Hey all, this was a busy month for the portfolio selling seven stocks and adding four new ones. Both Iren and Electrovaya are starting as high confidence positions.

Results as of the market close on August 29 were,

2024: +146%

2025: +80% YTD

Cumulative return +343%

Allocations,

AppLovin APP 19.2%

Iren IREN 18.2%

Astera Labs ALAB 17.9%

Electrovaya ELVA 9.1%

Credo CRDO 9.0%

Reddit RDDT 8.2%

Dave DAVE 8.1%

Health in Tech HIT 6.1%

Hive Digital Technologies HIVE 3.5%

Zoomd Technologies ZOMD.V 0.6%

Promising new ideas we looked at this month,

Halozyme Therapeutics HALO - drug delivery platform superior to IV, credit to @ryshab for finding this one

Curiosity Stream CURI - streaming platform for educational content

DLocal DLO - payment processor with a big quarterly step up

The Real Brokerage REAX - real estate broker with a nice quarter

Solesense SLSN - B2B seller for skincare minerals ingredients

OptimizeRX OPRX - platform for integrating electronic health records

The new format (skipping the stategy) works well, in my opinion. Your opus includes plenty of strategy, fine to skip that on the reviews, unless of course the review itself alters your thinking. I’m very interested in the 2022 retrospective. A friend (a wealth manager) recommeded that I read: The Art of Execution: How the world’s best investors get it wrong and still make millions. I haven’t finished yet, but the author, who for years supervised a group of investors, noted certain habits that helped his best investors to outperform. He writes that a relatively concentrated portfolio with relatively long holding periods is how his best investors outperformed, but emphasized the importance of: (1) not allowing a loss to go beyond 30% because when losses go much beyond that, it becomes increasingly difficult to recover; (2) periodically harvesting a relatively small portion of accumulated gains which he believed helped them to remain psychologically balanced and less likely sell too much of a winning postion too soon. Your modus operendi is similar in the sense that you will sell a position down if it becomes larger than 25% of your overall portfolio. I’m very grateful that you and so many others on Saul’s take the time and effort to share the fruits of their knowledge and experience.

I should have mentioned that the aforementioned wealth manager is someone I’m working with (and has become a friend). His guidance for me (I’m retired) is similar to the Art of Execution in that he encourages me to sell a relatively small portion of winning positions on a regular basis with the purpose of building a reserve in advance of the next bear market. He has seen too often how clients won’t sell at better prices and then are forced to sell when blood is flowing in the streets. He works at Fidelity Investments and said that many of the money managers there have read The Art of Execution.

Great update! Thank you for introducing ELVA, I’m looking forward to the introduction video.

I was looking at their yearly revenue and noticed a huge drop in 2017. A quick search I found that they had been supplying batteries for Daimler’s Smart EV program, but that contract wound down in late 2016. At the same time, the company pivoted away from automotive and into the forklift/material-handling market.

..this pivot caused the market cap to drop almost 20x. After the pivot it took half a decade to reach the same yearly revenue. My concern is this: with better foresight and planning, could management have avoided such a painful revenue gap? And aren’t you worried that something similar could repeat if they misstep again in transitioning to a new segment?

@twillo The Art of Execution sounds like it could have some relevant insights. I ordered a copy!

I would draw one key distinction on the 30% loss rule. If the loss is because the company underperformed it is an easy sell decision. However, if the 30%+ loss is from general market conditions or just pessimism about the stock, but the results have never faltered we will hold through those drawdowns. For example, with Astera Labs it got up to $140+ but then traded down to below $60 but they never posted a poor result.

There’s only really one growth investing book in my study corpus that I have revisited time and time again which is Common Stocks and Uncommon Profits by Philip Fisher. It was first published in 1958, so some of the points need to be adapted for modern times. I will eventually have some content regarding this book on my channel, but here were some big take aways that have stuck with me,

Fisher looks for companies that have both strong R&D and S&M. Meaning we want a superior research organization along with a talented sales force. If the company produces a great product but cannot sell it’s bad for investors. Likewise if the company is incapable to release new products, but has a great sales force it is also going to lead to a poor result. Under this theory we actually prefer to see some rising R&D and S&M costs, and R&D which is decreasing is often a yellow or red flag for a business

Fisher like to invest behind industry trends or what we usually call a tailwind now. He was discussing how the 1960s will see the biggest boom in semiconductors the world has ever seen. One of his big investments was Texas Instruments, and that proved to be an incredible call as the stock went on a historic run in the 1960s. Additionally he added 30 years from now we will see an even bigger semiconductor boom (implying 1990s) and 30 years after that the semiconductor boom will dwarf the that one (implying 2020s or right now). When I was first reading this book two of my high confidence holdings were Supermicro and Nvidia. He literally called it exactly as it would play out!

