The problems being experienced in the worldwide financial industry stem from two key failures – the failure of banks and their customers (individuals and businesses) to accurately / consistently contemplate all of the components of risk in their financial decisions and the failure of governments and central banks to consistently enforce meaningful regulations that stop the feedback loop of ever-larger dumb corporations requiring ever-larger dumb banks to hold ever-larger concentrations of wealth.

Unique Factors Driving the SVB Failure

Initial reporting on the failure of SVB attempted to emphasize unique factors that contributed to SVB’s insolvency and takeover by the FDIC. Understanding these factors at face value is worthwhile for what they say about management decisions made by SVB executives and those of its customers. The basic narrative behind the failure is that SVB incurred a spike of withdrawals from some of its largest startup customers which required cashing out significant numbers of longer term bonds held by the bank to raise the cash, which forced the firm to take losses on those bonds due to rising interest rates set by the Federal Reserve.

Note that THIS round of withdrawals itself did NOT cause the complete failure. A few more days of iterative actions and reactions were required.

After selling some of its holdings at a loss, SVB executives decided they needed to raise cash and chose to do so via selling stock. The sequence of events here is what actually triggered the bank’s demise.

- SVB executives chose to raise the equity via TWO separate actions -- a typical common stock offering and a distinct offering of preferred stock. Common stock provides the stockholder voting rights in the company's decision making while preferred stock provides ZERO voting rights but provides a higher prioritization of dividend payments as compensation for the lack of voting influence.

- In an attempt to calm public concerns, SVB executives publicly announced their two-tiered equity plan so depositors, current shareholders and regulators could all relax knowing they had a plan.

- In fact, SVB's public announcement not only conveyed the size of its shortfall (the offers totaled $1.8 billion dollars), it confirmed ALL of the dollars the firm stated it needed would not be all available at the same time. Funds from the preferred stock offering would be delayed by at least a half day in order for the firm to complete the extra legal paperwork required for such an offering.

- This timing gap convinced many depositors that their funds would still be at risk for at least another entire day so depositors lined up the next morning to continue draining money from SVB accounts.

- The FDIC saw the continued run and stepped in to take over the bank.

It isn’t clear if a unified common stock offering executed in a single step would have saved SVB but the decision by its management to split the offering and inject a delay in obtaining the full $1.8 billion it publicly said was required GUARANTEED a run and the bank’s failure.

Besides this tactical error that proved to be existential (at least for SVB’s original management team), SVB reflected a multitude of unique factors that made the risk of failure a near certainty.

- geographically concentrated commercial customers

- high share of young start-up firms facing separate headwinds leading to high cash withdrawals

- high share of customers (commercial and individual) above the $250,000 FDIC protection limit

- investment decisions chasing higher returns on long term Treasures in a period of rising interest rates

- a vacant Chief Risk Officer positions for most of 2022

The first two bullets above merged into one bigger problem. The number of start-up firms in the same geographic region and similar industries magnified existing group think tendencies that kick in during financial crises. Higher interest rates made venture capital funding harder to obtain, making existing start-ups more dependent on existing cash on deposit. Firms seeing their prospects dimming might have required cash for severance payments, etc. Having a concentration of firms served by a single bank magnified those pressures and SVB lacked the diversification across industries and geography to act as ballast against those draws.

That original problem then triggered unique fears due to the profile of SVB’s customer deposits. While the FDIC officially limits deposit protections to $250,000 (more on this later…), it is common for a larger bank (i.e. a regional or national) to have accounts above that limit. Presumably, the assumptions made in these cases by both the bank and the depositor are

- the customer knows those dollars are unprotected

- the customer enjoys the convenience of drafting payroll checks and paying vendors from a single bank

- the customer does NOT want to manage N different accounts to avoid crossing the $250,000 limit

- the customer assumes they'd recognize signs of trouble to find alternatives before their chosen bank fails

- the bank enjoys the extra cash to use in its quest for returns elsewhere

Note - it isn’t clear if banks pay FDIC insurance for ALL of their deposits on hand or just the portion of balances under the $250,000 limit. If they only pay for the balances under $250,000, then essentially the deposits in excess of the $250,000 limit cost them LESS, given them an incentive to continue accepting the excess deposits. A gigantic moral hazard.

