$AES moved up 11.66% ($1.21) on Friday on 5~6x volume after earnings. This is an energy company not a SW company the move is significant. The below chart shows how high the volume is.

So Why the stock moved up so significantly? was the earnings were out of the park? No. What about the guidance? The management reiterated their guidance for 2025 to 2027.

At first quick look at the earnings presentation, I didn’t catch it. Subsequently, on seeing the price action, volume and absence of any analyst notes subsequent to the call, I was intrigued and spend the weekend listening to the conference call multiple times and read the transcript to catch the changes.

Some context, In 3Q conference call Bank of America analyst tangled with the management and challenged them and subsequently she slapped a sell rating with $11 price target, the stock declined and went below $10 on Feb 18. Separately she is absent during 4Q call. It was bit surprise, as she had published a note of what she is looking to hear in the call

In this post, $AES: AES Corporation - #2 by Kingran I have highlighted her concerns.

In summary, Investor Concerns are:

- policy uncertainties

- renewable EBITDA growth

- balance sheet and funding constraints

To address the concerns the company is taking the following steps:

- reducing current investment in renewables by focusing on the highest risk adjusted return projects,

- improving organizational efficiency

- continuing to operate some of the energy infrastructure assets.

As a result

- Credit metrics will improve over time, maintaining IG rating

- Eliminating the need for issuing new equity

- Dividend will be maintained till 2027 (no increase) but committing to dividends

- Growth post 2027 is going to slow

Let us discuss each of the actions, I will skip reviewing 4Q and utilities, so as to focus on the changes and what it means to the stock.

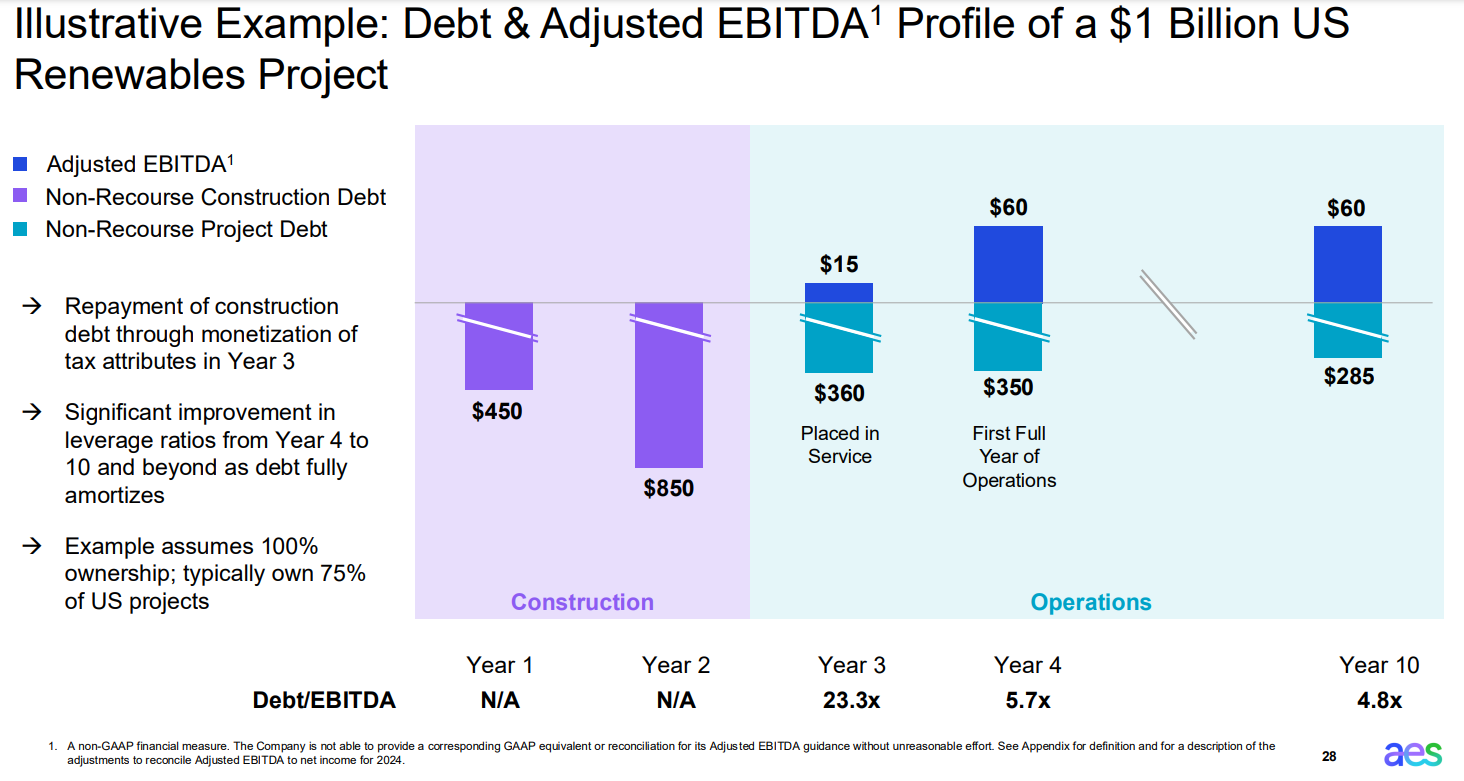

Renewables Investments

as profitability of each megawatt of new PPA sign has substantially increased we do not need to bring online as many new projects

with that one sentence, basically the company declared they are abandoning their ambitious growth plans and going to focus on executing the existing pipeline.