Fisher talked about how investors like to get behind popular stocks. Back in his day it was the Nifty50 and he mentioned some investors will feel “prestigious” just owning these stocks. He talked about how the list sometimes expands and narrows like in recently times the list was FANG or then expanded again to Mag7. He said the main issue here is hindsight bias. These companies have already risen to to the top and proven themselves, but it does not indicate future performance.

@SailingDev The material that really put me over the top with confidence for Electrovaya was listening to the 16th Annual Midwest Ideas Conference where the CEO spoke recently. It’s available in the Quartr app if you want to track down this conference.

He spoke about how the company was on the verge of bankruptcy seven years ago, but Walmart decided to give them a chance for their forklifts. The process for Walmart to swap batteries was complex and risky. It meant taking out a 2,000 pound lead acid battery from the lift and putting in a new one. With ELVA’s batteries the theory was they would not need to replace the battery.

Now seven years later, these batteries in the initial forklifts have outlived the forklift itself! The forklifts have broken down before the batteries did and Walmart can still use those batteries. What has changed in the story is now they have a proven 100% safety record, a battery has never caught fire. They also have the “life cycle data” showing these batteries really do last a long time as advertised, it’s not just theory.

The main competitors in lithium ion are cheap manufacturers from China and Korea, but they do not have any innovation. The CEO said that 30%+ margins are stellar in this business where competitors are running with lower margins. However, the main difference is now performance, the company’s batteries way outperform competitors with their proprietary technology meaning they can move up market. They said they ship batteries to Japan now for Toyota, and how rare it is to be shipping batteries from North America to Asia. Traditionally the flow was one way with batteries coming from Asia to North America.