Here’s what the histogram of a typical bank’s account balances might look like.

The key point from this illustration is that the majority of assets (the area in green) lie BELOW the FDIC limit. In this environment, none of the depositors under the FDIC limit have any need to panic amid trouble so they don’t and the dollars in the accounts over the limit are not a majority of deposits. As such, the vast majority of the bank’s cash isn’t subjected to a run.

In contrast, SVB’s account histogram reflected VASTLY greater risk. Conceptually, it looked more like this, though this scale doesn’t reflect the HUNDREDS of millions present in many of SVB’s accounts – the $250,000 FDIC cutoff line would have been a blip at the bottom at that scale.

At SVB, an astounding NINETY FIVE PERCENT of the bank’s deposits were over the $250,000 FDIC protection limit. Many of those accounts over the limit had amounts that were ORDERS OF MAGNITUDE over the limit. Examples: Circle ($3.8 billion with a B). Roku ($487 million). Block-Fi ($227 million). Roblox ($150 million).

When rumors about a bank with THIS depositor profile begin swirling, the vast majority of the bank’s deposit accounts lie ABOVE the FDIC cutoff, meaning ALL of those customers face immediate risk of losing their cash and have EVERY reason to withdraw their money, and they do - IN DROVES. In the case of SVB, the initial triggering event prior to the big trigger was the sale of $21.billion of securities to raise cash for withdrawals that incurred $1.8 billion in losses. The $1.8 billion shortfall represented a small portion of the total liabilities but each individual depositor had no way to know if their account might get caught short so depositors attempted to withdraw another $42 billion before the FDIC closed the bank.

Operating a bank with this depositor profile itself is a catastrophe waiting to happen. It appears SVB compounded this risk with additional strategic failures. With a “traditional” retail bank with a mix of individual and commercial accounts, accounts are likely split between checking accounts and “time deposit” accounts like savings accounts and certificates of deposit which limit withdrawals per month or have fixed maturity terms which tend to make the money “sticky” and less subject to flight. At SVB, a large portion of its biggest accounts were commercial accounts used primarily for payment processing (payroll, accounts payable, etc.). Such accounts have ZERO “stickiness” and are VITAL to firms’ daily operations. SVB executives failed to imagine how the behavior of such customers might differ in uncertain times from traditional depositors and reflect a higher likelihood of flight as those firms worried about keeping their own businesses afloat. This profile essentially narrowed SVB’s margin of error and should have triggered more conservatism in its strategy.

It appears this profile actually magnified SVB’s risk as the firm used the piles of cash to chase higher returns by locking up cash in longer term, higher interest Treasuries. Since SVB’s customers were not necessarily expecting high returns (at first) on essentially checking account money, this at first proved lucrative for SVB. SVB’s year over year revenue increased 22.8% in 2022, 47.65% in 2021 and 15.6% in 2020. However, once the Fed began raising interest rates to combat inflation after COVID stimulus and disruptions, more customers began expecting higher returns on SVB deposits but SVB already had large chunks of cash locked up – at lower rates. There are entire courses in finance theory taught in business schools that likely sail over the head of most individuals (and most depositors) but understanding yield curves and impacts of changes in short versus long term interest rates is a requirement of anyone operating a bank filled with other people’s money.

It isn’t clear yet how much SVB executives understood these risks and reacted to them but one fact is quite damning in hindsight. The position of Chief Risk Officer at SVB was vacant between April and December of 2022. The previous occupant, Laura Izurieta, vacated the position in April but technically didn’t leave the company until October 2022 according to proxy filings. Those filings don’t reflect the circumstances behind Izurieta’s departure but the 6-month delay before final separation is frequently seen in cases where at least one of the parties is not happy about something and they agree to disagree on the specifics while keeping quiet about any conflicts. Did the firm find the CRO failed to steer them away from risks posed by the changing yield curves? Or did the CRO flag the looming problems and request strategic changes only to be ignored by the CEO and board?

