Amazon Will Benefit From Growing E-Commerce Market Even With Loss Of Market Share $AMZN

http://www.seekingalpha.com/article/4028105

It will be interesting to see how this shakes out in the long term.

sjo

Amazon Will Benefit From Growing E-Commerce Market Even With Loss Of Market Share $AMZN

http://www.seekingalpha.com/article/4028105

It will be interesting to see how this shakes out in the long term.

sjo

Market share: 31.1 → 30.9 (-0.643%)

I fail to see how a rounding error is important enough to base an article on it.

Denny Schlesinger

Good catch Denny. Thank you.

sjo

Isn’t the point of the Seeking Alpha article more specifically AMZN’s profit margin as it was last year and this year vs what the other retailers did to their profit margins to increase their market share for this cyber sale time period. In addition, how much more of an ongoing/regular flow of revenue from internet sales AMZN has throughout the year vs. the other retailers. Isn’t AMZN coke and the others Pepsi?

Isn’t the point of the Seeking Alpha article more specifically AMZN’s profit margin as it was last year and this year vs what the other retailers did to their profit margins to increase their market share for this cyber sale time period.

I confess that initially I never read past the rounding error. Based on your question, I went back to read the whole article. It’s a blind man feeling up an elephant.

I took the numbers provided and did some analysis. They report that ten companies took just under 60% of online sales. Amazon’s share is more than the next nine, all well known brands. Amazon’s share changed by less than 1% while Apple jumped 67% and Walmart dropped 20% If you eyeball my list you’ll see that high ticket items increased in online market share while low ticked items dropped. Amazon is in the middle. People worry that Walmart is going to eat Amazon’s lunch. Not according these numbers.

If you think about Amazon’s business, how much, percentage wise, could Amazon discount over Apple products? Would you go to Amazon to buy big ticket Apple products? (I wouldn’t). But small items in another story and that’s Amazon bulk of the business, the so called “long tail.” Seen in this light it is easy to understand why Amazon’s share remains unchanged while more some specialized competitors lag or zoom ahead. It’s definitively NOT Coke vs. Pepsi.

**Company 2015 2016 Delta Delta %**

AAPL 0.9 1.5 0.6 66.67%

BBY 6.1 7.4 1.3 21.31%

KSS 2.3 2.7 0.4 17.39%

HD 1.1 1.2 0.1 9.09%

TGT 4.3 4.4 0.1 2.33%

AMZN 31.1 30.9 -0.2 -0.64%

Macys 3.4 3.2 -0.2 -5.88%

Nordstrom 2.7 2.5 -0.2 -7.41%

J. Crew 1.6 1.3 -0.3 -18.75%

WMT 5.1 4.1 -1.0 -19.61%

**Total 58.6 59.2 0.6**

The numbers presented in the article allow an interesting examination of the online market and instead of doing that the author gets lost in trivia:

For now, e-commerce growth will overcome slight loss of market share,

Doh!

but it does point to concerns over the “why” of that loss of share, and the long-term performance of retailers that are losing it.

How to think of e-commerce growth and online market share

With e-commerce growth going to continue at a hefty pace over the next several years at least, investors need to understand this isn’t a zero-sum game. Not only is that true if market leaders continue to grow share, but also for those that may be losing share.

Did not address what these concerns were, as far as I can tell.

ONE THIRD of ALL online RETAIL! Now, that’s a lovely worry to have!

Denny Schlesinger

Going past the article, the table I presented shows that people are buying more big ticket items online at a faster clip than lower ticket items. This is corroborated independently by off-price retail stores like Ross that don’t sell online. One also must think about the Walmart customer who might not have a credit card to buy online with.

I keep thinking that understanding the business model is more important than slicing and dicing numbers. This is one of my complaints against value investors who rely too much on numbers while not enough attention is paid to the big picture, the business model.

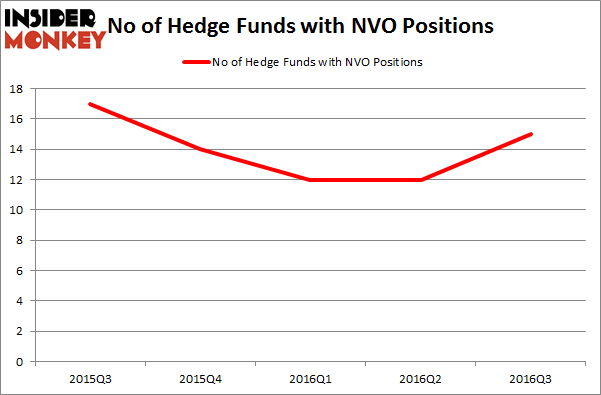

Recently I had an interesting experience. Novo Nordisk (NVO) cratered based on adverse news falling from an all time high of $60.23 to a low of $30.89, a drop of 49% (ouch!).