Some additional details which were impressive,

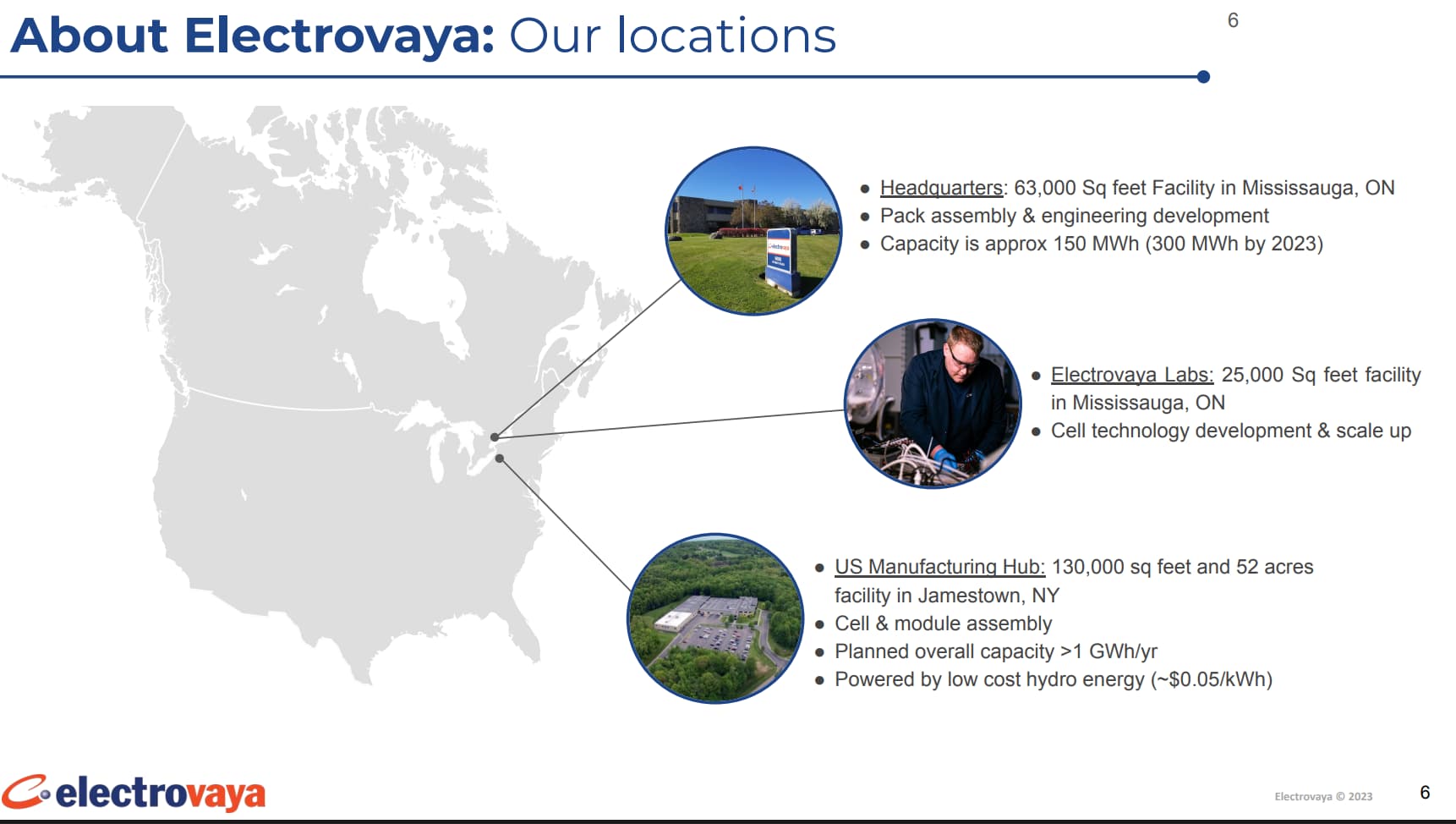

Jamestown increases production by 3x with a local supply chain as they are running into capacity constraints soon and this site comes online next year, Jamestown is 2.5 hours from HQ, they drive down there all the time

Entering additional verticals such as defense, submarines use lead acid batteries which is again a safety risk, now that they have the life cycle data there is real interest where having 1/4th the density of lead acid is really appealing

Robotics, “growing very rapidly”

3 robotics OEMs using the tech, set to grow further

Looking at energy storage

“Applications are expanding, manufacturing capacity is expanding”

Toyota is a promoter of them, Toyota is paying for independent studies of their batteries in the US, “some of the world’s best relationships”

Toyota has 5+ years of data with no degradations in performance

Toyota is able to lease ELVA batteries with a strong residual value

“appetite for higher performance batteries as sectors become more mature”

Looking to add recurring revenue streams like data analytics

Looking at subscription models rather than just selling batteries, starting “energy as a service”

“making net profits, able to put cash back in the business”

“exciting technology which doesn’t have much in terms of rivalry”

Solid state batteries from Amprius and Enovix are more niche products (they called them out by name)

Lower sticker shock by leveraging performance

Core customers provide 12+ months of visibility, seeing 12-18 months out

Data center use case, keeping in mind a data center burning down is billions in damage which has happened from lead acid batteries

Their batteries in cars would do 14,000 cycles, or 3.5M miles (this is why they failed in auto, too much performance for no reason)

Jamestown 0.05 kWH low cost and all renewables, Bitcoin miners keep asking if they can join there, they tell them no repeatedly