A final factor that likely played a role in SVB’s demise was the archaic nature of its own internal IT systems. Despite being in business for 40 years and despite operating in the heart of Silicon Valley amid hundreds of high tech firms who acted as customers, SVB’s internal systems were in fact woefully out of date. Its systems presented unique challenges to the flows required to accept PPP payments from the government and to the load imposed by thousands of commercial users attempting to use its online tools to handle those payments. One CEO customer of SVB (David Selinger of Deep Sentinal) stated the company’s back-office system locked up as thousands of its commercial customers attempted to use its online banking tools to manage incoming PPP payments and map them for payroll and accounts payable functions. Customer-facing systems that poorly perform in good times do not inspire confidence in bad times, triggering more fear and doubt that contribute to a run.

If basic self-help portal functions for customers were antiquated, perhaps it is too much to expect much of the more critical core systems supporting senior management. What types of analytics did SVB generate against its account and customer profile data each day? How did they analyze inflows and outflows by customer segment to spot worrisome trends? Did they have warning threshholds for the number of accounts exceeding FDIC limits or the total dollars exceeding FDIC limits? Did they review the bank’s investment portfolio for sensitivity to changing interest rates? Did they define limits on the duration of Treasuries and bond maturities in light of their own customer cash demand patterns to avoid getting caught short? Of course, these types of questions tie into larger questions about similar peers and the larger industry.

Shared Factors Driving the SVB Failure

One thing is common with all financial failures. From the Asian Crisis of 1997 to the post 9/11 recovery in 2001 to the 2007-2008 meltdown to the present failure, public statements at the beginning of each crisis from banking leaders, politicians and regulators follow an identical script:

The () failure is an unfortunate but unique circumstance. Officials have carefully reviewed the situation and have crafted a series of actions to protect the larger system. We have spoken with leaders of other major institutions who are confident similar issues will not occur with their firms. The (_) public can operate as they normally would. Now is not the time to panic.

Uh huh. In times like this, here are the questions the public should be asking:

Is the situation at SVB unique? Absolutely not. Backoffice systems at most megabanks formed from mergers of mergers of mergers likely date from the mid-1990s, making them difficult to maintain and expensive to enhance to offer new capabilities for customers or new insights for management that could improve risk management. SVB is also not likely to be the only bank managing large numbers of accounts exceeding FDIC protection limits. (See the next section on systemic risks for insights into why.)

Do bank executives and regulators have the proper “telemetry” to identify similar looming problems at other banks? It’s already clear SVB’s systems were woefully antiquated, making it likely they failed to devise metrics that could have set limits that would have prevented them from getting burned by shifting yield curves. Do other banks have better systems? Virtually all banks faced the same audit requirements after Dodd-Frank and the same financial climate to drive their priorities for investing in their back offices. It is safe to assume many banks have no better telemetry in place. Why bother crafting new alarms when you are tagged as TBTF? If telemetry improvements are skipped and things go well, the money that would have been spent on tools can be distributed to executives and stockholders. If things go poorly, well, TBTF, the government will bail us out. Why spend the money?

Assuming the required telemetry is available, do other bank executives and regulators have the willpower to ACT upon the telemetry to correct problems and avoid them going forward? There’s no way to factually answer this hypothetical question but the past is likely to be prologue. A wide range of financial institutions have a decades long track record of operating for their own short term benefit, even in direct conflict with fiduciary obligations to their customers, be they wealthy individuals, large commercial accounts or fellow institutions. Given the distorted moral perspective created by TBTF status, it is highly likely executives are eager to avoid acting on news of POTENTIAL risks as long as profits continue flowing for the current quarter.

Will there ever be a time when regulators or politicians will tell the public to move deposits out of harm’s way? Uhhhhh, obviously not. Leaders and experts will ALWAYS say “this is not the time to panic, just sit tight.” That doesn’t mean that won’t be the appropriate action nine out of ten times but it means leaders and experts will NEVER clearly state depositors in a specific bank need to take their ball and go home. Depositors with balances above FDIC limits will be on thier own to understand their own risk tolerances and the risks posed by the banks they choose to use. This requires a substantial boost in financial literacy. This sounds odd to state in relation to people in control of large sums of money but the SVB failure made it clear THOUSANDS of customers (individuals and companies) operated with tens and hundreds of millions of dollars without FDIC protection.

