As interest rates rise you expect the NAV of a bond fund to fall along with the value of their bonds. They should pay competitive interest rates but mostly due to falling NAV.

You expect per share payout to increase as bonds in the portfolio mature and get replaced with higher yielding bonds. Hence, you expect NAV to gradually recover while payout increases.

Best time to buy a bond fund is when you think interest rates have peaked.

But what happens if a whole bunch of people got scared out of the fund meanwhile, and the fund had to sell a bunch of their bonds at a loss? Those bonds may recover someday, but that fund doesn’t own them anymore, someone else does.

This is one of the irksome problems of bond funds.

I agree. Best to buy when interest rates have peaked. And of course as people buy to lock in good interest rates they buy new bonds at higher rates so dividend increases faster.

But closed end fund avoids all of this. Funds for sellers come from the market; not from fund selling bonds.

The opposite is also true. As rates fall, then NAV increases.

Right now, with interest rates backing off --though for all the wrong reasons–, I’m making killer money on my holdings of individual bonds, which tend to be long dated and, therefore, more responsive.

Thank goodness taxes are paid only on realized cap-gains, not on paper ones.

I’m not sure how bond funds work, but stock funds, when they have net capital gains, they distribute them, and they will send you a 1099 with those capital gains on it … and you will have to pay taxes on it. Bond funds probably work similarly.

What you say about having to pay taxes on realized cap gains --from any source-- is true. But taxes aren’t paid on unrealized gains. All that happens is one’s net-worth has increased, but not yet one’s tax liability.

I own a lot of bonds. Not as many as I used to for having gotten massively called as interest rates dropped some years back, but about 250 issues, many of them long-dated, spread across corporates, munis, agencies, and foreign sovereigns. (Plus, a ton of T-Bills.) But no bond funds, because I was doing the equivalent of running my own bond fund for preferring to control when the underlying was bought or sold.

As interest rates rose, my mark-to-market worth on those bonds suffered, predictably and expectedly so. But, no biggie. Part of the game. Now the opposite is happening, and my net-worth is walking back up by $1k or so per day, which is fun, but also kinda scary.

My expectation is that 2024 will be a choppy market and a down market, but that intertest rates won’t be raised, because the Fed can’t raise them without crashing the already too fragile economy, never mind excerbating the problem of servicing our increasing national debt. Therefore, that portion of my portfolio is now in the cat bird’s seat.

What is problematic and will need hands-on management is my tiny, tiny allocation to stocks. But that’s what inverse ETFs are for. So 2024 might be a good year afterall.

Yes, of course. But we were discussing bond funds, and in that case, the decision to realize capital gains (from bond trading) is made by the fund manager, not by the holder of the funds shares. This is yet another reason to not own bond funds and instead invest in bonds directly.

Actually, the thread is less about bond funds and more about the impact of interest rate changes on the the price of bonds, be they held directly or as derivatives (aka, indirectly in a fund).

Yes, there a plenty of reasons not to own bond funds, just as there are plenty of reasons not to own bonds, stocks, options, commodities, etc. It all depends on one’s means, needs, goals, etc.

But let’s stick with bond funds for a bit. There are zero good reasons to own a vanilla bond fund that holds short-term treasuries. In most cases, there are few reasons to own upper-tier corportate bond funds as opposed to the underlying. But as credit quality declines, the usefulness of bond funds increases. And in the case of emerging market bonds, a fund becomes the only reasonable way for most investors to access that asset class.

Bonds are fixed income investments. Bond funds do have potential for increased dividends as bonds mature and are replaced by higher yield bonds. Leveraged Closed end bond funds can also increase income by borrowing to buy more bonds as the yield curve flattens and returns to normal.

When interest rates are falling i would think capital gains are rare for bond funds. Most of their bonds mature and are repaid with no capital gains. I wonder how much bond trading they do. When NAVs are falling and investors are selling they can be forced to sell bonds to fund redemptions. But less so when NAVs are rising.

Really? When interest rates fall, the prices of bonds go up. If the fund has to sell bonds to pay for redemptions, the bonds that it sells may very well have capital gains. So when interest rates fall, that would seem to be the most likely time that bond funds would have to declare capital gains.

Redemptions are not limited to when NAVs are falling - they also occur when NAVs are rising, as some investors would like to realize capital gains.

Sure. But bond funds have bonds maturing and interest income all the time. They almost certainly budget for typical turnover. They do not have to sell bonds for typical turnover.

Its when market conditions cause herd selling that you are most likely to have capital gains.