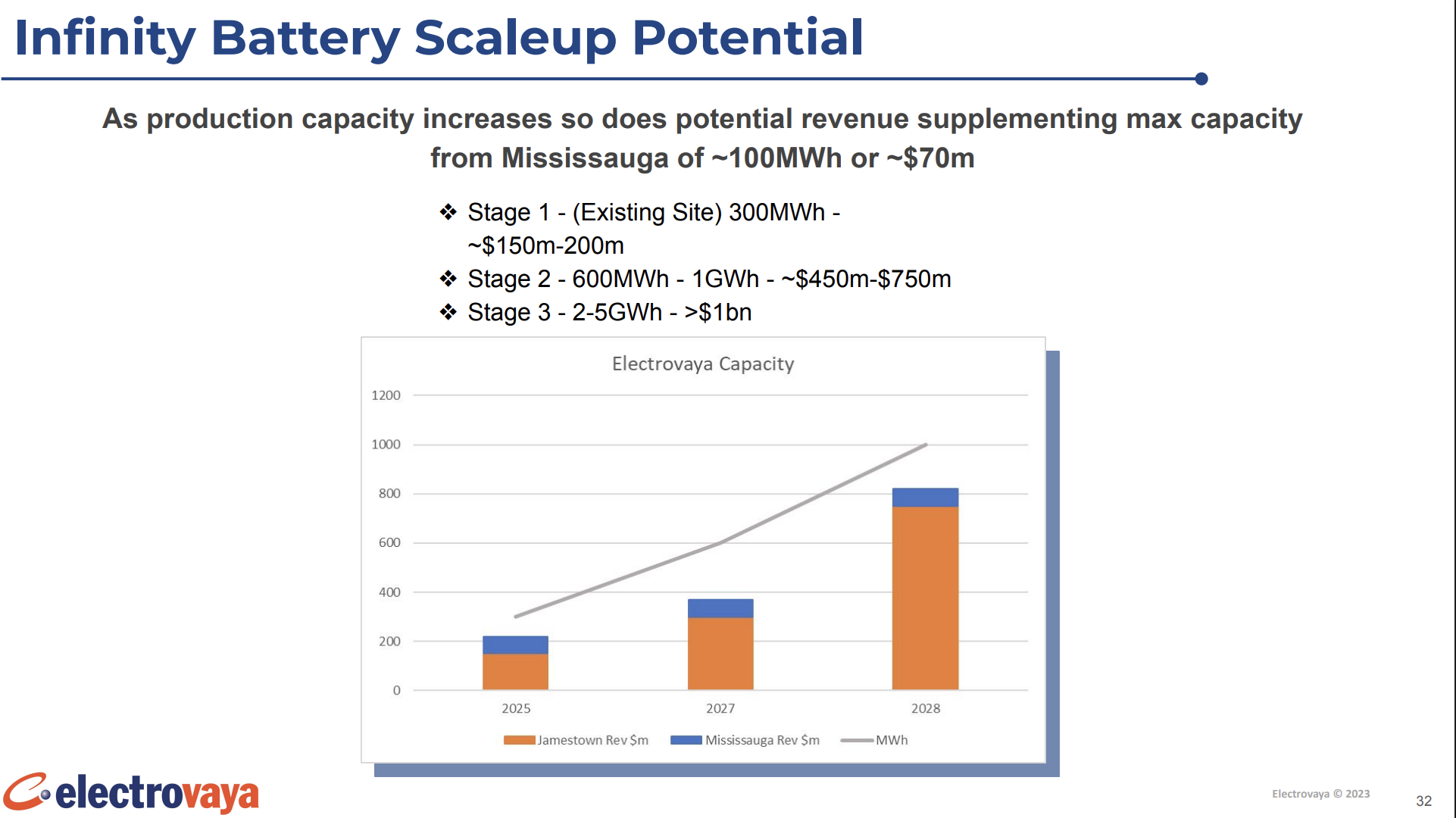

There is a whole lot more to cover with the company as well, these were just some of the highlights! With the market cap at just 250M, it seems way to low to me. They are ramping up massively, outperforming competitors, and getting into SaaS and recurring revenue.

Wow, one of the recent reviews that caught my attention. Too bad that my brokerage has deemed it too illiquid for trading through them. I submitted a review request and put it on my watch list. (Was going to open a 1% position to force me to research, but guess I have to do it without motivation now…lol.)

I’m always wary of battery companies. And statements like this are red flags for me. Companies don’t fail in automotive because their performance is too good, they fail because automotive is one of the tougher battery applications: They need the right balance of power density, energy density, safety, charging speed, cycle life, and probably a few more.

There are no large-scale solid state batteries from anyone on the market now. I can’t tell if ELVA is pushing that tech or responding to that tech, but it’s still years away from things much larger than an earbud.

The shipment to Japan is just one and just recent.

Selling “energy as a service” and claiming SaaS are also red flags for me. Sure, a battery lease model can make sense, but that’s not what they’re calling, right?

Company has been around for decades, why now are they poised to take off?

Sure I get the lead acid battery replacement market is a good one. Is that their main market, and how is that growing versus the competition, etc.??

Lead acid batteries are really safe. Are there actually documented cases where lead acid batteries caused a data center fire?

Yah, I hate when I hear about an interesting company, look up the stock history, looks great over the last year, and then I pull up 5 years and … oops. Now, I well know there are acceptable stories for a number of patterns, but it is a dose of cold water.

Looking into that last question there has led to an interesting thread. I was asking Perplexity about if there have been documented cases of lead acid batteries causing a data center fire. It gave one example in Strasbourg, Germany of a data center fire from 2021 where the suspected cause was a lead acid battery system. It also added the detail that data center fires are more often caused by lithium ion batteries, which I think leads into the other question of why now.

The technology that Electrovaya has is designed to prevent fires and insulates the cells from being able to spread overheating easily. They say they’ve had a perfect 100% safety record and now they have the life cycle data as well. This explains better why this type of battery was not taking off in previous years; there was documented risk that fires are more common with lithium ion. The producers from China and Korea do not have this protection from heat spreading between cells, which is why those manufacturers are not an option for a customer like Walmart or Toyota.

Another part of the why now question is the stakes are higher now. Before it was less expensive servers but now its Blackwells with a lot higher power requirements. The machines themselves cost a lot more and the risk is higher with greater power consumption. Many of these data centers are powered by solar, and they need somewhere for the excess energy to go which is driving development of battery systems.

I’m not too sure about the solid state batteries being years away from significance. The interest primarily comes from industrial customers who need added performance. Many of these designs are probably prototypes that defense contractors are trying out. Here’s what Amprius said about their customer count on the latest quarter,

In Q2, we shipped batteries to 93 customers, 43 of whom are new to the Amprius platform. The remaining 50 are repeat customers, including several of our long-time strategic partners such as AALTO/Airbus, BAE Systems and the U.S. Army.

Here’s what the CEO of Electrovaya said about competitors and entering a new space,

If you look at some of our competitors, there are companies that have shown success with silicon anode-type cells. And we think ours could be the arrival at that. It won’t be a silicon anode; it would be a lithium metal anode. So, probably even higher energy densities. So that’s what we’re targeting. We want to get it right before we want to get the samples to the potential customers, before we push it.

As for misrepresenting their subscription model, it sounds like the analytics platform they are proposing is SaaS. It’s never going to be a purely subscription model like native SaaS companies but it technically fits the definition if customers are paying for a subscription to that software. Between Toyota already leasing ELVA batteries and adding in a new analytics platform, that could add to potential upside.

It’s not a question of interest, it’s a question of the technology. Everything I’ve read says solid state applications at any resonable scale are still years away, and for tough applications like cars, probably half a decade away, or more.