Regardless of one’s account balances, every depositor needs to understand EVERYONE they encounter in the financial sphere is talking their own book and is dispensing advice one hundred and eighty degrees out of phase with the interest of individuals situated outside the 0.1%. Indeed, Jim Cramer appeared on CNBC on February 8, 2023 describing the firm as a good play on the bounce back occurring with a collection of tech stocks which had tanked in 2022. He correctly identified the bank as concentrated in the “merchant bank to startup firms” sector and stated “private equity investors aren’t going anywhere.” On March 9, 2023, Cramer’s story was different. “SVB was getting killed on its bond portfolio each time the Fed raised interest rates. The bank didn’t signal that it had too many bad loans that were backed up in stock of startups that hadn’t been able to come public because there’s no appetite for IPOs when the Fed is tightening aggressively. They should have been raising money like CRAZY for MONTHS like some of the other banks out there.” For those outside the 0.1%, education, skepticism and vigilance are the only viable defenses.

Systemic Factors Driving the SVB Failure

So far, it seems clear that SVB wasn’t a one-off. There were two other failures (Silvergate and Signature Bank) bracketing the SVB failure. As of March 16, 2023, a collection of uber-banks (the capital TBTFs?) including JPMorgan, Citigroup, Bank of America, Wells Fargo and additional sub-uber banks (the lower-case tbtfs?) announced a plan for a total of $30 billion dollars to be infused (no better word, really) into First Republic Bank. Why? Officials stated it was intended to convey their collective confidence in the banking system but investors were selling off First Republic Bank stock, raising fears a dive in the stock price would trigger a run similar to SVB which the bank couldn’t survive.

Clearly, there are immediate forces at work creating acute conditions for marginal institutions. There will likely be other failures as part of this “wave.” It is more important to understand the systemic factors that are creating SERIES of failures over time, seemingly like clockwork, ten to fifteen years apart. What are those factors?

Forgetting Prior Disastrous Teachable Moments – The US created a firewall between retail and investment banking via the Glass-Steagull Act in 1933 after massive losses in investment banking contaminated retail accounts, tanking the entire economy. Politicians were convinced by financial experts that technology cured the system of such risks, leading to the passage of the Commodities and Futures Modernization Act of 1999, which eliminated the investment/retail firewall requirement which led DIRECTLY to the 2008 meltdown. The failure of banks to accurately valuate their derivative investments led to recurring “stress test” requirements under Wall Street Reform and Consumer Protection Act of 2010 (Dodd-Frank) whereby banks had to prove they could support worst case deposit draws even under extreme market conditions that might materially reduce the value of their assets. Banks and clear majorities in both political parties voted to eliminate those tests for all but the biggest banks only eight years later via the Economic Growth, Regulatory Relief and Consumer Protection Act (bitterly ironic name, huh?) of 2018. The relaxed rules eliminated stress tests for all banks with under $250 billion in assets. The 2018 changes were supported by CEOs of many regional banks, including the CEOs of SVB and Signature. SVB’s CEO provided testimony to Congressional committees as far back as 2015 pushing for tehse relaxed rules and Signature Bank donated heavily to key Democrats who served as co-sponsors of the 2018 legislation.

Predatory Self-Dealing – Also coming to light in the SVB incident is a familiar pattern of even larger financial institutions contributing financial advice that may prove to be completely incompetent at a minimum or perfectly hedged to generate outsized profits for the advisor at the expense of the advised. SVB obtained investment advice from Goldman Sachs regarding its portfolio and Goldman was one of the institutions who gobbled up some of the securities SVB unloaded as part of its $20 billion dollar fire sale to raise cash. Goldman made a quick $300 million off those trades. Sound familiar?

