“We’re doing coal. I don’t want windmills destroying our place. I don’t want these solar things where they go for miles and they cover up half a mountain and they’re ugly as hell.” - Trump

Coal is beautiful, clean… Solar is ugly and windmills are destroying the country… Some people can peddle nonsense for a very long time. Power to them, not to the people…

I had previously sold some puts and calls, and have since closed those positions opportunistically. For now, I’m holding steady and not making any new moves.

If the current Senate version of the bill passes, buying $AES at around these levels—with a 6.5% dividend yield—could turn out to be a solid play. That said, the details matter, and I don’t fully understand the nuances of how the tax code specifically affects $AES. My view is more high-level, and it appears favorable at this point.

I’ll wait for the Q2 results and for the final version of the bill before taking further action.

$AES is exploring strategic options, including potential sale. The stock moved up 15% in after hours and at one point moved above $13 and now trading at 12.65.

May be going private is better for the company to move out of public eye and allows them to sell certain assets, eliminate the dividend and bring additional capital to expand capacity, become 100% renewables and wait for the next administration.

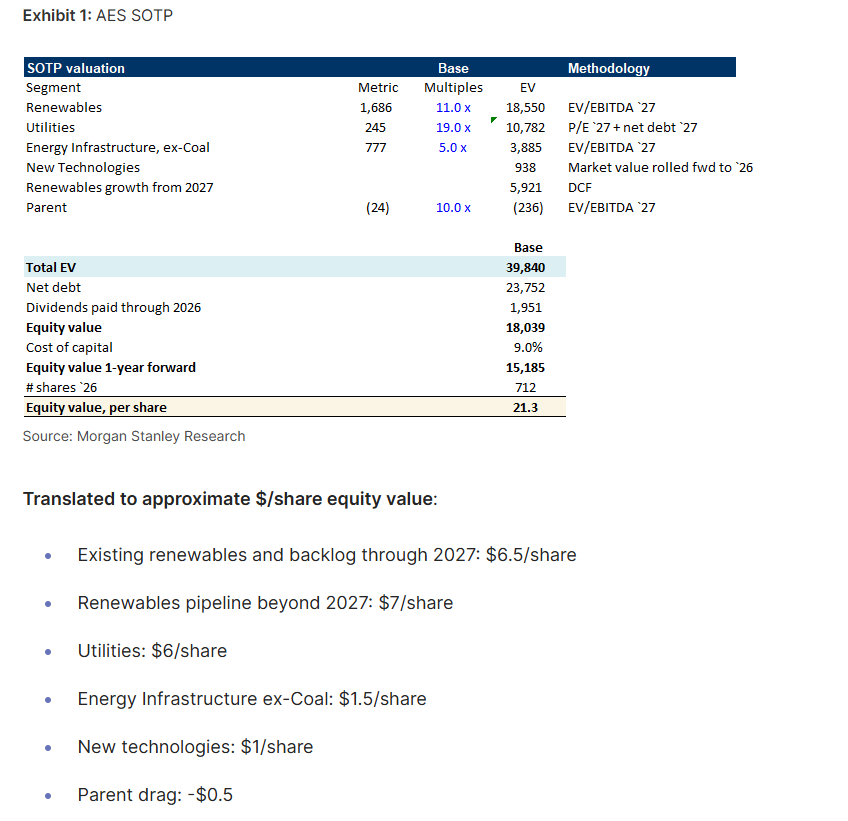

Currently there is lot of fear priced in, under normal environment, the stock should be trading much closer to $20.

I have sold some covered calls, that sucks, but luckily it is just 10% of my $AES holdings, so not that bad.

Today Morgan Stanley came out a research report where they shared their sum of the part valuation estimates and the assumptions within that.

May be MS is not part of the deal. Also, MS had a high PT all along, so they may be they are trying to set some floor for the deal price. Coincidently, today $AES moved up 2.75%. My own expectation is if $AES is taken out, it will be at least around $15+.

I still believe, AES is a leader in the solar, AI needs lots of electricity, and Solar is the quickest way to generate electricity, and it is environmentally friendly.

But, the Trump administration attack on Solar is relentless, even though it is head-scratching and IMHO a very, very dumb policy position.

I have sold additional Aug covered call, instead of rolling them, I let those stocks to be called away, and reduced my overall position by 50%. Assuming the profits and dividends, my cost basis is now $8.5 and the stock is paying $0.7036 per annum. There is still a buyout possibility. I will for now hold the remaining shares.

For all those who cheer for coal… be prepared to pay more for electricity. Elections have consequences, policy choices have consequences… stupidity has consequences.

The stock has been trading within a range since the last post, and is now showing signs of a potential breakout. The impact of most regulatory risks is now known and has been priced in. I’ve sold the $13 puts, as I believe there’s a possibility of the situation improving, including a potential buyout. I am prepared to be assigned the shares.

I am trying to work out what is parent’s debt and what will be takeout price… but quick math shows the price should be around $16~$18…

BlackRock’s Global Infrastructure Partners LP is set to acquire power company AES Corp. within the coming days for $38 billion, the Financial Times reported, citing people familiar with the matter who weren’t identified.

When you find a company that is having some short-term issue, in the case of $AES, there is no real issue with the business, but a president who just happens to hate renewable energy, one individual whose sway is dictation the fortunes of the industry, and likely that will go away in few years, and in the meantime, the company has enough existing business and future business for the next 3 years are secured, has a low stock price…

Step in private equity, it takes out the company cheaply, and they can eliminate the dividend, instantly the company can save $500 M cash, which they can use to continue to plough into the business, keep expanding without worrying about profitability, even shed some more business, get a good payout in the form return of capital, then after the administration changes, bring the company public at nice premium…

Under normal circumstances this company should be trading between $20 ~ $25, but here we are…

All the time you spend on learning about company, it is not a simple and easy structure, this is a real hairball, are wasted.

So in the end, you don’t know whether to feel happy if it is taken out at $16 or so or feel bad…

The last week sudden revelations of “opacity” in PE, and given this deal is going to be between $35 ~ $40 B, a sizable deal, the corporate structure of AES with its gazillion subsidiaries, international operations, public utilities and PPA’s with AI players like $AMZN, $META are now suddenly risky!!!.. is a hairball. The chances of this deal getting further delayed is a high possibility.

If the stock price goes below $13, towards $12 on this, I will be buyer.

Another quarter of solid execution. The management re-iterated guidance from 2025 to 2027. They are guiding 5~7% EBITDA growth, since tax credits are lumpier, EBITDA is the preferred method. The EBITDA guide is slightly above current estimates. Renewables IRR 12~15%. Most importantly the management mentioned there is no need for them to issue equity, this was one of the major overhangs, of course they have scaled down the growth plans as part of the reset few quarters ago. The cost reduction actions taken as part of the reset is started flowing through the results. As part of the reset company said, no dividend hike planned till 27, and I am not expecting any buybacks either.

Overall, execution is good, company seems to be turning around. Either they go private or even if they stay public, the multiple re-rating is a higher possibility.

I initiated some covered call because the premiums were good, due to takeover rumor. I will not rotate them as they expire, and will maintain 1% allocation and sit back.