Well we seem to be off to a good start, at least. It was my first month in the green in what feels like forever. Let’s hope the Fed doesn’t spoil it later today…

Here’s what I did in January:

I sold most of my SentinelOne shares and reallocated it to my top 4. My thinking about S has changed a bit after looking at someting which does not often get looked at in detail on this board (and almost all of our companies exclude this from their commentary), namely gaap operating profits and SBC. Now why look at that? Because SBC is a cost to someone and it needs to be taken into account in one’s thinking in some way (I think we all agree on that - we just have passionate debates about whose cost it is). So, either you include it in your thinking by thinking through the dilutive impact of SBC (i.e. you think about it as a direct cost to shareholders, which it is, actually). Or you incorporate it into a company’s expenses as GAAP dictates, which makes hiding the ball more difficult for management teams and makes comparing companies easier.

First, dilution: S’s weighted average share count was up 7% in the last 4 quarters. That’s quite a lot. More than most companies we follow I believe.

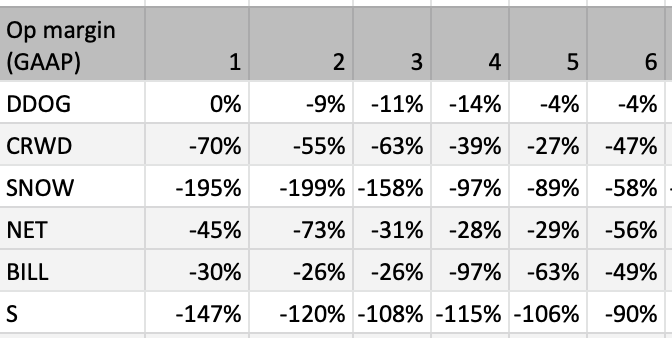

Next, gaap operating margin (so this includes expensed SBC according to the way GAAP requires). Here I’m comparing S to other companies in my portfolio, but I’m starting the comparison at the point where each company had revenues below $50m (it’s roughly $45m for all companies - that’s the first column in the table below):

So vs my other portfolio companies, at similar stages of growth (i.e. the 6 quarters starting on the one in which each one had revenues of ±$45m), S is in a league of their own ito how opex & SBC intensive the business model is: with a negative 90% gaap operating margin last Q (vs better for all of the others).

Now normally that wouldn’t need to be an issue per se. But in our current environment where profitability has become relatively (vs 2020-2021) more important than growth that’s a big deal. So to offset that negative, revenue growth really must be flying, like SNOW’s was at that point in time. However, I’m not sure that S is in that spot - we all expect that revenue growth will slow, and management said the same thing.

Now I don’t think S will crash and burn - I’m not going on an S bashing here. The company is founder-led, they’ve got more than enough cash on hand to easily handle the cash burn for many moons, their revenue is still growing exceptionally fast and they are improving their operating margins each quarter. I still believe all of those things. And it is really cheaply valued. However they may be forced to guide lower for next year than what they previously implied, or they may only just miss the implied ARR growth for this coming quarter (they did last quarter) or they may not be able to pull the breaks on opex fast enough (especially SBC may be expensive for them as their share price has tanked so much).

So I simply came to the conclusion that I do not want such a big position in S at the moment as I had prior to this. I think the stock could really take off given its exceptionally low valuation relative to its growth - but I’m not as sure as I was before. And I’m more sure about my top 4 positions. Hence I significantly lowered my position in S, however what I retained is leveraged with options. If it does take off I should benefit a lot. I’ll wait for earnings and reassess. I’m not writing this one off.

My 2023 results

January: +7.2%

Yay! It’s a psychological win after last year. I’ll take it - volatility and all.

Portfolio composition

| Company | Ticker | % of port |

|---|---|---|

| Snowflake | SNOW | 23.3% |

| Cloudflare | NET | 22.7% |

| Datadog | DDOG | 21.2% |

| Bill | BILL | 20.0% |

| Trade Desk | TTD | 5.1% |

| Transmedics | TMDX | 4.6% |

| SentinelOne | S | 2.9% |

| Crowdstrike | CRWD | 0.2% |

| Cash | 0.0% |

Individual companies

Snowflake

Snowflake announced plans to acquire two companies in Jan: Myst, a small company, probably acquired for the talent and mobilize.net which has upward of 200 employees on LinkedIn and which helps with migrations from legacy DB’s to Snowflake. From their website:

SnowConvert from Mobilize.Net can unblock your move to Snowflake from Teradata, Oracle, SQL Server, Apache Spark and more. Our automated migration tools can reduce the effort needed to migrate SQL procedures, scripts, and tables by as much as 88 percent. Our analysis tools can help you extract all your data warehouse code and understand the level of effort—as well as any potential issues—to migrate that code to Snowflake.