Lack of a Corporate Death Penalty – Justice officials and bank regulators alike in multiple countries seem completely unwilling to impose a “corporate death penalty” upon financial institutions involved not only with heinous crimes in their own right (arms trafficking, money laundering for terrorists, etc.) but crimes and incompetence which impair the bank itself with all of its TBTF interconnections that could trigger larger failures. As of March 16, 2023, Europe is facing it’s own “unique” basket case in the entity Credit Suisse. Credit Suisse has been labeled as one of the 30 largest systematically critical banks in the world and provides wealth management services for entrepreneurs and the uber-wealthy worldwide. The bank has seen a 75% decline in its stock price over the last year and industry experts and regulators are quick to state its immediate problems as of March 16, 2023 are totally unrelated to the problems reflected in Silvergate, SVB, Signature Bank and Republic Bank. Instead, Credit Suisse has demonstrated a pattern of criminal behavior over decades that has resulted in CEO churn, a series of investment bets on behalf of large sovereign wealth clients that resulted in large losses, and more recent losses based on rising interest rates lowering valuations of its existing portfolio. Despite being “unrelated”, failures of US banks trigger a hunt for other weak victims across the globe whose books might collapse from an unexpected draw down of cash or an unexpected loss in its portfolio. Credit Suisse obtained a $54 billion injection from the Swiss central bank as a means for calming global fears but not all watchers are convinced that is enough. The plight of Credit Suisse is also generating speculation that Deutsche Bank will encounter similar rough seas for similar reasons.

Key Learnings (So Far)

Banks and the incompetent politicians they own materially misrepresent what constitutes a “small” bank. Banks managing less than $250 BILLION dollars are not “small banks” by any definition of the word. SVB had about $208 billion in assets as of late 2022. Any bank managing $208 billion or $150 billion or $50 billion in assets still has to settle its books with overnight loans to/from other banks or the Fed. When MILLION dollar amounts have to slosh back and forth between banks every night, ANY sudden perception of existential risk can trigger ripple effects between dozens of banks. Tiny local banks can do little to solve a liquidity problem at a mega-regional or mega-national bank which ensures ANY problem at one tier can ripple laterally within a tier or vertically up to other banks instantaneously.

Banks continue growing larger and larger for a single related reason - the failure to adequately enforce anti-trust regulations. At one level, failing to enforce anti-trust limits on banks themselves means fewer minds impact more assets so a single bad action (whether by incompetence or active malfeasance) can impact an ever-larger pool of assets. Banks argue they MUST get bigger because their business customers are getting larger. A bank with a mere $200 million under management cannot handle the payroll of a single company whose biweekly payroll for 40,000 workers is $120 million dollars. A bank with $3 billion under management cannot handle a commercial account that has $1 billion in retained earnings in its treasury. But that cannot be a logical argument for allowing unlimited growth for banks. Consolidation of entire sectors into near-monopolies not only creates systemic economic risks for the same reasons (fewer unique minds controller larger pools of assets), it is already stifling innovation as the megacorporations focus on protecting existing products rather than inventing something better.

Governments repeatedly push stimulus dollars primarily through banking channels on a top-down basis where the public stimulus is diverted for private gain by the exact parties and practices that produced the failure being mitigated. On March 14, 2023, PBS’ Frontline program aired an insightful two-hour report entitled The Age of Easy Money that presents a convincing unifying theory regarding the cause of the current financial dilemma facing the US. The program can be viewed online at Frontline: The Age of Easy Money

The thesis of the program is basically this:

The Federal Reserve offered freakishly low interest rates for ten years after the 2008 meltdown. At first, they were required for a few years but after roughly 2012, they were not strictly necessary. The Fed continued them thinking both governments and corporations would take advantage of them to invest in critical infrastructure (roads, bridges, chip plants, new assembly lines) that would provide long term boosts to productivity in the economy. Instead, they continued past 2016 and instead of passing infrastructure bills, Congress passed tax cuts for the uber-wealthy and corporations borrowed BILLIONS of dollars at absurdly low rates and used the cash to buy back their stock and boost bonus metrics and options payouts for executives, further funneling trillions into the 0.1%. This magnified wealth inequality and did NOTHING for productivity. When the Fed attempted to take the crack cocaine away with initial rate hikes in 2018, markets screamed and Jerome Powell cowered and reversed the rate hike, adding another two years to the party. By the time the COVID lockdown hit, adding another $2.3 trillion of cash stimulus to the economy put all those distortions into overdrive.