But for large stationary applications, why not lead acid? Weight and even size aren’t major issues. They’ve optimized the cost out of those, and in gazillion automobiles, even in accidents and fires, they’ve proven safe enough. And they’re almost 100% recycle-able. Now, they don’t have a long life and do require maintenance, so I could see some reasons for switching away from them, but it would have to be to proven technology for data center applications.

Yeah, that’s more like it. Solid state is not near-term. And there are lots of players in the space. How can we know which company will get the tech right first?

Thanks for your response. I just purchased the Audible version of Common Stocks and Uncommon Profits. I do some of my best thinking on “on the hoof” (ie, country walks,) so this will come in handy. With regard to the “30%” sell rule, I’ve been wondering how that would work. I assume it means to sell if the prices goes 30% below cost, rather than a simple 30% drawdown. But your point is well taken … your system is based on evidence so absent countervailing evidence, your system holds firm.

By the way, on August 28th ALAB’s CEO was interviewed at a Deutsche Technology Conference. The audio is available on Quartr. It left me feeling more bullish about ALAB than ever. Below is an excerpt from the interview, starting with a question by the interviewer, Ross Seymore:

“So if we bring it back to the ASTERA level, and think about Scorpio … That’s gone from basically zero revenues last year to I think low double digit percentage of sales this year and at least in my estimate is going to more than double again next year. Talk a little bit about the ramp we’ve seen thus far in the [Scorpio] P series and when the [Scorpio] X series kicks in and maybe just kind of frame the content increase relative to say a retimer that the company was originally built on.

Sanjay Gadendra: Yeah. So like I noted, we are … shipping the [Scorpio] P series, the PCIe switch for head node connectivity we started in Q2 for the Blackwell based platform. The Scorpio X series is something we’re super excited about. It’s going to completely transform the company because both from a business standpoint and also because these are anchor sockets, meaning if you are a system engineer at a HyperScaler, there are two devices you will care about during the first five minutes of starting a new design. One is the GPU, the other one is the scale-up switch, right? And then everything else is designed around it. For us, Scorpio X series makes us part of the conversation literally from the first meeting and right now we are having these conversations looking at not just the immediate generation but for the next two or three generations with our hyperscaler customers.

So it is going to be an important device or product category to provide that anchor around which we will build our business in terms of attach rate and dollar content. Like I noted with re-timers we were let’s say a little less than 100 bucks per accelerator on a given design win. We have graduated now to multiple hundreds of dollars per accelerator with the P series switch. And with the X series switch we expect that to transform to multiple thousands of dollars per device. So the path is going to be pretty, pretty significant if you think about just the attached content and the dollars that we will expect to see. This is a big market so we are pretty excited about what could happen.”

@Smorgasbord1 My investment is ELVA is based on who is winning in the marketplace right now and who has the better business model. It’s not based on guessing which future product is better.

