Ben’s Portfolio update end of November 2023

Returns and portfolio holdings:

Portfolio Notes 2020 63.6% Since May 12, 2020, where I started this portfolio with over 40 companies, mostly holding large cap tech & FAANG, but also some high-growth SaaS. 2021 13.1% Discovered Saul’s board in February 2021 and started concentrating to 16 companies through December 2021. 2022 -60.7% Concentrated a bit more through July 2022 from which point I started posting my monthly updates on Saul’s board, holding about 12 or fewer positions. 2023 YTD Month Jan 8.3% 8.3% Feb 16.3% 7.3% Mar 17.9% 1.4% Apr 5.2% -10.8% May 40.5% 33.5% Jun 38.6% -1.3% Jul 50.7% 8.7% Aug 41.2% -6.3% Sep 35.3% -4.2% Oct 27.5% -5.8% Nov 66.0% 30.3%

Time stamp: November 30, after market close.

These are my current positions:

Nov 2023 Oct 2023 First buy* Datadog 17.5% 16.0% 5/13/2020 Snowflake 17.0% 17.1% 2/8/2021 Crowdstrike 16.2% 15.8% 5/13/2020 Cloudflare 14.8% 14.1% 11/2/2020 Zscaler 13.4% 14.0% 3/4/2021 Nvidia 12.5% 14.2% 5/13/2020 Monday 6.1% 5.7% 9/13/2021 TradeDesk 1.8% 2.3% 5/13/2020 Enphase 0.8% 0.8% 5/15/2020

Time stamp: November 30, after market close.

*held through today

Company comments:

Cloudflare:

Cloudflare reported Fiscal Q3 2023 on 11/2/23. They delivered $335.6M in revenue (8.8% QoQ, 32.2% YoY), exceeding my expectation of $330M (7.2% QoQ, 30% YoY) and beating their own guide by 1.5%. This is a good development as their beats are starting to pick up again. While I wanted to see a new Q4 guide of $353M (they guided for $352.5M at the midpoint), another 1.5% beat would mean QoQ revenue growth will drop again in Q4, to 6.6%. However, given their improvements in NRR and customer growth numbers this quarter, I think it is likely that they will beat by Q4 by 2% or maybe even more. A 3.6% beat would mean they keep QoQ revenue growth constant at 8.8%. I am not sure how realistic this is considering their beats have been around 1% or less in the previous 4 quarters. On the other hand, improving NRR and accelerating customer growth point towards further revenue growth acceleration … we’ll see which way it goes when they report Q4.

With regard to secondary metrics, the just mentioned NRR rebound to 116%, up by one percent, indicates that this metric might have bottomed, which would be great. But since there is a possibility that it just went from 115.49% last Q to 115.51% this quarter due to noise, I am going to wait another quarter before calling the NRR bottom. Given the inertia in this metric, any further increase in Q4 would be a strong sign of continued revenue re-acceleration, when combined with continued strong customer growth. Speaking about the latter, they grew their total customer base by an amazing 4.5% this quarter. A whole percentage point more than I had hoped for. Large customers, which I expected to grow around 7.5% QoQ grew 8.8%, similar to Q2’s 9.1% growth. RPO growth was a little lighter than I had hoped for, with 4.6% QoQ growth, down from 8% growth last Q.

I estimated the static revenue growth assuming a constant customer growth rate of 3.5% QoQ and a constant NRR of 115% in my August recap. This would lead to revenue growth of 32% YoY. We can do the same calculation with this Q’s numbers and get (1.045^4*1.16), 38% static YoY growth. So it would be fantastic if they can keep customer growth at 4.5% and NRR at 116% going forward. Either way, I am happy to hold Cloudflare if it just keeps growing revenue at about 30% YoY, while making a ton of money at the bottom line.