After watching the program, an obvious question comes up. If stimulus for the COVID lockdown could not reliably transmitted through banks, what alternatives could have been considered?

Here’s some fun with numbers and math and the concept of simplicity:

- the CARES Act providing COVID stimulus in 2020 spent $2.2 trillion dollars

- of the $2.2 trillion, $300 billion went directly to taxpayers, $800 billion went to business owners as part of the Payroll Protection Program (PPP) and $1.1 trillion was injected into banks through Fed purchases of corporate bonds and other financial instruments

- in 2020, a total of 157,494,242 tax returns were filed

- those 157,494,242 tax returns reflected a total of $12.533 trillion adjusted gross income

- that's an average of $79,577 income per tax return

- an average income of $79,577 equates to $1530 in weekly income

- at the time, everyone thought a shutdown might last 8 weeks

- sending a check replacing 8 weeks of "average" income for all tax filers would have cost 8 x $1530 x 157,494,242 or $1.928 trillion dollars

If you skip payments to the top 1% of earners, that could be approximated by just ignoring the 1,574,942 returns with the highest income, reducing the payout by $19.28 billion. The exclusion cutoff point can slide left or right as fairness dictates. All the math could have been done with 2018 tax year data which should have been available by April 2020 (many 2019 filers would just be submitting returns in April of 2020).

How would the impact of this distribution scheme differ from the actual approach chosen? It would have bypassed all the fraud encountered with the Payroll Protection Program component (nearly $80 billion dollars of fraud as of 2023). Wage earners with incomes below the average $79,577 would receive a proportionately higher pandemic payment which would actually reflect the disproportionate risk facing lower income workers during an economic emergency. The distribution of dollars into banks would have exactly mirrored the existing allocation of consumer accounts across the retail banking system rather than allowing resources to funnel to existing TBTF banks. Small business wouldn’t have to worry about meeting payroll since their workers would have their equivalent net income deposited directly to their account or sent to them by check with zero middleman fraud.

Financial Literacy and Risk

The American public has suffered through financial failures only to see protections enacted then rolled back (Glass-Steagull then the Commodities and Futures Moderization Act then Dodd-Frank then the 2018 bill…). It’s clear individuals are failing to achieve a base level of financial literacy required to reject the pleas from the rich and powerful talking their own book looking for “regulatory relief” that privatizes obscene profits and socializes obscene costs of failures. The worldwide public needs a crash course in the basics of financial operations, ranging from accounting, audits and regulatory capture and corruption but most urgently, the public needs a more complete model for understanding financial risk and the use of interest rates as a catch-all indicator of risk.

The majority of individual consumers loosely equate interest rates with inflation and assume one is a direct reflection of the other. A minority of people may have a vague recollection that central banks use interest rates they set as a lever to try to manipulate inflation rates to optimize economic growth and employment. Extreme levels of infation (high or low) can be problematic and unexpected changes in inflation levels can damage the economy so many understand interest rates reflect those risks. But at a more conceptal level, “interest rates” reflect multiple dimensions of risk at work in the economy, not just risks associated with inflation. What are those dimensions?

Time Risk – The time value of money is the most foundational component of interest. It reflects the fact that every rational human values X units of a thing in their hand TODAY more than they value the same X units of the same thing at any future point in time. Intuitively, this makes sense and holds true in most situations (***). With X in hand today, there is no risk that X won’t be delivered at some point in the future or that each unit of X won’t change in value so now always has more certainty over “eventually.” In theory, even if all other risk categories could be “solved” and reduced to zero, lenders would still demand SOME interest payment solely to compensate them for deferring an amount into some future period.

*** In certain market conditions (such as a massive, temporary drop in demand) it is possible for people to prefer more at a later point in time than now if they are short of storage facilities, etc. The temporary negative prices for oil during the initial pandemic lockdown is an example of this phenomena.

