Hi, I’d love to start a discussion thread for Zeta Global ($ZETA).

Brief Overview of the Company

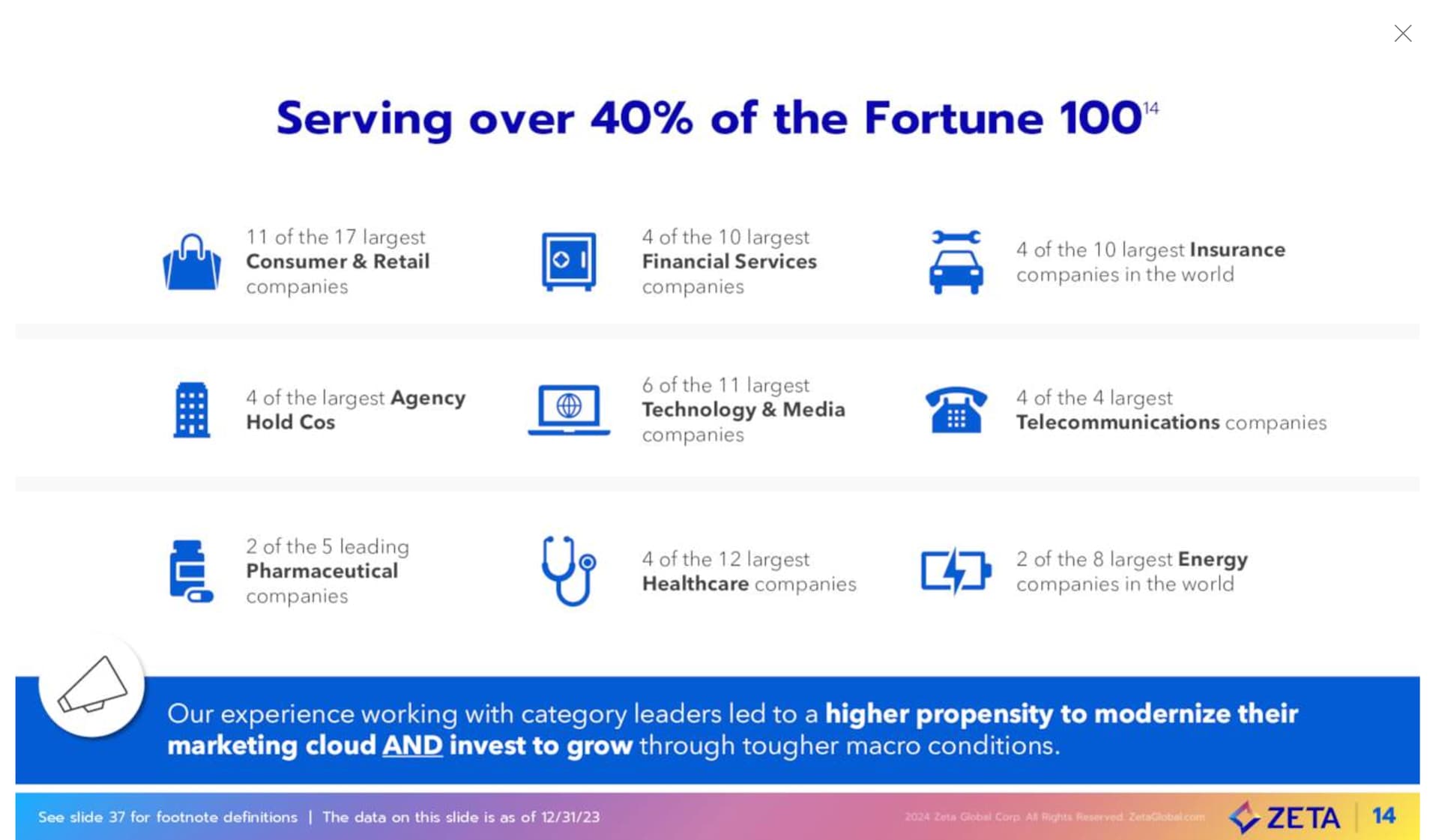

Zeta Global is a data-driven marketing technology company that leverages advanced analytics and artificial intelligence to help brands acquire, engage, and retain customers. Its platform integrates customer data management, marketing automation, and analytics to deliver personalized marketing campaigns across multiple channels, including email, social media, mobile, and display advertising. Operating on a subscription-based model, Zeta Global provides businesses with access to its suite of marketing tools and services, enabling them to enhance customer experiences and drive marketing effectiveness.

Quarterly Revenue

$210.3 → $194.9 → $227.8 → $268.3 (guidance was 241.2) → $297 (Q4 guidance)

YoY growth:

20.10% → 23.67% → 32.6% → 41.96% → 41.23% (Q4 guidance)

Organic Revenue Excluding Election Related:

$210.3 → $194.9 → $226 → $247

20.10% → 23.67% → 31.55% → 30.69%

So even excluding the impact from political spends, the YoY growth still accelerated to and stabilized at above 30% starting Q2 this year. The company attributed this success to the adoption of their Gen AI products. In Q2 earning call

the vast majority of our customers are now actively using our Gen AI products, I believe it is a direct result of the 22% ARPU growth of our existing customers. We are seeing customers that use it, scale substantially faster than customers who have not adopted it yet in utilization fees and increasing their contractual relationships with us.

Other Information

Zeta is FCF profitable with TTM FCF / share being $0.45 / share. So with the current share price of $22.9 today, TTM Price / FCF is ~51.

GAAP net income has been improving and close to break-even.

The diluted EPS for the last 4 quarters are:

(0.22) → (0.23) → (0.16) → (0.09)

NNR is within the company’s long-term expectation: 110% ~ 115%

In Q3 earning:

Strength was broad-based, on a year-to-date basis, net revenue retention is at the high end of our 110% to 115% model.

The insiders seem to be very confident on the company. According to Robinhood’s data, insiders purchased 387k shares in November with 0 shares sold. Among the purchases, 7 purchases were “Informative Buy”.

Zeta was attacked by a short report, which was why the share price dropped significantly from the ATH at November 11th. But the company has responded to the report very positively saying that the report was false claim.

Today, the share price dropped by more than 10% again without any reason. Seeking Alpha said that it was related to the announcement of a merge between two ad agents who are both Zeta’s customer. But the CEO has responded and believed that it should be positive for Zeta:

Expanding on my earlier comments, we are proud of our extensive relationships with the top Holdcos, including both Omnicom and IPG, and believe that today’s announcement is a positive one for the industry and Zeta

With the strong business performance and insider stock purchases, I believe the company is doing pretty well and the share price drop recently was an over-reaction and was a great opportunity to buy the dip. Zeta appears to be undervalued with a TTM PS ratio of ~6 and a TTM P/FCF of ~51.

Long ~6%

Luffy