Here are the numbers for the three main competitors of next-gen batteries

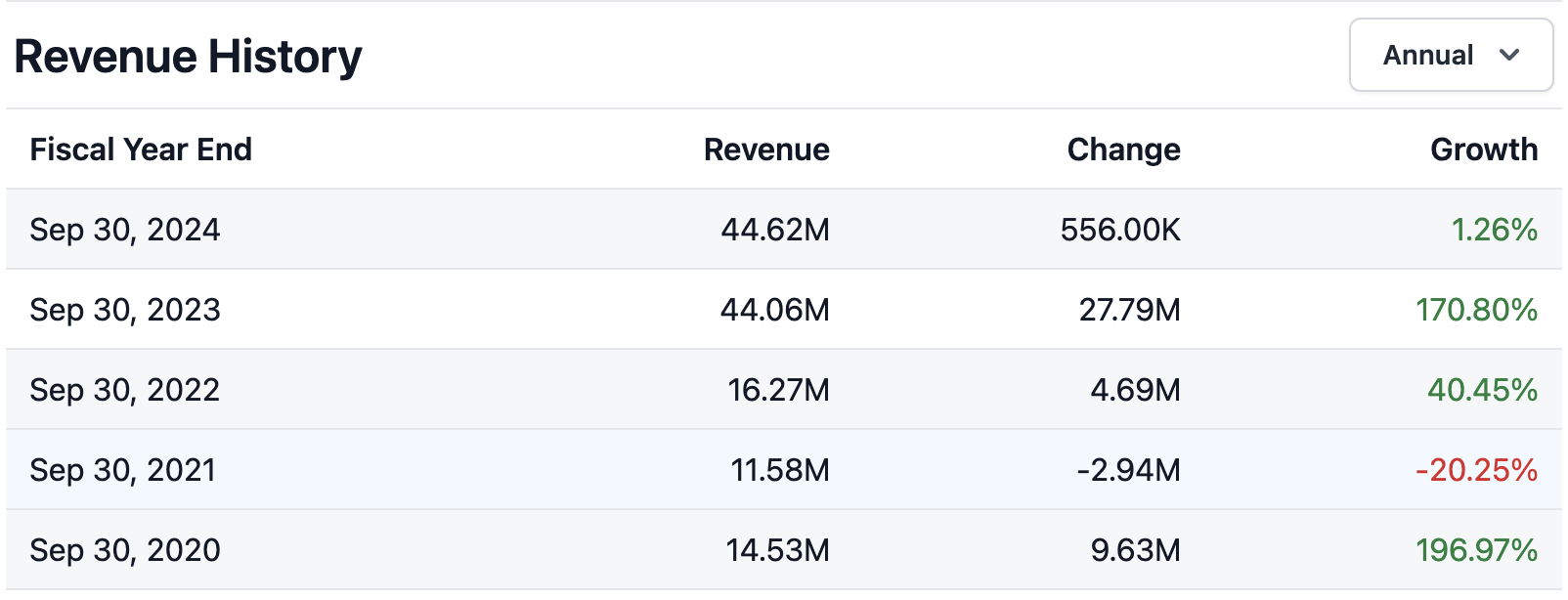

ELVA, revenue 17.1M +67% yoy, EBITDA 2.4M, net income 0.9M, gross margin 31%

AMPX, revenue 15.1M +350% yoy, EBITDA -5.8M, net income -6.4, gross margin 9%

ENVX, revenue 7.5M +98% yoy, EBITDA -34.9M, net income -44.5M, gross margin 26%

Yet here is how the market caps compare,

ELVA 254M, AMPX 887M, ENVX 1790M

Electrovaya’s competitors have less revenue, worse gross margin, and are a long way from profitability. That’s in addition to ELVA saying that the solid state batteries AMPX and ENVX produce are more niche products. Just getting comparably valued alongside its competitors would be a 5x+ gain alone.

@twillo I have been meaning to catch that Deutsche Technology Conference and saw the transcript has been out for a little while now. I really like Astera was able to release Scorpio and have it ramp up this fast. It seems like their product roadmap is extensive and they have the capabilities to react to the needs of their hyperscaler customers. Doesn’t hurt to have them being a leading member of UALink and literally setting what the next standard will be for AI hardware.

I wouldn’t say lead acid batteries are really safe. Batteries are inherently dangerous because its a storage of energy. I would agree lead acid batteries are safer than lithium ions but that’s because they are storing a lower amount of energy. Lithium ion batteries store 3-5x the amount of energy than lead acid batteries in a given volume.

As lithium ion technology matures, data centers are switching from VRLA (Valve-regulated Lead Acid) Batteries to Lithium Ions because you can replace a room full of batteries with a rack or two of batteries, this also reduces cooling costs, and maintenance costs.

I feel using 67% yoy is very misleading. In the LTM they had 54.9M (17.1, 15,11.2, 11.6) in revenue, the 4 quarters before that they had 49.5M (10.3, 10.7, 12.1, 16.4). Which had a YoY growth rate of 10.9%. Their 17.1M lines up with their lowest quarter of revenue in the last two years. My biggest concern is the volatility in their revenue.

If the company meets its guidance for Q4, they will be flat growth sequentially. The CEO mentioned they will beat guidance. Using WPR’s terminology, I see some yellow flags. With that in mind I’m going to take a small-medium position and watch how its revenue trends change in the coming months.

Electrovaya’s self-described market is “material handling battery systems.” What is the TAM for that market? Who’s winning? Established players are the lead acid battery makers, right? Alpine Power Systems make Li-Ion batteries for forklifts, too.

Electrovaya has been in this business for several years now. How fast is it growing?

Here’s an “article” on lithium ion batteries, showing things with “Toyota” labels. Apparently, this company sells and services material handling equipment:

Electrovaya admits their “core” market is the “material handling sector.” (Earnings Call link). They just “recently announced our entry into the airport ground equipment sector.” I do think there’s probably a lot of room for growth upgrading older forklifts to lithium ion, but I also suspect that requires a lot of retail outlets (like Conger, above) to convert their customers. What is Electrovaya’s relationship with the retailers? The way they talk about large companies suggests they’re going after large users of material handling equipment to sell them lithium upgrades directly. What is Electrovaya’s sales and marketing team, budget, etc for these efforts?

But, I suspect upgrading forklifts isn’t what attracts potential investors to the business. It’s all about the future. Which management talks up. As they said on the ER call: “eCommerce, robotics and defense are poised for rapid growth. We are particularly focused on the robotics sector.” They even talk about “autonomous vehicles…operating indoors” and “Some of the largest battery systems that we are developing are for Class 8 trucks.” “We are also working towards launching some specialized energy storage products later this calendar year.” and “Finally, we are also well on our way to launching multiple recurring revenue stream products in fiscal year 2026. This includes energy services and software based solutions.”