Monetary Risk – Lenders face monetary risks when they agree to accept future payments for a loan denominated in a fiat currency whose quantities are managed by a third party (typically, a central bank or government treasury). Any time the supply of fiat money grows FASTER than “real” growth in output of the economy, the future value of each unit of that fiat currency is reduced. If a central bank “prints” money at a 7% growth rate when the economy is only growing at 3%, lenders come to believe they are being paid back with inflated bills and will demand a higher interest rate on a loan to make up for that inflation. Millions of pages and blogs have been written about the interrelation between inflation and monetary policy which won’t be re-debated here. Suffice to say there is one school of thought that believes all inflation stems from manipulations of monetary policy by central banks and governments. Others believe some inflation can simply reflects market forces correcting for imbalances in supply and demand – for labor, raw materials or actual final goods and services – and can have little to do with what a central bank is doing. As an example, if healthcare costs are a key part of the market basket used to measure inflation, a sudden event like a PANDEMIC that drives tens of thousands of healthcare workers OUT of the field in frustration will drive up healthcare costs as hospitals pay higher wages chasing a smaller pool of workers but this increase in prices has nothing to do with monetary policy.

Borrower Risk – Each borrower poses unique risks based on their trustworthiness as perceived by the lender and factors that might limit or completely eliminate the borrower’s ability to pay back a loan at some future date. If a bank is considering a 4-year loan to someone operating a roofing firm, there might be less risk lending money to a twenty seven year-old roofer than a fifty eight year old roofer who might face a higher chance of a workplace injury that could end their ability to work.

Industry Risk – In addition to borrower-specific risk, there can be risks specific to an industry that could stem from technology changes, regulatory exposure, etc. that might increase or reduce the overall risk of payback by the borrower. A single lender looking at two potential borrowers for the same loan amount and term and similar individual credit histories might view a borrower in an industry with a long track record of income stability more favorably than a borrower in a high-tech industry that has only existed five years and has twenty start-ups attempting to be the next Google of that field when only two will even reach IPO. The lender might also attempt to analyze the risk of looming regulation or changes in government incentives as a factor of the interest rate on a loan.

Geopolitical Risk – Geopolitical risk covers the possibility of world events (wars, coups, shifts in political leanings for countries or regions) impacting the operations of the borrower and their ability to pay back a loan. With all other factors being even, a lender considering loan requests from an oil refinery company in the US and Ukraine would obviously demand a higher geopolitical risk premium from the Ukrainian firm, even if the two firm’s track records for soundness were identical prior to February 2022.

So is this concept really useful? No and yes.

This concept is NOT useful in the sense that borrowers will never see their overall interest rate offered by a lender broken out into these factors. In fact, in many individual and small business lending scenarios, lenders are PREVENTED from setting interest rates per client as part of discrimination protections. If five borrowers approach a bank on the same day with five slightly different credit histories and business proposals to pitch requesting the same loan amount and term, rather than all five getting loans at five unique interest rates, it could be that only three get a loan – all at the same rate – and two others simply get declined.

