do anything - or any real material impact on the stock price. So it’s probably just management realizing that investors (and maybe employees?) are really disappointed in the recent performance of the stock, and providing a little symbolic gesture to show that they are aware of that concern and take it seriously.