I believe that Snowflake has enormous further potential to grow average revenue per customer in its G2000 base, and that many of the workflows that SNOW enables will not get cut in a downturn. My view is therefore that SNOW should continue to see outsized relative growth compared to just about any other company out there at this scale. They will also start pumping out a lot of cash simply by curtailing hiring. I’ll be watching the CF number and NRR with a lot of interest when they report.

Cloudflare

In January they won a $7.2m CISA contract and Palantir announced a strategic partnership with them. Given that Palantir’s bread and butter is Government work, this seems to bode well for Cloudflare’s inroads into winning more work as the US Government upgrades its technology and security.

I believe that we may get strong - perhaps very strong - cash-flow numbers from Cloudflare in the ER on 9 Feb. Given that they promised to get to CF positive territory this financial year and this is their last quarter to make good on that promise, I’ll be watching that FCF number like a hawk.

Bill

Nice short name. Getting used to dropping that .com ![]() Last Q the standout achievement was the huge number of new customers they managed to sign up. This quarter I’ll be watching to see how much that has translated into revenue. Last quarter subscription revenues were up only 5.3% and transaction revenues up 12.1% sequentially, with float revenue creating the nice tailwind to margins and the bottom line, fuelled by higher interest rates. I’ll be looking for a continuation of that story this quarter (and hoping that subscription revenues do not deteriorate further): relatively subdued subscription and transaction revenue being boosted by outsized float revenue falling to to bottom line for as long as the Fed holds rates high. A nice hedge in the business model. I’ll be looking for mid 60% revenue growth yoy. ER coming up tomorrow - looking forward to it!

Last Q the standout achievement was the huge number of new customers they managed to sign up. This quarter I’ll be watching to see how much that has translated into revenue. Last quarter subscription revenues were up only 5.3% and transaction revenues up 12.1% sequentially, with float revenue creating the nice tailwind to margins and the bottom line, fuelled by higher interest rates. I’ll be looking for a continuation of that story this quarter (and hoping that subscription revenues do not deteriorate further): relatively subdued subscription and transaction revenue being boosted by outsized float revenue falling to to bottom line for as long as the Fed holds rates high. A nice hedge in the business model. I’ll be looking for mid 60% revenue growth yoy. ER coming up tomorrow - looking forward to it!

Datadog

With Datadog the thing that became more important to me this month is the long history this company has of extremely efficient growth. It has a fantastic business model. Frictionless sales motion coupled with hugely impressive innovation cadence. No other company that I follow has managed to grow this fast this big with so little cash burn.

They have a usage-based revenue model, so will likely see some further pull-back from the 7.5% sequential growth of last Q, but should also see acceleration once “the macro” abates. For the coming ER on 16 Feb I’ll be looking to operating margins bouncing back from the relatively low 17% they hit last quarter and looking for revenue growth in the mid 40%'s.

The Trade Desk

The key thing that impressed me in the last quarter was the extent to which this company gained market share in an otherwise depressed and volatile digital ad market. While posting strong financial numbers: EBITDA margin of 41%, net profit margin of 33% and operating cash flow margin of 35% is just great. For the coming ER I’m hoping for an acceleration of growth from the 31% reported last Q, fueled by political ad spending, but will focus more on comments around market share gains, as was the case last Q.

Transmedics

Transmedics guided to $22.9m revenue for next quarter which would be a 11% sequential decline (still good for 136% yoy though) but with analysts, probably cognisant of how much management has low-balled guidance in the past, averaging $24.5m. I’ll be looking for something much closer to $30m. Let’s see. This company could be explosive and that’s probably why @XMFRob has it as such a big position. I’m very tempted to increase my position but don’t know what to reduce in order to buy more!

For those not familiar with the company, they put out a new investor deck on January 12th. Highly recommend squizzing through.

Finishing up

Things can only get better this year, right?

Good luck, all!

-WSM