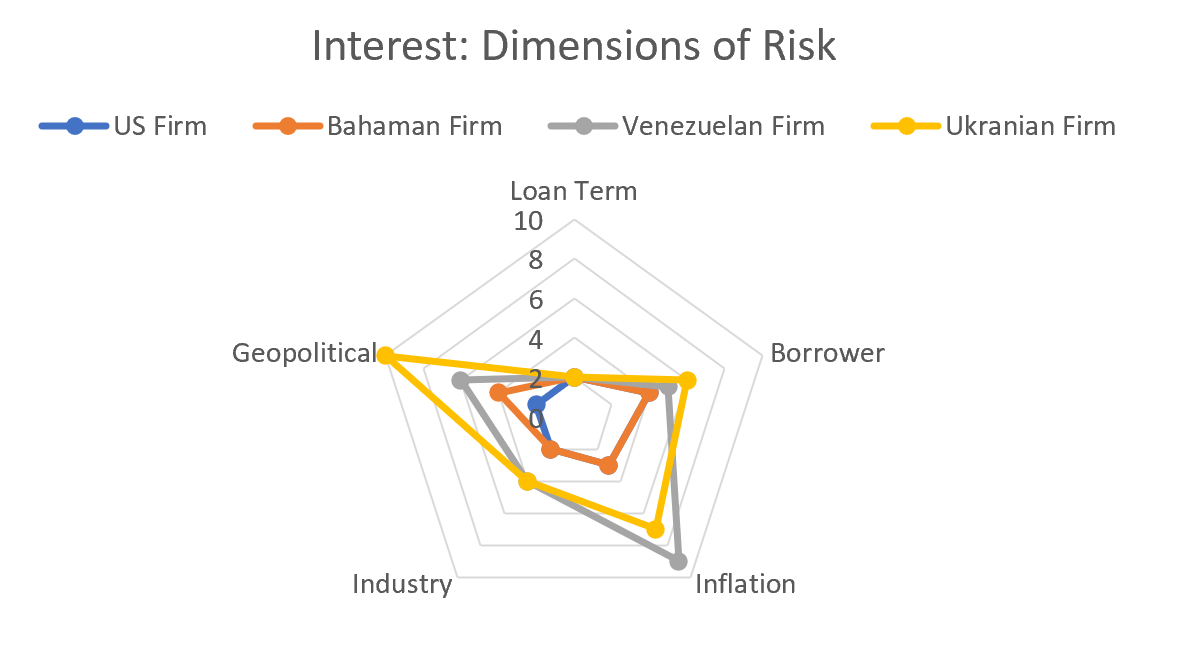

The concept IS useful however when analyzing collections of customers and strategies selected by banks when setting lending criteria and investing depositor money. If a bank was considering four loan applications for identical amounts and identical terms from four different clients, their component scores might look like this in table format:

More numerate types might be able to digest those numbers and discern that the Ukrainian firm represents the highest risk but the raw numbers still wouldn’t intuitively convey the exact degree or how they compare across dimensions with the other firms. Imagine instead the numbers are graphed in “radar graph” format as shown below:

The area of each polygon directly reflects the total risk of each borrower and the stretch in each dimension immediately conveys the extent each dimension contributes to the total risk.

The same “radar” technique can be used to compare dimensions of behavior between types of accounts within a bank or quantifiable characteristics of customers (dollar amount exceeding FDIC limit, payroll, angel investor capital, revenue, etc.). Banks should be conducting this type of analysis to identify how market shocks might trigger collections of customers to act in concert in ways that could exhaust capital on hand. The events between March 9 and March 16 of 2023 make it clear most banks are giving this type of analysis lip service or are not doing it at all. Obtaining these insights is deemed unimportant because they’ve identified easier ways to maximize bank profits when things go well and are assuming divine intervention will protect them as too big to fail when things go wrong.

Is this concept valuable for individuals? Yes. By thinking of “interest rates” in terms of these components, individuals deciding where to put their savings or where to house a checking account with large sums of money can look at interest rates offered by a bank then ponder how those rates reflect all of these components. Remember, in a savings scenario, essentially the DEPOSITOR is the lender and the BANK is the borrower so all of these factors still apply, only the party in the driver’s seat changes. Some examples:

Why is Bank of America only paying 0.04% on savings accounts and First Bank of Hollywood is paying 2.9%? Possibly because FBOH is viewed as a small bank with limited assets and thus considered a higher risk and has to offer higher interest rates to savers to compensate them for the risk of not putting their money in BOA, viewed as too big to fail.

Why is First Bank of Podunk paying 4.3% while equally small First Bank of Hollywood is only paying 2.9%. Possibly because FBOP is located in a rural community dependent upon crops and their region has been inundated with flooding, raising the risk of many of its deposits getting withdrawn and many of its borrowers becoming unable to pay back loans. To continue attracting deposits, they have to offer a higher rate to compensate the depositor for the risk.

Why is Mutual of Miami issuing a new round of 10-year corporate bonds at 7.3% when Mutual of Montana is only paying 4.9% and 10-year Treasuries are only paying 3.39%? Possibly because Mutual of Miami’s insurance business is subject to vastly larger risks from hurricanes, flooding and tornados than that of Mutual of Montana whose customers only have to worry about droughts and blizzards which typically don’t do much property damage requiring payouts.

In short, individuals cannot just go chasing high yields without understanding the risks signaled by those higher yields and understanding if those risks are appropriate for the tolerances of the individual. if rates in general are 4% and an opportunity presents itself offering 9%, there’s a reason for it.

WTH