The pipeline development expenditure runs through the P&L now, it takes time to sign the PPA, build and then eventually start producing revenue. That lag is impacting the credit metrics. By cutting down the pipeline development, they are reducing the expenses today, which will help the credit metrics.

- Resizing (from 25~30 GB by 2027 to 18 GB) will reduce Parent investments by $1.3 billion through 2027

- Reduced pipeline development expenses lead to cost savings (they have 50 GW pipeline in US and 10 GW outside US)

- Focus on executing, bring 12 GW online by 2027; 3.1G expected to come online in 2025; 7.1 G additions during 2026~2027

- AES has $4 ~ $5 B construction debt, think of it as a pool as projects come online, the construction debt is paid by tax credits and replaced by project debt and the new projects will become part of the pool; This debt pool is not really earning anything, is hurting their credit metrics and also limits their ability on executing multiple concurrent projects

- The key is they are scaling down their ambitious plan; After tap dancing and avoiding answering directly in earlier questions, at last the CEO said below

Yes. I would put it this way. Post 2027, what we see is less growth in number of megawatts than our original plans.

Improving organizational efficiency

With reducing the pipeline development effort and layoffs, 10% of workforce

- will result in $150 M cost savings in 2025, and $300 M in 2026.

- This is run rate and not one time; The actions are already taken, so very high confidence in achieving these numbers

Energy infrastructure assets divestments

- Compared to initial plan, the company will operate some coal plants

- Original guidance is reduction of $750 M EBITDA from coal plants; now they expect at least to have $250 M EBITDA coming from coal

- These plants are mature, debt is amortized; very acreditive to credit metrics; (I guess the main driver)

Policy uncertainties

- Essentially all solar panels, trackers and batteries either in-country, or contracted to be domestically produced for US projects coming online through 2027

- Safe harbor protections for nearly all 8.4 GW of projects in US backlog; 30%, of backlog in international markets, primarily Chile, which are unaffected by US policy

- The below shows, the EBITDA generation viz-a-viz capex requirement; without tax credits these projects are not viable at current power price;

Balance Sheet and Funding

- The company expects $150 M saving in 2025, and $300 M run rate savings which helps

- In addition to reducing pipeline development activities, company expects to execute more development transfer agreements, thus reducing the AES equity in those projects

- The refinancing of maturing debt is not expected to have any impact on the interest rates as they have rate hedges in place

- They are planning to operate few coal plants, which will result slower EBITDA decline in energy infrastructure SBU; contributing to the credit metrics; These coal plants are mature assets with amortized cost;

- The company is increasing the rate base in Ohio and Indiana utilities by 20%; They have already invested $1.6 B and this should help DPL (Dayton Power & Light, which is a subsidiary of AES Ohio, which is a subsidiary of AES) achieve investment grade rating.

- This new plan could lead to debt to FFO to 4.5, < 5x; If this metric stayed above 5x sustained basis, that would lead to credit downgrade;

- The company projects $800 ~ 1200 M asset sales; Still this is a risk and may result in equity issuance (a risk); Management mentioned the changes eliminated the need to issue equity;

Lastly, it seems the company was facing rating challenges in the next review and basically with these actions they are hoping to retain their investment grade rating, which is essential for their funding.

Guidance

- 2025 adjusted EBITDA of 2650 m to $2,850 m

- Parent (AES) free cash flow of $1,150 m to $1,250m

- Adjusted EPS of $2.1 to $2.26

- Reaffirming all of long term growth rates, including 5% to 7% adjusted EBITDA growth through 2027.

- Expected to close 30% AS Ohio sale; Raise $400 ~ $500 M from asset sales

Other

- Today 50% of portfolio is renewables

- US focused growth

- Reduced international footprint

In conclusion, the profile of the business has changed. They have cut down their ambitious growth plans; This new plan allows them to operate within their means, execute asset sales at their convenience, and avoid dilution.

Now, you have $AES producing $2 EPS, and $.70 dividend per year on a $11.6 share price. The questions are:

- Will these reduction in uncertainties, lead to stock price rerating?

- Will the post 2027 reduced growth plan hurt the stock price?

- The lack of dividend growth hurt rerating of the stock price?

For now, I have my position in and waiting to see analysts report.