http://invest.kleinnet.com/bmw1/stats35/NVO.html

Being long I was watching events unfold. TA said to sell at $42 (support back in Jan/Feb 2015) but the business model said the company was too well run, too profitable and there were no signs of the obesity epidemic going away any time soon. So I decided to hold on. Over the past few sessions the stock rebounded to $34. This morning I discovered that hedge funds are buying up the stock after having divested through the first quarter of 2016

http://cdn2.insidermonkey.com/blog/wp-content/uploads/2016/1…

The article

http://www.insidermonkey.com/blog/novo-nordisk-as-adr-nvohed…

How does this differ from 3D Printing that got Saul all riled up? The business model of 3D Printing sucks except for niche players like Arcam which was bought out by GE. I wrote several TMF post on my reasons for not investing in 3DP.

GE Announces $1.4 Billion Investment: Acquisition of Arcam AB and SLM Solutions

https://3dprint.com/148290/ge-acquires-arcam-slm-solutions/

So yes, invest using business model plus TA plus a dash of FA. LOL

Denny Schlesinger

Hi Denny, Thanks for the interesting table. In looking at it, it seems like a giant and a bunch of pygmies. The other companies changes which look so huge on a percent basis seem like just random static. Apple’s increase of 67% sounds great when looked at by itself, but it was from 0.9% to 1.5%. That’s nothing. They increased 0.6% in a year, while Amazon makes that much in sales every WEEK.

Best,

Saul

Denny I have been looking at NVO based on a few of your posts. But they seem stuck in a no growth mode.

What would have to happen for either earnings or the P/E to increase?

What would have to happen for either earnings or the P/E to increase?

Sell more insulin at better prices! LOL

The problem is competition and price pressure. Their major market is North America making FDA approval very important. Not too long ago their competitors got approval for a competing drug while the FDA asked them for more data.

They are constantly asking for regulatory approval and this makes business somewhat lumpy. Just today:

Novo Nordisk Files for Regulatory Approval of Once-Weekly Semaglutide with the FDA for the Treatment of Type 2 Diabetes

http://finance.yahoo.com/news/novo-nordisk-files-regulatory-…

It is a complicated business and one has to have faith in management. Their track record is darn good but beyond that I can’t give any assurances.

There is an article today saying that hedge funds are getting back into NVO

http://cdn2.insidermonkey.com/blog/wp-content/uploads/2015/1…

Sorry, wrong image, try this one:

http://cdn2.insidermonkey.com/blog/wp-content/uploads/2016/1…

and the link to the article

http://www.insidermonkey.com/blog/novo-nordisk-as-adr-nvohed…

Denny Schlesinger

ONE THIRD of ALL online RETAIL! Now, that’s a lovely worry to have!

As a running business, sure. As an investor in AMZN, it’s quite worrisome.

Amazon is a great business: great company, great people, great future. The problem is that everyone knows that and agrees, so much so that the stock trades at a 174 PE level. With Amazon already owning 1/3 of all online retail, how can it grow into its current valuation? It literally can’t triple, and probably won’t double, it’s share of online sales. And even with online sales growing, can Amazon’s probably close to stagnant portion of online sales be enough to satisfy that PE?

The answer is no.

But Amazon has other businesses. Web Services (AWS), is the biggie. That’s growing leaps and bounds now and the market as a whole is growing. We don’t really know what the TAM (Total Addressable Market) will be in 5 or 10 years. All kinds of things, including things that don’t even exist today, could run on AWS.

That’s what perhaps justifies Amazon’s high valuation. Perhaps.

The question I ask myself is “Do I understand Amazon’s future business prospects better than the thousands of analysts and hundreds of thousands other investors?”

The answer is no. The problem with investing in AMZN today is that if the company does as well as many people expect, that won’t be enough to fuel future growth - and may even result in a devaluation of its shares.

I’d rather choose a company not so well followed, and not so well understood by analysts or the general population. All analysts understand retail - and most of them understand retail better than I. Even with me understanding AWS pretty darn well, I don’t have any insight that gives me an advantage over all those other smart people.

One example of a company I like very much today is ANET. Most people don’t understand Software Defined Networking and don’t understand how a small company can steal business away from CSCO. That’s something I do understand better than most, and so I feel more comfortable that I have some advantage. For instance, as soon as I read the patent claims against ANET, I bought even more stock, because it was clear to me that CSCO was doing anything it could to slow them down. And that’s because they’re scared.