That’s a lot of different irons in different fires. What is the Class 8 truck thing? Here’s a PR article:

This is a battery swap model, not charging on the road, btw (watch the embedded video). Is this a growth business, and if so, what’s the expectations in terms of volume, time, and profit?

Everyone’s solid state batteries are niche or vaporware. Including Electrovaya’s. I reiterate my belief that to pick the business winner, you need to know which future product (solid state battery) is going to be better. And then who has the capital to produce them cost effectively, who has the business relationships to sell them, etc.?

The company’s market cap is only $265m. The 10th largest institutional holder has only $156k invested in the company, number 9 has only $295k. Those are retail investor type numbers. Many investors on Saul’s board alone could swing this easily. Has this thread itself moved the needle on the stock?

You’ve found some great opportunities in the past, but, sorry, I’m just not getting this one. And, I could easily be wrong here, too.

@drew1618t nice callout on the weak comp that ELVA was going against in the prior quarter which was 10.3M

I do agree it is a bid odd for a CEO to say “we will beat that guidance” as most management teams would give more of a hat tip in that scenario. Since management has flat out told us the guidance will not be accurate the next best bet is to look at what analyst’s are projecting.

For next quarter analysts are projecting 20M of revenue which would be +75% yoy and +18% qoq. It’s a fairly decent step up, and I would like to see them come above this number to have a lot of interest in continuing a position.

What is interesting after that, though is that two quarters from now my data provider shows they would get only 17M of revenue, or a -17% qoq decline in revenue from the prior expected 20M. This is where I see an opportunity because I seriously doubt this company is going to be posting a sequential decline two quarters from now based on how optimistic the transcript reads. Just listening to the CEO at the Midwest Ideas Conference has me convinced this is a huge growth story, but I could of course be wrong as well.

We believe we can continue this growth trajectory into the current quarter and beyond as we leverage continuing demand growth from our core material handling sector

and

During the quarter, we secured more than $21m worth of orders, bringing total orders to over $65m in the nine months ending 06/30/2025. This steady order flow is backed by a much larger pipeline of projects

CFO said:

Further revenue growth, which we have line of sight off for the rest of the fiscal year, will further contribute to increased overall profitability.

So, yeah, management is positive on the future of their existing forklift style battery business. Is that why people are interested in this company?

I am more interested in the zero accidents and large amount of cycles for it’s batteries. The technology that they use in the batteries for forklifts will transition easily to other high cycle high load industries.

Batteries are important to this world. Would you pay 60% more for a battery that won’t catch on fire and live twice as long as the competitors?

@Smorgasbord1 I will look to spin off an introduction thread about Electrovaya coming up. A lot of points to cover in the monthly summary thread and will look to address those questions and concerns you raised.

One more document worth checking is with the CFO on June 3 for a “Special Call” or investor tech conference.

Some added notes, a lot of them from the Special Call,

The company is HQ’d in Mississauga or basically the Toronto general metropolitan area, and it’s dual listed on the TSX and Nasdaq. It does not have a big institutional following which I like because if they keep delivering results it will eventually attract institutional interest.

They currently have 300 MW electricity online in Mississauga, 300 MW is coming online in Jamestown NY around April 2026, expanding to 1000 MW by the end of 2026, and plans to scale up to 3 GW longer term. Keeping in mind this amount of electricity they are bringing online is the same as both CoreWeave and Iren plan to bring online. It’s hydro-electric and very cheap electricity, they cite the same 0.05 kWH rate which Iren has advertised as being world leading.

Electrovaya batteries for industrial forklifts seems to make up about 2-3% of the US market and 5-7% of the Canadian market, biggest competitor is EnerSys ENS making up about 28-32% of the market according to AI.

Walmart Canada alone has placed 7M CAD worth of orders in 2025 (Both Toyota and Walmart seem interested in promoting this company, two great customers to have)

Batteries for industrial robotics is just starting to kick off, and they are also targeting defense, commercial vehicles, and airport ground equipment, along with energy storage.

Getting into heavy duty construction and mining vehicles, designed with one of the Japanese OEMs

Three competitive advantages: safety, longevity, domestic supply chain

Comparing in phones they lithium ion battery there does 1000 cycles, where their battery does 10,000 to 15,000 cycles (guessing phone companies don’t want this though it seems because it would kill part of their upsell cycle)

They do admit “lithium-ion batteries have had a checkered history”, cause of thermal runaway or chain reaction, people familiar with phones overheating

Technology is a polymer separator, stable at high temperatures, cells pass “the most stringent safety testing”, including “nail penetration testing”

The technology is “chemistry agnostic”

“If you put our battery in an electric vehicle, you’ll do over 3 million miles in that electric vehicle, maybe you don’t need that there”

Robotics or forklifts in the warehouse do more cycles that a car, so they need more performance, car is 1-2 cycles per week while warehouse applications are 2-3 cycles per day