Speaking about bottom line, profitability continued to greatly improve this quarter: They managed to get $42.5M in operating income, more than doubling last Q’s operating income, beating their guide by an amazing 108% instead of my expected beat of 37%. With that they more than doubled their operating income margin, reaching 12.7%, which is up from 6.6% last Q and 5.8% last Q3. Just for perspective, in my August recap I wrote that I hoped for operating income to come close to $60M in the second half of the FY. With $42.5M in Q3 and a Q4 guide which I hope they can beat by 40%, they would manage another $40M in Q4, or a total of more than $80M in 2H23 - 33% more than I hoped for just 2 months ago. Net margin also more than doubled from last year, reaching 16.5% and FCF margin grew 75% QoQ to 10.4%. It was negative just a year ago! Well done Cloudflare!

Datadog:

Run, Datadog, run! What an amazing Q3 Datadog delivered. Revenue came in at an incredible $547.5M (7.5% QoQ, 25.4% YoY), beating their guide by 4.7% and significantly above my expectation of $533M (4.7% QoQ, 22% YoY), where I had assumed what I thought would have been a strong 2% beat. This revenue growth acceleration is especially noteworthy as Q3 QoQ growth dropped in 4 out of the previous 5 years in comparison to Q2, with 2020 being the exception. So they managed to accelerate revenue growth against a strong seasonal headwind!

For Q4 they guided for $566M, versus my expected $562M and they increased their full year guide by 2.4% to $2.105b. In my August recap about Q2 I wrote “the reduction in the FY guide might not have been necessary”. At the time they had reduced their FY guide to $2.055b, from $2.090b. Turns out they could have increased it all along …

Another way to look at the strong turn-around that Datadog managed in the last two quarters is to look at their sequential net new revenue increases. Just have a look at this plot below:

What a recovery from the most recent bottom! With that, they should handily beat the $60M net new revenue I was dreaming about for 2H23. My projection for Q4 is just based on the assumption that they will be able to beat their Q4 revenue guide again by 4.7%. Here I have not factored in the incredible jump in RPO and billings they managed this quarter, which I believe gives additional upside. Just look how both forward looking metrics improved starting with the bottom-Q1:

RPO QoQ growth: 7.5% → 9.6% → 16.0%

Billings QoQ growth: -4.7% → 1.8% → 16.7%

The most recent RPO and Billings acceleration hasn’t made it yet into revenue growth. I think this is very encouraging. That and that they were able to accelerate in Q3 against a seasonal headwind, while Q4 will be a seasonal tailwind, where QoQ revenue growth accelerated from Q3 to Q4 in every year since 2017, besides the last year’s Q3-Q4, where we were in the midst of the last economic down-cycle.

Also encouraging was QoQ customer growth. Total customer growth is showing first signs of re-acceleration going from 2.4% in Q2 to 2.7% in Q3. The more important cohort of large customers spending more than $100k in ARR jumped from 2.7% in Q2 to 4.7% in Q3 (this cohort makes up for 86% of revenue). Multi-product adoption took a little breather this Q, where the percentage of customers using 2+, 4+ and 6+ products was

Q2 → Q3

82% → 82%,

45% → 46%,

21% → 21%,

respectively. I am hopeful that we’ll see further progress here in Q4.

The only negative I saw in the report was NRR which dropped to below 120%. I am least concerned about this metric though, since it is a backward-looking, lagging metric.

Finally, given their recent profitability margin progress, I would have been just happy with steady margins, but look, they even improved here significantly: operating margin grew to 24%, up from 21% last Q and net margin improved to 29%, up from 25% last Q. FCF margin dropped to 25%, from 28% last Q, but that 28% last Q was what I would call a positive outlier; it is up from 15% last Q3! So again amazing progress here.

Monday:

Monday reported Fiscal Q3 2023 on 11/13/23. Revenue was $189M (7.7% QoQ, 38% YoY), versus my expected $189M (7.7% QoQ, 38% YoY), where I had assumed same 4% beat as last Q. So well done here. For Q4 the guide was $197M (4.1% QoQ, 31.4% YoY) versus my expected $197M (4% QoQ, 31% YoY). Nailed that as well. They also increased their FY guide by 1.3%. In my last Monday recap I wrote “I don’t see them meaningfully breaking out of their quarterly net revenue adds, which has been hovering around $13M.” It was again at $13.5M this Q3, but given their guidance I am optimistic that they will break out of this range when they report Q4, for which I have penciled in $15.7M in net new revenue. Something to watch out for.