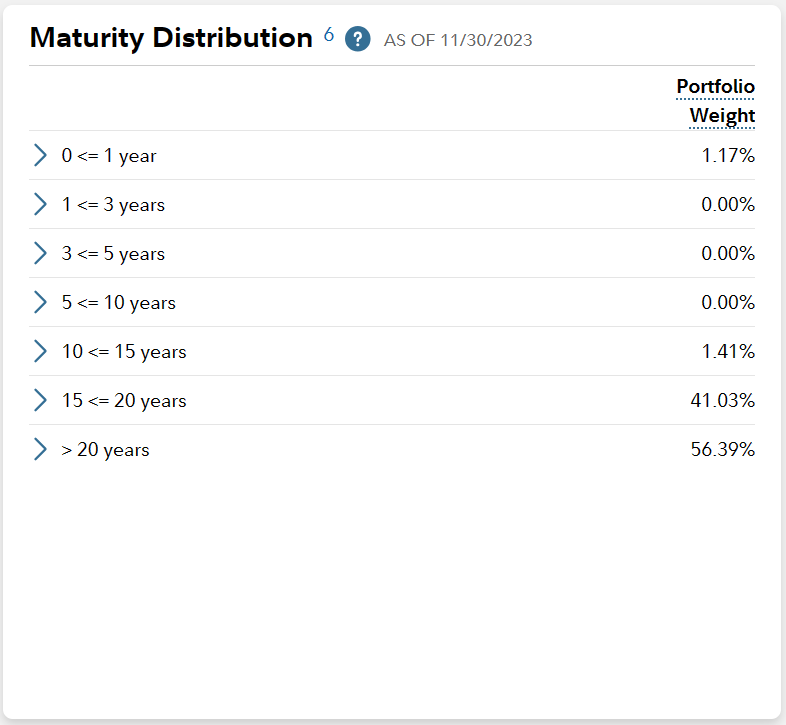

Sorry, but I disagree. The fund may own 56.39% maturing in over 20 years, but if they have been around for over 20 years, they are maturing all the time. The long bond, short bond distribution says nothing about when they mature. It talks about what they buy.

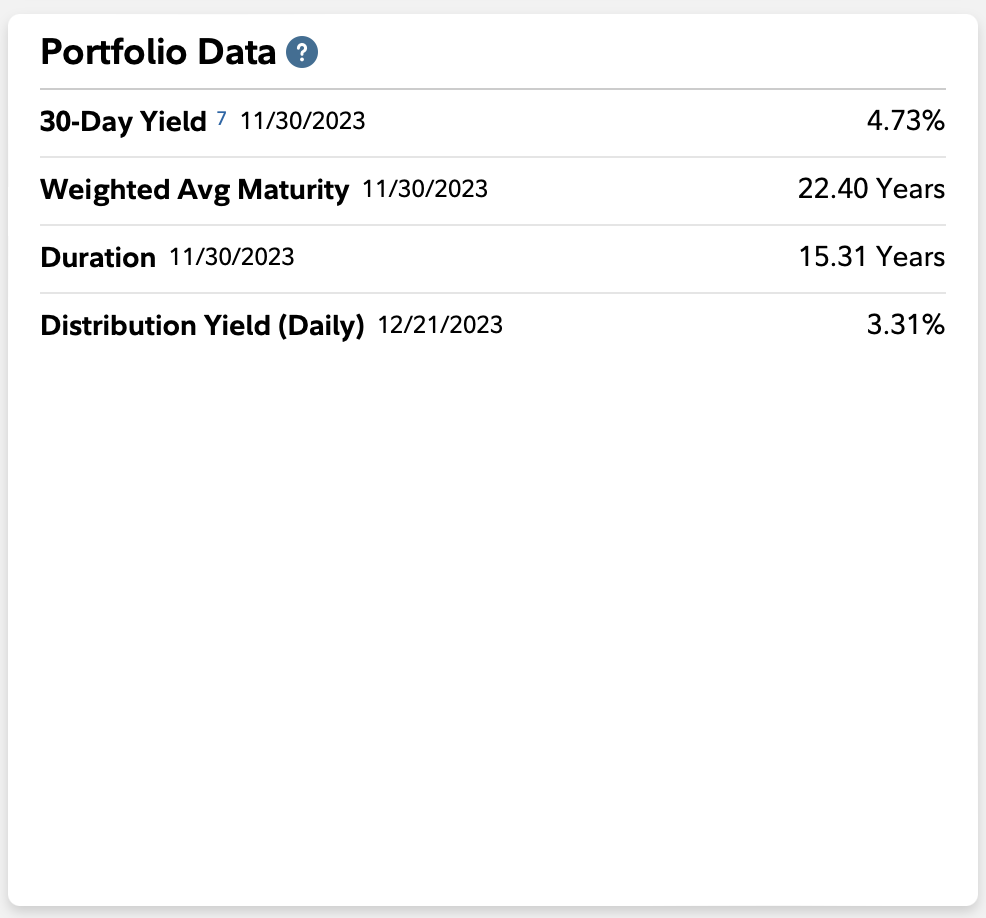

I’m pretty sure that the fund disclosures presented are about what the fund owns … in total, not about what they buy. Their average maturity and duration are quite long, because they are a long-term bond fund (long-term is in the name!),. See image below for average maturity and duration. I suspect they use most of the interest earned on their bonds to pay distributions, and when sudden redemptions occur, they have to sell bonds to raise the money to meet those redemptions.

The issue under discussion is taxable capital gains distributions to holders of bond fund shares. I don’t recall that happening. I think they are possible but rare. What is your experience?

People buy and sell bond shares every day. That does not usually cause bond funds to sell bonds.

But in the example above if the fund buys long bonds and truly owns no 1 to 10 year bonds, that implies they sell their long bonds as they get in that range. That does risk capital gains and losses.

If over the next year, $100M of redemptions come in, with no new money being deposited, basically a net redemption of $100M, then they may have to sell some bonds to meet those redemptions. How many bonds would they have to sell? That’s difficult to answer because it depends on how much of the interest collected they would keep to satisfy those redemptions.

But more simply, if there are $500M of redemptions (redemptions in excess of new investments) in the next year, they would have to sell many of their long-term bonds to raise the money to meet those redemptions. If there were net capital gains from those sales, they (the capital gains) would be distributed to the existing holders of the fund, and they would be taxed appropriately.