“In terms of of addressable markets, these are large markets. Material Handling, Warehousing in general, it’s very quickly growing, especially with further proliferation of e-commerce”

Powering over 200 warehouses across multiple continents, operating 24 hours a day

“In terms of customers and partnerships, we probably have as blue chip a roster as you could have”

Launching a product in ground support equipment, deployed next month at a major airport (implying July)

Opportunity to deploy an intelligent AI Demand Response System, “gets us into virtual power plants”, “SaaS-driven revenue generation model”, looking to get 10% of revenue from recurring streams by fiscal 2027 (this is admittedly not a revenue driver for the near term)

“Seeing so much activity coming out of Japan”, planning to launch an operation there, “and that will be announced when it will be announced”

Jamestown is “friend-shored”, very domestically orientated, 51M loan from Export-Import Bank, strong incentives from New York state and the county, significantly below market rates on the interest rate, flexibility on CAD vs USD, can pick and choose the interest rate wanted

“we’ve increased our total assets and decreased our liabilities at the same time, increasing shareholder equity considerably by almost 3x in the last 12 months”

2009 focus was auto, supplying Chrysler and Mercedes Benz, supplying auto is intensively competitive, continuous cost reduction is main objective, very difficult to compete against “Asian players”

Infinity battery technology, CEO “There’s nothing really quite like in the market”, “it’s getting recognized now”

Asked about Aspen Aerogels, ELVA product stops runaway thermal in the cell, “you don’t need to use Aerogels”

“We’re not targeting the Auto space because of the margins available”

Toyota Material Handling is building a new plant in Indiana, spending hundreds of millions to increase capacity for electric forklift production, “TAM for the core Material Handling market is large and growing”

“We have our batteries in a number of defense applications already”, takes time for these applications to scale up

Grid scale storage systems were dependent on Asian battery systems with safety hazards, especially being located near new expensive distribution centers

Not involved in actual chemical procurement, procure materials from large corporations

“Electrovaya’s battery products are not commoditized, so movements in commodities do not really affect our margins nor our sales price”

Made the leasing market very competitive for Toyota, “driving a lot of new business our way”

Energy as a Service, “we’re starting to see opportunities to scale that where an end customer will want to take a battery, but pay for it as they use it”

Lithium price movements have very little bearing on overall cost or sale price of units

“We’re quite happy to lose bids if it comes down to cost. We have a very robust pipeline of orders already and a growing - and that’s growing every week”

100+ patents, continue to file patents, 4-5 new ones under review

Targeting around 40% gross margin, more important is generating strong EBITDA and net profits

Oldest battery in the field is 7 years old, out lasted the forklift and moved to next forklift, lost less than 5% of its battery capacity during that period, do provide a warranty as its a good accounting practice, not seen any significant claims

Initial bill in Congress has 45X incentive staying, restrictions against relying on China which ELVA does not, production tax credit will benefit production from Jamestown

NO. You’re dropping the “h” from the units, which stands for hours.

It’s not 300MW, it’s 300MWh.

It’s not electricity generation (power units), it’s battery capacity production (energy units). MWh, not MW.

It’s the sum of the capacity of battery production they hope/plan to have online next year; as in ‘take the storage capacity of every battery made during a year and add that capacity up.’ It’s got nothing to do with electricity generation.

That has both the annual battery capacity projects, as well as a separate note that their Jamestown plant uses “low cost hydro energy (~0.05/kWh).” But, don’t conflate those two.

Again, note the units for “production capacity” are in all kWH, MWh, or GWh - they are all energy, not power.

Not comparable, nor relevant to CoreWeave nor Iren, except if those companies want to install some batteries to keep their data centers running.

Again, are you investing in a forklift battery company for what it is today and how it’s growing today - or are you investing in the narrative of future solid state products for a future robotics market? Could be both, but understand these are separate technologies with very different time and risk profiles.

Wow, this clears up a multi-year misunderstanding I’d had regarding electricity! I thought the ‘h’ was optionally silent or some companies wrote that notation with the ‘h’ and others did not.

Two years ago when I was interested in Amprius they had mentioned they were scaling up to a GW, but now I see that was a GWh. This was confusing because when I was reading about IREN and they were saying having ~810 MW online is massive, I was thinking it does not really sound that big. My conclusion was that Amprius was delusional about scaling up to a GW, they were all talk. It makes a lot more sense that now that Amprius is aiming for 1 GWh.

I’m still wrapping my head around this, but some examples which helped explain it more,

If a 10 MW plant runs for 1 hour, it produces 10 MWh of electricity

Power (MW) * Time (hours) = Energy (MWh)

MW is for power capacity at any instant, MWh is for total energy over time

MW can be thought of as “speed” or MWh as “distance”

Lastly, I was asking AI about how much MW is a facility which produces 300 MWh. It seems like it’s maybe 1/10th or if they run for 10 hours in the day. Meaning we do 300 / 10 = 30 MW, or the Mississauga facility is probably in that range for Power (not energy).