We also have a first datapoint showing NRR leveling off for all customers as it stayed above 110% this quarter, while the 10+ and 50k+ ARR cohort’s NRRs continued to drop to above 115% from above 120% in Q2. Again, lagging metric so less concerning and total NRR leveling off is actually encouraging. Hopefully the other cohorts will follow suite and not drop further in Q4.

How about customer growth rates? On the face of it one could be alarmed by the fact that QoQ growth of 50k+ customers dropped for the second quarter in a row, from 14.2% in Q1 to 12.4% in Q2 to now 9.8% in Q3. I think though this has more to do with seasonality than anything else. Q3 seems to have always been a weak quarter for Monday, when it comes to large customer growth. QoQ growth dropped from Q2 to Q3 in every of the last four years and 2023 is no exception. It gets even more interesting when calculating the relative drop in growth from Q2 to Q3: In 2019 QoQ growth dropped from 156% to 100%, or by 36% (56/156=36%). In 2020 it dropped by 24%, in 2021 it dropped by 25%, in 2022 it dropped by 33% and now, in 2023 it only dropped by 17%. You could call this relative strength. So it would be great if they accelerate large customer growth again in Q4.

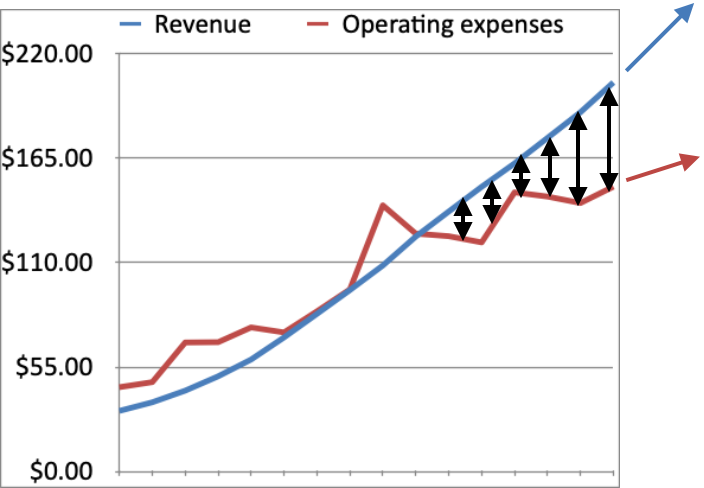

Lastly, Monday continued to deliver on the profitability front: operating income margin jumped to 13%, up from 9% last Q and -2% last Q3. Net income margin jumped to 17%, up from 12% last Q and 2% last Q3. And FCF margin jumped to an amazing 34%, up from 26% last Q and 10% last Q3. Looking at operating expenses versus revenue it is nice to see how the gap is widening here, nicely showing their operational leverage:

Wrapping it up

I’ll cover the earnings reports from Snowflake, Crowdstrike and Zscaler in my next update but from what I have seen so far things are looking pretty good!

Thanks for reading and I wish you all a great December!

Ben

Past recaps

July 2022: Ben’s Portfolio end of July 2022 - Saul’s Investing Discussions - Motley Fool Community

August 2022: Ben’s Portfolio end of August 2022 - Saul’s Investing Discussions - Motley Fool Community

September 2022: Ben’s Portfolio update end of September 2022

October 2022: Ben’s Portfolio update end of October 2022

November 2022: Ben’s Portfolio update end of November 2022

December 2022: Ben’s Portfolio update end of December 2022

January 2023: Ben’s Portfolio update end of January 2023

February 2023: Ben’s Portfolio update end of February 2023

March 2023: Ben’s Portfolio update end of March 2023

April 2023: Ben’s Portfolio update end of April 2023

May 2023: Ben’s Portfolio update end of May 2023

June 2023: Ben’s Portfolio update end of June 2023

July 2023: Ben’s Portfolio update end of July 2023

August 2023: Ben’s Portfolio update end of August 2023

September 2023: Ben’s Portfolio update end of September 2023

October 2023: Ben’s Portfolio update end of October 2023