Smorgasbord1,

Could you please do a Cisco/ANET piece.

As a person interested in Software Defined Networking, from the inside. (The large telecom that I work for is moving that way rapidly.) I understand that not only are the large telecoms interested in Software Defined Networking for its low cost and flexibility, the executives are particularly hostile to the business model passed down to Cisco from Nortel. In other words, while everyone must get on board with the Software Defined Network, Cisco starts out with a handicap; that is, “We don’t like you.”

Cheers

Qazulight

With Amazon already owning 1/3 of all online retail, how can it grow into its current valuation? It literally can’t triple, and probably won’t double, it’s share of online sales. And even with online sales growing, can Amazon’s probably close to stagnant portion of online sales be enough to satisfy that PE?

Hi Smorgasbord,

That’s a good question. But the way I see it is that online sales are only about 12% of all retail sales (I think I read), and keeps growing, and the “all retail sales” pie that it’s a part of keeps growing too. So I don’t see growth petering out. And amazon keeps making Prime more and more attractive, and they’ll probably end up with well more than their current 30% of online sales, and then their is AWS.

That said, I like Arista too.

Best,

Saul

The problem is that everyone knows that and agrees, so much so that the stock trades at a 174 PE level.

If you read the comments to the article I link below you’ll find the world divided about Amazon, not “everyone agrees.”

Amazon India

Amazon Effectively Eliminates Competition In Another Market

Dec. 2, 2016 11:11 AM ET|

Summary

Amazon has always been aggressive outside its home base in the US and now it is looking to build on the momentum to take the leadership position in major markets.

After showing a dismal performance in China, the company went all-in in India with indicated investments of over $5 billion.

This has had a deleterious effect on local players like Flipkart, which has seen its valuation lowered by investor Morgan Stanley from $15.5 billion to $5.54 billion in 18 months.

Amazon is going for the kill in this market where substantial changes in pecking order are possible in the next two quarters.

This market can boost Amazon’s international revenue considerably and would provide a stepping stone for expansion in other markets in the region.

http://seekingalpha.com/article/4027839-amazon-effectively-e…

While India never had a Communist regime like China, it’s protectionist policies kept development in check. It seems they have seen the damage that protectionism brings and while it has not been abolished entirely it is a lot softer now. A developing India will create millions of middle class buyers just like China has done over the past quarter century.

Anyone who thinks that Amazon’s growth is just about over, is wrong. Of course it will end some day but I think 20 more years is a safe bet.

Denny Schlesinger

online sales vs retail sales

I bought my last car online but looked at one in a brick and mortar showroom. And did a test drive from that facility.

So I guess this is an "online"sale but actually it is more complex. We may see a lot more of those mixed sales.

A totally online sale would be one where you buy online and then download whatever it was you bought, zero atoms, 100% bits!

Denny Schlesinger

online sales vs retail sales

I bought my last car online but looked at one in a brick and mortar showroom. And did a test drive from that facility.

So I guess this is an "online"sale but actually it is more complex. We may see a lot more of those mixed sales.

I don’t mean to be petty, but I’m willing to bet that might even be considered “Theft of Services”

I hope you don’t think that the brick and mortar showroom and their employees make a living by your coming in to see and test drive vehicles for you to then buy them on line.

b&w

I don’t mean to be petty, but I’m willing to bet that might even be considered “Theft of Services”

I hope you don’t think that the brick and mortar showroom and their employees make a living by your coming in to see and test drive vehicles for you to then buy them on line.

b&w

So B&W do you think that if I take a test ride from a facility that I am obligated to buy from that facility? Or do you think I can still shop around for the best price? Or what if I like another companies product better. Would I still be obligated to buy from the first facility because I did a test drive?

Andy

I don’t mean to be petty, but I’m willing to bet that might even be considered “Theft of Services”

This is a problem know as Showrooming

https://en.wikipedia.org/wiki/Showrooming

Denny Schlesinger

Thank you Denny for this and all your good work on this board. AMZN is so pioneering and ahead of its time that with proceeds of AWS used to finance growth, plus Bezos’ culture of innovation, how can anyone catch them now?

Andy:

You aren’t obligated to buy anything anywhere. Why don’t you have AMAZON ship you one of each cars you would like to test drive and then ship the others back that you don’t want. I’m sure Amazon will be happy to accommodate you.

b&w

{kind=link}

{kind=link}